"BREAKING!!!" Diaries ain't my thing. This is my second one in four years. Chalk it up to too many nights monitoring the AP machines for stories that might have to be substituted for what we already had pasted up on page 5 or 11 or 23 of whichever newspaper I worked for at the time. That kind of watchfulness gets really old. Occasionally, however, I have to violate my own rules.

When my friend Jerome a Paris wrote his first Countdown to 100$ oil three years ago this month, a number of people laughed their heads off. On that not-so-long-ago June day, oil was trading at $59 a barrel. It took two and a half years before the stuff actually hit $100 a barrel. That happened this January. Since then, Jerome has begun a new series, "Countdown to $200 oil."

I don't hear much laughing.

He started on April 1 with this:

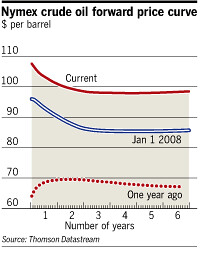

Oil futures are contracts whereby parties commit to buy or sell oil at a pre-agreed price at a given date in the future. The graph shows at what price levels futures traded last Friday, on the first day of this year and a year ago (ie, the most recent futures indicate that markets expect prices to slowly go down from their current level above $100 per barrel to stable prices in the high 90s - and stay there for the next several years: in effect, market are betting on almost constant $100 oil over the foreseeable future).

The most striking thing about these graphs is that markets have no clue whatsoever as to where prices will be in the future. In the past, it used to be simple: whatever the short term price, future prices would be around $20, ie markets expected prices to be stable in the long run, whetever the short term variations. Today, they are in effect still clinging to the same formula, ie that prices will go back to some stable level from where they are today - but given that prices keep on increasing, that target can obviously no longer be $20, and given that they have not been stable at any level in the recent past, they are just taking last month's prices as a "safe" bet.

Today, writes Jad Mouawad at The New York Times, oil prices took their biggest leap ever:

Oil prices had their biggest gains ever on Friday, jumping nearly $11 to a new record above $138 a barrel, after a senior Israeli politician raised the specter of an attack on Iran and the dollar fell sharply against the euro.

The unprecedented gains on Friday capped a second day of strong gains on energy markets, and fueled suspicions that commodities might be caught in a speculative bubble. ...

Even as uncertainties abound about the fundamentals of the market, geopolitical tensions in the Middle East regained center stage after Israel’s transportation minister, Shaul Mofaz, said Friday that an attack on Iran’s nuclear sites looked "unavoidable." Iran is the second-largest oil producer within the OPEC cartel and any interruptions in its exports could push prices higher levels.

"The return of the Iranian risk premium calls for a careful assessment of the potential oil supply impact of military strikes on Iran," said Antoine Halff, an analyst at Newedge, an energy broker. ...

One view that has been gaining ground in recent months is that the commodity market is caught in a speculative bubble akin to the housing or technology bubble of the late 1990s. The notion is buffered by the fact the oil prices have doubled in 12 months despite a slowing economy. ...

"I don’t know how else to say it, this is not a bubble," Jan Stuart, global oil economist at UBS, said. "I think this is real. There is a whole bunch of commercial buyers out there who are spooked and are buying. You are an airline, right now, you’re scared. But I don’t see who would buy at these prices unless they need to."

The always interesting folks over at the Oil Drum have an interesting theory, as explained by Nate Hagens. (As usual, excerpting complex arguments doesn't do them justice. Anybody planning to praise or dice Hagens should read his whole post, which provides the nuance):

A good many years ago, I read George Soros' "The Alchemy of Finance", which introduced me to the concept of reflexivity, which in a nutshell is when observers of a phenomenon can't help but impact the phenomenon itself via their 'observing', thus changing the original underlying fundamentals and setting in motion a boom-bust dynamic (i.e. more exaggerated trends in both directions). Since Mr. Soros recently spoke to Congress regarding the oil futures market 'bubble', I thought I'd take a closer look at the concept of reflexivity, both as it relates to oil and commodities in general, as well as its broader implications for efforts in raising awareness of global resource constraints. ...

In financial markets (which include oil futures), reflexivity occurs when prices themselves influence the fundamentals and that this newly-influenced set of fundamentals then changes expectations, thus influencing prices. This process then continues in a self-reinforcing pattern until it has overshot equilibrium. Because the pattern is self-perpetuating, markets tend towards disequilibrium- where every outcome is uniquely different from the past. (This of course flies in the face of most everything I was taught at the University of Chicago Business School) ...

In 1999 with oil below $10 per barrel, the stock market at all time highs, and resource limit concerns restricted to a handful of cranky environmentalists and Hubbert acolytes, were we at 'equilibrium'? In 2001 with oil at $20? In 2005 with oil at $50? The point is that for a very long time we were not in equilibrium - the pendulum was pulled way to the left and finally let fly in 2000 - the question is, has it now past equilibrium in the other direction? Or have we moved into the third stage, where human collective awareness is accelerating knowledge about and action in the oil sector? More knowledge about finite flow limits changes professionals opinions about the future, which changes investment into refineries, changes long term contracts with exporting nations, changes military strategies, changes hoarding strategies, all of which are reflected in the price moonshot. Soros theory, which I happen to subscribe to, implies we will overshoot in both directions, because gravity and momementum will combine to send the pendulum backwards once market participants have not only caught up, but exceeded the reality of the situation. But Soros (to my knowledge) generally applied this principle to finance, and admitted to Congress he is not an expert in things energy. Reflexivity could of course have larger societal implications beyond investment booms and busts.

In other words, folks, we're flying by the seat of our pants here. And anything could happen. That wildly swinging pendulum could knock a lot of people on their butts.

For those of us who have long argued that we should have higher oil prices, that the $10-a-barrel oil of nine years ago, and the $20 price of 25 years ago, provided the perfect opportunity to gradually boost gasoline taxes and use the revenue to research, develop and commercialize alternative energy sources, the current situation has a bittersweet taste.

Because now, everyone who was saying a decade ago, or two-and-a-half decades ago, that the time wasn't propitious to raise gasoline taxes are finally right. I paid $4.39 a gallon for regular gas yesterday, but I can afford it. Many Americans are hurting. Adding a tax to that hurt right now is not just unpalatable, it's politically impossible.

But, perhaps, just perhaps, the shock of what's happening will finally, finally, finally spur the federal government the way it was spurred in the '70s to actually come up with a far-sighted energy policy the way the much-maligned Jimmy Carter did. And perhaps, this time, it won't be dismantled by the fools who have been doing their best since 1981 to ignore our need to revolutionize our production and consumption of energy and its effects on the environment.