I originally wrote this in September 2008 as the financial collapse began. With Senator Levin's expose questioning on "shitty deals" it seemed an opportune time to revisit it -- with some minor variations.

Let me see if I have this straight.

Let me see if I have this straight.

United States businesses, with the help of the Reagan administration, busted the unions, leaving workers more or less powerless to collectively bargain to obtain higher wages.

Then, through the magic of open markets, they placed American labor in competition with foreign labor. They threatened labor "if you don't give us concessions, we'll move our factories overseas, where workers are so poor they'll work for a fraction of what you make". So labor made even more concessions.

And business decided that defined-benefit pension plans were too expensive, and instituted "defined contribution plans" — they didn't have to guarantee a decent pension any more.

Eventually, despite the concessions made by labor, business moved its factories overseas anyway, and crowed how they were benefiting the "consumer" because they were making cheaper goods available. So it was A-OK that workers were seeing no income gains, and having their benefits cut.

And as American business stopped making real things, and adding value to material goods to make a profit, it invented the "financial services industry". It manipulated elected officials and "free market" true believers into deregulating the financial markets. Labor was forced to participate, putting the 401K dollars that replaced the defined benefit pensions into the stock market.

The United States went from having an economy that relied on adding value to raw materials, to an economy that relied on moving mythical money around. And the New American Business — the financial services industry — grew and grew. And claimed to have ended the business cycle; the economy will keep growing perpetually.

Wall Street and the government manipulated and re-defined the statistics the measured economic activity, wages, and inflation — rather like changing all thermometers to centigrade from Fahrenheit, but still declaring that freezing was 32°, that water boiled at 212°, and a body was healthy because the thermometer read 98.6°. Wall Street and the paper economy replaced Main Street and the real economy as the measurement of the economic health of the nation.

When labor complained, business and the Republican-controlled government said "you're crazy! Look at the statistics: inflation is low, interest rates are low, unemployment is low, productivity and profitability are high. If you're not doing well, it's your own fault. You have to get re-educated to participate in the New Economy, and then you can have decent wages".

And the New American Business — the financial services industry — found itself with even more opportunity: with wages low, people relied more and more on their credit cards to make ends meet. And it flooded our mail boxes with pre-approved credit card offers with "low introductory rates" and hidden fees. Not only could profitability be raised by keeping wages low and productivity high, it could make even more money from strapped consumers by selling the means to stay temporarily afloat. And the money flowed in through overdraft fees and late payment fees and increased interest rates.

And the financial institutions merged and expanded and reached their tentacles ever deeper into the very fabric of American life.

Trying to improve their economic outlook, workers who could got more education — taking out loans to do it — only to discover that the "prevailing wage" for rank and file workers was in a race to the bottom (while the "required compensation" for executives increased exponentially in a race to the heights). Labor lost medical coverage and sick leave and vacation time; it worked longer hours, and took second jobs, and wondered why it was that the press and their elected leaders said the economy was booming, but they were running faster and faster and still slipping back. Even if they managed to save some of their meager wages, those savings lost value each and every month as interest rates paid on savings accounts failed to keep up with even an "official" inflation rate manipulated to exclude the exponentially rising costs of housing, health care, fuel and education. As a final insult, the meager returns were taxed as ordinary income, not at the preferred "capital gains" rate.

Far too often, though, the workers fell into bankruptcy not because of bad decisions, but through bad luck: illness, divorce, job loss or the death of a breadwinner — the smallest pebble was enough to disrupt the fragile balance of their economic equilibrium. And there the financiers also had it all their way: bankruptcy laws for individuals were rewritten to be punishingly harsh, allowing less and less debt to be discharged, while the bankruptcy laws for business were designed to make bankruptcy an advantageous business decision, not the least because when a business went into bankruptcy, the compensation owed to the rank and file workers could be "discharged" without a penny paid, while that allegedly owed to the executive suite was honored in full.

And then, with those magical, artificially low interest rates set by the Republican-controlled Fed, the New American Business fomented a housing bubble and touted the "ownership society", convincing the beleaguered workers everyone could "make money from real estate", that the economy could expand if we all just sold houses to one another.

So a house was redefined from a place to live and raise one's family into an "investment" — an ever-paying slot machine of equity just waiting to be tapped. Just pay the fees and take out another loan to pay off those "high interest credit cards". Everyone was exhorted to "get the credit you need and deserve"; houses were sold with no money down adjustable rate piggy-backed liar's loans with the emphasis on the low mortgage payments of the first three years, and assurance that when that low teaser rate ended it was "safe as houses" because real estate prices always went up, they could get a different loan, or another loan, when the teaser rate reset.

And as the Great Credit Wheel spun, the financial services industry convinced the American worker that they could ensure their own financial security by investing their savings, whether for retirement or their children's college educations, in their own debt. They could buy shares in banks, or even better, "mortgage backed securities" — real estate loans bundled together and sliced and diced and shredded in a manner which would virtually eliminate risk. The credit rating agencies said so! They were all AAA-rated investment opportunities — Safe As Houses!

Except the houses weren't safe; they were built on sand foundations in flood plains and resting on fault lines. The builders colluded with the building inspectors to rig the game, and then bet on the inevitable collapse of the entire edifice.

And every step along the way, the commoners paid a fee — fees on their credit card debt; fees to refinance their mortgages; fees to take out home equity loans to pay off their credit card debt; fees to take out student loans.

And paid more fees to the brokerage houses and investment advisors to buy a piece of their own debt, taking a dollar out of one pocket and putting it in the other and leaving a few pennies or dimes or quarters along the way, never knowing that they were investing in shit, and the financial experts and advisers knew they were serving up shit.

Each step of the way, the financial services industry proclaimed the strength of the economy, and put ever greater shares of the phantom wealth onto their own ledgers, granting executives bonuses and golden parachutes to the point that their only possibility trajectory was to fail upwards, with ever larger pieces of the pie. At every turn the commoners lost with no safety net to break their fall; at every turn the financial services industry made a killing, floating on golden parachutes through the stratosphere.

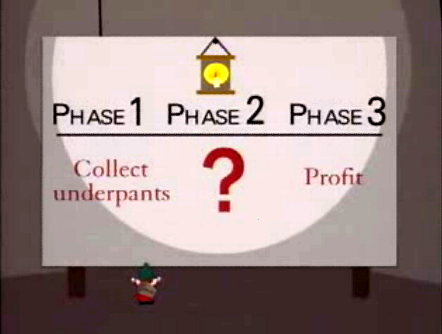

And when the entire Ponzi scheme fell apart, the Underpants Gnomes finally figured out the last step between "steal underpants" and "profit".

You sell the dirty, tattered underwear back to its original owners at a premium price, under the threat of leaving us all bare-assed naked.