Meta: this post can be considered the sequel (until there's a third) to the epic Your Economy is in Trouble When The Dollar In Your Hand Loses Value by the Day (dKos version) epic.

When we last left off with economic worries, the utmost concern at the time was the seemingly endless water torture trickle of the U.S. Dollar. A few months later and we're still relatively in the same spot - sideways trading becoming the norm since about March of this year. The housing market bubble is not done claiming victims just yet...

...in some ways we've only just begun.

Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation) can trace their roots to The Great Depression and The New Deal. Fannie Mae was set up as a government sponsored monopoly with the expressed purpose of being an entity to provide liquidity (money) to the mortgage market. Fannie Mae made it possible for the American Dream of everyone having a home to be realized for returning soldiers from World War 2 and years onward. As it provided more and more mortgages and the total amount of backed debt grew, the entity was cut from the federal government in 1968 - spun off into its own company with a suggested government backing. To head off charges of monopoly, the government chartered Freddie Mac in 1970 to provide competition - again with the same suggested government backing.

Through their history, Fannie and Freddie have been held to somewhat of a higher standard than competing banks. In the housing boom of this decade, that translates to "they were actually held to a standard", when compared with other banks. In real terms, it meant that they did not have nearly as much exposure to the subprime loans (read: loans that should have never been made) and were thought, at least initially, to be somewhat safe from the bloodshed in the subprime markets.

Of course, these predictions are from the same people who once tagged the housing market bust as a "slowdown", and said that the market should calm down when Bear Sterns fell from $140 to $100 per share -- before it fell to $2 & disappeared from the marketplace.

Click for bigger size

-----

The above chart is one of current conditions in the financial markets vs. other great crashes in our modern financial history - running on a scale of days after the all time high. The purple line is the most recent crash that we have dealt with, the Nasdaq in 2001. It reached a high early that year and would go on to lose more than 75% of its value over the next 650 trading days (note: your average year will have roughly 250 trading days). As portions of its line on the left side of the chart are the furthest down, its decline was the most steep, only being briefly outdone by the 1929 Dow.

Speaking of which, the Dow Jones Industrial Average of 1929 onward is represented by the blue line. It reached its all time high in the middle of 1929, and would go on to lose nearly 90% of its value over the next 700 trading days.

The bold, dark red line is a chart of a stock created to represent a selected industry, in this case a snapshot of the financial industry as represented by the ticker symbol IYF. Its high came in the spring of 2007, almost rising back up to beat its mark that summer, but soon after entering a downward death spiral that has led to losses of more than 45% in less than 400 trading days.

XLF is the ticker symbol of another stock that does what IYF does, but for layman's purposes, is run by a different entity and calculates its price differently than IYF. In the end it is another measure for the financial sector. It is represented on the chart by the bold orange line. Where IYF never overtook its early 2007 high, XLF did, so on the chart its counting starts from the summer of 2007. Its decline, over time, is keeping pace with the speed and severity of the Dow post 1929 - having lost over 50% of its value in under 300 trading days.

The speed at which financials are losing value is staggering, but expected for an industry that made the seemingly fatal mistake of engaging in such a period of irresponsible loaning like there was no tomorrow. It's like the man who thinks he'll be dead in a year so he maxes out all his credit cards, only to find himself quite alive and with creditors haunting him night and day, wishing he was quite dead.

That's just a smoothed out average, though. That's the bright side. If you happen to be caught up in the companies whose value is evaporating before Wall Street's eyes, the pain hurts much more. A selection with 1-year movements...

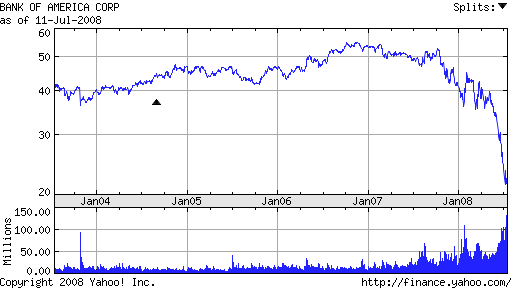

Bank of America: -59%

---

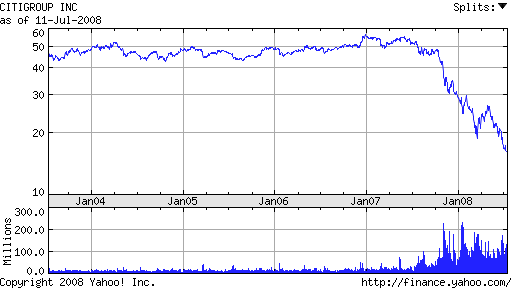

Citigroup: -70%

---

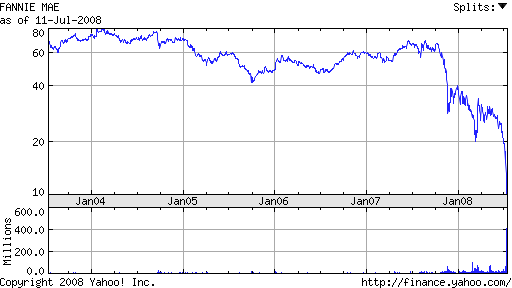

Fanne Mae: -85%

---

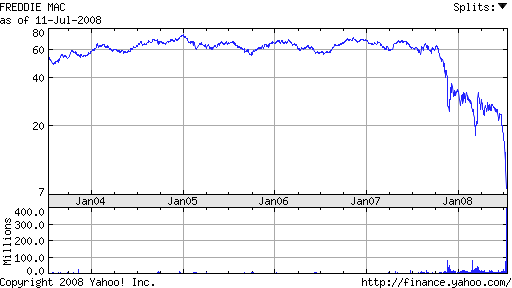

Freddie Mac: -94%

---

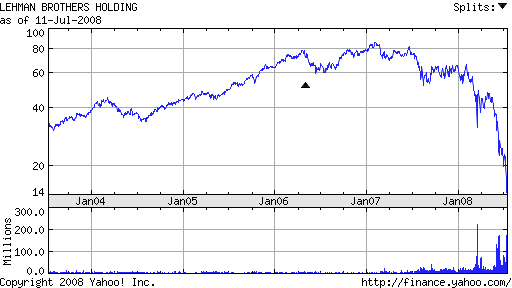

Lehman Brothers: -81%

---

...and the list goes on.

While the plight of stocks and the market in general is getting attention and grabbing the headlines, it is all a symptom of something that could have been seen by anyone who bothered to look for months, even years now. What started as a housing price bubble bursting has turned into something with a life of its own, hammering the quality of life for millions around the country, and worsening by the month.

The unemployment rate, which is an absolutely terrible way of accounting for how many people are really hurting right now is rising.

The amount of money being spent on construction continues to dive.

The root cause of all of this, the decline in the housing market after the decline in prices, shows absolutely no signs of stopping any time soon.

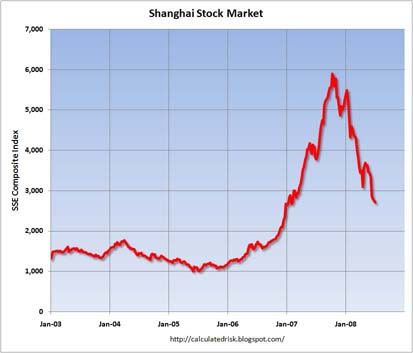

The realization that the United States, the biggest buyer of anything and everything, is in a recession at best is weighing on places where the sky was formally the limit. The above chart is one of the Shanghai stock market, off over 50% in less than a year.

While I do not believe that we are living through a 1929-esque crash, we are probably living through a Nasdaq 2001 crash impacted on the rest of the country. While the 2001 crash was bad, if you really want to get technical about it, it "only" effected the tech sector. While the cliff diving and the destruction of a bunch of .com's and biotechs was bad, the far reaching implications of that will ultimately pale in comparison to the far reaching effects of a crash involving the financial sector at large.

This is a crisis that $600 checks will do nothing to solve. At least for the next five months, though, people who think that just that is the solution to all of our problems will remain at the helm. The next administration has a gigantic financial mess to pick up, and our children, grandchildren, and great-grandchildren have already been saddled with an enormous new financial burden per person that simply was not there a mere eight years ago.

---

Major, major hat tips to the amazing financial blog, Calculated Risk.

Meta2/Disclaimer:

I in no way pretend to be as good as bonddad or Jerome a Paris at breaking down economic things here, but I've been reading their blogs for quite a bit and this economy issue has become more and more important to me - especially since as a resident of the Detroit area I'm in one of the epicenters of the worst this economy has to offer. I know I'll say what they've said, but amidst the siege of candidate diaries, some important issues are getting buried, and I believe this is one of the more important ones that really needs attention. So, sorry if it sounds like a broken record to some.

Cross posted @ my newly launched blog.