It was, as I recall, at some point in October 2008, that the President called us all together on the phone. He wanted to be absolutely clear about our obligation to the campaign, to each other and to our nation -- that it would be a terrible crime to fail to close the deal. After all the hard work by so many for so long, we needed to double down and "leave it all on the field."

When he finished, David Plouffe reinforced the message with a single sentence, which we immediately scrawled on the white board where we tracked our phonebank stats: "let's go out and win this f*cking thing."

Let's start with the most important number in the debate: 19.5 years. On average, a window of political opportunity on healthcare opens every 19.5 years. That's how long we might wait for the chance to fix healthcare to come around again.

You know what you need to do. The President just told you how you can help. Let's go out and win this f*cking thing.

We know the status quo is unacceptable. Tens of millions of uninsured Americans, bankruptcies and foreclosures due to rising costs, insurance "coverage" that is so full of loopholes and exclusions it hardly justifies the name.

As the President just said, "The system works well for the insurance companies but does not work real well for the American people."

So we are going to fix it, and we need your help. Because the best way to drown out the tea party crowd is to reach out personally and directly to people you know - your neighbors, your friends, your family. Post on Facebook and Twitter, e-mail your grandmother who is worried and your friends in red states who are hearing misinformation on a regular basis. Get them to engage and get involved.

And yes, call YOUR representative, if you haven't already. The fact that, as announced today, Organizing for America has generated 60,000 visits to Congressional office speaks volumes more than a few people mugging for the cameras at selected townhalls. It is the sustained, authentic, local pressure that will make the difference. Once you have done that, make sure everyone in your Congressional District is doing the same.

As the President told us "the best offense against lies is the truth." And also that we are the most credible people to deliver that truth. So here's how you can join a phonebank, canvass, rally, townhall or other activity in your area right now - click here and put in your zip code.

Here's the Organizing for Healthcare Portal, where you can send a letter to the editor to your local paper, share information with your networks and make calls to Congress and to your neighbors.

Here's the health care story portal, where you can share your stories and read about why we need to make change.

To quote the President today:

"We cannot be intimidated" but "people are invested in the status quo" and people are "worried - and vulnerable to misinformation."

We are the very people who can help get the right message out. And check out the Reality Check website for ammunition to debunk the lies.

So what are we fighting for? A health insurance exchange with a public option, an expansion of coverage to the uninsured, mechanisms that make healthcare more affordable for everyone and keep insurance companies from taking your protection away.

Here's what the President said today:

"If you don't have health insurance, we intend to provide you high quality, affordable options."

"One of the options WILL be a public option. I think a public option is important. . . . If we have a public option in there it will help keep insurers honest."

So here is what that means in legislative terms:

Versions of HR 3200, or America's Affordable Health Choices Act, have passed all three relevant committees in the House and the Senate version has passed one of two relevant committees in the Senate (Senator Kennedy's HELP Committee).

Pause for a minute and take stock of what that means. In 1994, Clinton never even got a bill out of committee. Presidents for sixty years have tried and failed to pass any kind of healthcare reform. We are closer than we have ever been to success. That means we can't afford to let up.

In addition, although there are some differences among these bills, they are extremely similar in their core elements. I'll highlight a few variations, but these bills are remarkably consistent. The one committee that has yet to act, the Senate Finance Committee, may produce a quite different bill, based on what we have heard they are considering. We have no way of knowing until it is "marked up" (meaning debated and voted on by the Committee.) Right now we have four similar, and strong bills, and one potentially weaker bill.

There are at least five key elements of the bill, present in all four committee-passed versions. I describe each one below and talk about what it does and why it matters. I refuse to assign them a hierarchy, or say which one is the most important, especially because they work best as a package. Here they are: (1) the health insurance exchange, (2) the public option as an element of the exchange, (3) subsidies to help individuals afford insurance and tax credits to help small businesses cover their workers, (4) the improvements to federal programs like Medicare and Medicaid, and (5) the consumer health care bill of rights.

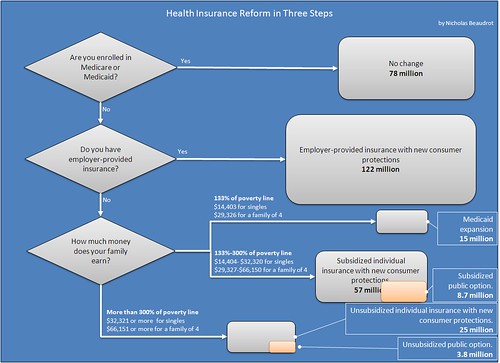

[Update: Can't believe I forgot to credit the flow chart. h/t to donkylicious, and also to the folks at Netroots Nation who were part of the discussion that generarated it.]

Here's a great flowchart that explains how the bill works (note the subsidies part is wrong - it is actually higher as explained below):

1. THE HEALTH INSURANCE EXCHANGE

What is it? Remember the periodic conversation about giving everyday Americans "the same healthcare plan Congress has"? That's what the health insurance exchange does. It creates a one-stop-shopping market where plans compete for your business.

Why do we need it? Currently, Americans who don't have insurance and want it have to try to buy a policy as an individual. Those policies are usually full of loopholes and exclusions, and more expensive than group plans. For example, I have a family member currently under an individual plan that doesn't cover any of the medication he needs, and a close friend with a pre-existing condition about to lose his health insurance, who may be unable to get it on the individual market.

Ezra Klein says the health insurance exchange is "the Most Important, Undernoticed Part of Health Reform:"

You could, of course. . . go buy insurance on your own. But the individual insurance market is a scary place. You're on your own, so you have no bargaining power with insurers. Providers can simply refuse to sell you health insurance, or they can jack up your prices because of past illness. They can sell you a plan that's insufficient for your needs and that's thick with loopholes and technicalities. A favored trick, for instance, is to sell plans that don't cover any preexisting conditions: If you go to a doctor complaining of back pain, but it turns out you've felt back pain before, they don't have to cover any costs relating to the ailment.

The Health Insurance Exchange gives you another option. . . . It will have a wide array of competing providers offering different plans with varying benefit levels, emphases and price tags. Unlike the individual market, insurers won't be able to discriminate based on your health history or your future risk. Plans will have to be certified as meeting a minimum level of comprehensiveness. Plans that routinely screw over members will lose customers to competing insurers.

The Health Insurance Exchange, combines the benefits of choice that are theoretically available on the individual market with the bargaining power and scale that's generally accessible only in large employers (and the exchange will, in theory, have more bargaining power than even the largest employers, as it will have a much larger base of customers).

Under the current bills, the exchange would be open to people without other good health insurance options - the uninsured, the self-employed and small businesses. But there is an additional piece of legislation proposed by Ron Wyden, the Free Choice Act, that would open the exchange to anyone.

2. THE PUBLIC OPTION

What is it? The "public option" would be a new, government-administered nonprofit health insurance program offered as one of the options on the exchange. Health Care for America Now, a broad-based coalition supporting healthcare reform, has established a set of key principles to judge a public option by:

If any proposal meets these principles, no matter what you call it, it is worthy of support.

1. National and available everywhere: A strong public health insurance option will be a national public health insurance program, available in all areas of the country. The insurance industry is made of of conglomerates that have national reach. In order to have the clout to compete with the insurance industry and keep them honest, the public health insurance option must be national as well.

2. Government appointed and accountable: The entire problem with private health insurance is that they aren't accountable to you or me. A public health insurance option must have a different incentive. A public health insurance option doesn't have to be a government entity necessarily, but its decision makers must be appointed by government and must be accountable to government.

3. Bargaining clout: The whole point of health reform is to lower health care costs. Clearly, the insurance industry has failed to lower costs when left to their own devices. As the President says, we need a strong public health insurance option to lower rates, change the incentives in our health care system, and keep the industry honest.

4. Ready on day one: The private health insurance industry has utterly failed to control health care costs or provide their customers the quality they've paid through the nose for. With one person going bankrupt every 30 seconds due to health care costs, we cannot afford to wait any longer for a real fix. We need the public health insurance option to start lowering prices now. That means no trigger.

The four pending bills passed by House and Senate Committees include public options that meet this test - the unknown is what will happen to the Senate Finance Comittee bill, but the chair and committee members appear resistant to the public option.

Why do we need it? The public option would force greater competition on the exchange, because it is likely to have lower costs than private insurers. Jacob Hacker, one of the chief architects of this policy explains it best:

Private insurance and public insurance have distinct strengths and weaknesses, and thus should be encouraged to compete side by side to attract enrollees on a level playing field that rewards plans that deliver better value and health to their enrollees. Public insurance has a better track record at reining in costs, while preserving access; it has pioneered key quality and payment innovations that have often set the standard for private plans; it is essential to set a standard against which private plans must compete to drive value and can be a source of stability for people. Private plans are a source of new benefit options, and continuing pressure for innovation in benefit design and care management strategies.

3. MAKING IT AFFORDABLE - SUPPORT FOR INDIVIDUALS AND SMALL BUSINESSES TO HELP PEOPLE BUY INSURANCE

What is it? The four committee-passed bills include provisions for subsidizing the cost of insurance for individuals and families up to 400% of the poverty line. This means up to $43,320 for an individual and $88,200 for a family of four. Small businesses would get tax credits to help them afford coverage for their workers.

You can download great fact sheets from the House Education and Labor Committee blog that explain a lot of aspects of the bill, including the increased affordability provisions.

Why do we need it? Because health insurance costs are bankrupting middle class families and hurting small businesses. The way to make sure everyone gets covered is to make it easier for people to afford insurance, as well as expanding the safety net programs.

4. IMPROVEMENTS TO CURRENT FEDERAL PROGRAMS LIKE MEDICARE AND MEDICAID

What is it?

All these programs are strengthened and expanded. Federal Medicaid eligibility would go up to 133% - 150% of the poverty level, depending on the version (and states that go beyond that level could keep their programs). Also some state eligibility limits (like only adults with children can get Medicaid) would be eliminated. This would be a fully federally-funded mandate.

We would finally close the infamous Medicare "donut hole" and make prescription drugs more affordable for seniors by permitting national negotiation of drug prices.

Why do we need it?

Many of the uninsured are low-income people not currently eligible for Medicaid. Healthy Families USA estimates that 17 million currently uninsured Americans could get coverage through this program. Making this a federally-funded expansion could ease pressure on state budgets.

5. THE CONSUMER HEALTH CARE BILL OF RIGHTS

What is it?

For people who already have insurance, the bills provide something too - a list of key consumer protections - here's the 8 from the White House website:

* No Discrimination for Pre-Existing Conditions Insurance companies will be prohibited from refusing you coverage because of your medical history.

* No Exorbitant Out-of-Pocket Expenses, Deductibles or Co-Pays Insurance companies will have to abide by yearly caps on how much they can charge for out-of-pocket expenses.

* No Cost-Sharing for Preventive Care Insurance companies must fully cover, without charge, regular checkups and tests that help you prevent illness, such as mammograms or eye and foot exams for diabetics.

* No Dropping of Coverage for Seriously Ill Insurance companies will be prohibited from dropping or watering down insurance coverage for those who become seriously ill.

* No Gender Discrimination Insurance companies will be prohibited from charging you more because of your gender.

* No Annual or Lifetime Caps on Coverage Insurance companies will be prevented from placing annual or lifetime caps on the coverage you receive.

* Extended Coverage for Young Adults Children would continue to be eligible for family coverage through the age of 26.

* Guaranteed Insurance Renewal Insurance companies will be required to renew any policy as long as the policyholder pays their premium in full. Insurance companies won't be allowed to refuse renewal because someone became sick.

And I would add one more - the minimum benefits package. This is the bare minimum that private insurance plans have to meet, so we don't have policies that exclude maternity care and other basic health care needs.

Why do we need it?

Well, because insurance companies routinely do all of those things - drop you when you are sick, jack up your rates just when you can least afford it, make it too expensive to get the basic care that keeps you healthy and avoids expensive treatments later (when they have already dropped you). Simply put, the insurance market is very poorly regulated and it's hurting a lot of people. These bills would help rein in abusive practices. And these protections apply to everyone, not just folks in the Exchange or on the Public Option.

AN HISTORIC OPPORTUNITY

Health care reform is a moral and economic imperative for our nation. And we are closer than we have ever come to getting a bill passed that will make a difference in real people's lives. The changes listed here represent serious reform and we need to get behind this as a package.

Here's those action links again:

Here's how you can join a phonebank, canvass, rally, townhall or other activity in your area right now - click here and put in your zip code.

Here's the Organizing for Healthcare Portal, where you can send a letter to the editor to your local paper, share information with your networks and make calls to Congress and to your neighbors.

Here's the health care story portal, where you can share your stories and read about why we need to make change.

Check out the Reality Check website for ammunition to debunk the lies.

Yes we can win this. Together.

Disclaimer: I am a volunteer with Organizing for America in California. Writing here I speak for myself and not the organization. This diary, and all the words in it, are my own.