Greece on Monday became the country with the lowest credit rating in the world after Standard & Poor's downgraded it by three notches, saying the agency would consider a likely debt restructuring as a default.

Reuters via Yahoo!

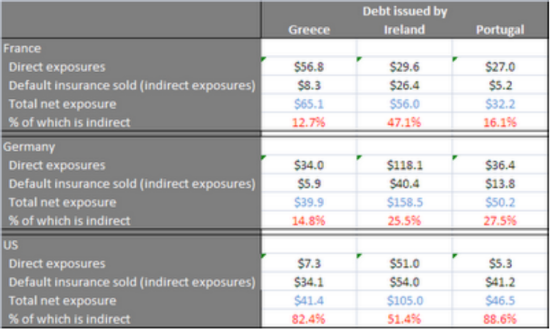

US firms are on the hook for insuring these defaults. Details below the Orange Squiggle of Power.

This image, obtained here, shows that different nation's banks are exposed to Greece in different ways.

Banks in France and Germany have, respectively, $56.8B and $34.0B of direct exposure to Greek sovereign debt - meaning that they have lent Greece money in that amount. Their indirect exposure, which means they have agreed to be on the insuring side of a credit default swap, is $8.3B and $5.9B, respectively.

Banks in the United States have $7.3B in direct exposure and $34.1B in indirect exposure.

What this means is that France and Germany have lent Greece money and insured their loans with US banks. If Greece actually defaults, tens of billions of dollars will flow from the United States to Europe as a consequence.

But the important thing to remember about credit default swaps is that it is possible to sell them without either party being involved at all with the possibly defaulting party - in this case, Greece. For example, I could sell Meteor Blades a CDS on Greek sovereign debt without either he nor I owning a single drachma worth of Greek bonds - that is, if MB and I were both big-time banks.

And since, as noted in the linked Minyanville article, there is NO exchange for credit default swaps, there is no way to know how many such deals have been struck. The US banks say that they have re-insured their insurance; with who is not known. There may be another AIG coming down the pipe and no one would know.

A Greek default would likely result in a "flight to quality", where investors sold stocks and purchased safer vehicles such as US Treasuries. If, then, a few weeks after the Greek shock the United States were to default because Republicans wouldn't raise the debt ceiling, the results would be catastrophic.

Are you ready for another set of bank bailouts? You know, I think that maybe this time we'll test whether or not these banks are too big to fail.

A little Shelly seems apropos

I met a traveller from an antique land

Who said: "Two vast and trunkless legs of stone

Stand in the desert. Near them on the sand,

Half sunk, a shattered visage lies, whose frown

And wrinkled lip and sneer of cold command

Tell that its sculptor well those passions read

Which yet survive, stamped on these lifeless things,

The hand that mocked them and the heart that fed.

And on the pedestal these words appear:

`My name is Ozymandias, King of Kings:

Look on my works, ye mighty, and despair!'

Nothing beside remains. Round the decay

Of that colossal wreck, boundless and bare,

The lone and level sands stretch far away".

Or, perhaps, Yeats

Turning and turning in the widening gyre

The falcon cannot hear the falconer;

Things fall apart; the centre cannot hold;

Mere anarchy is loosed upon the world,

The blood-dimmed tide is loosed, and everywhere

The ceremony of innocence is drowned;

The best lack all conviction, while the worst

Are full of passionate intensity.

Surely some revelation is at hand;

Surely the Second Coming is at hand.

The Second Coming! Hardly are those words out

When a vast image out of Spiritus Mundi

Troubles my sight: a waste of desert sand;

A shape with lion body and the head of a man,

A gaze blank and pitiless as the sun,

Is moving its slow thighs, while all about it

Wind shadows of the indignant desert birds.

The darkness drops again but now I know

That twenty centuries of stony sleep

Were vexed to nightmare by a rocking cradle,

And what rough beast, its hour come round at last,

Slouches towards Bethlehem to be born?

1:38 PM PT: Added information from Bloomberg

The confrontation between the European Central Bank and Germany over bailing out Greece risks causing so much damage that officials may be forced to compromise.

“The balance of forces in the euro zone is a little like it was in the Cold War: both sides are brandishing deterrents that would be too horrendous to use,” said Philip Whyte, a senior research fellow at the Centre for European Reform in London. “It’s all going to turn on whether you can fiddle with debt maturities without calling it a credit event.”

What this says, translated, is that the proposed mechanism for saving Greece's credit is to push out the number of years Greece has to repay said debt. S&P has announced today that it will view such a move as Greece defaulting on its debt, triggering the "swap" in the credit default swaps.

Somebody has to concede ground over the coming days or the region will experience a full-blown financial crisis,” JP Morgan Chase & Co. economists led by Bruce Kasman, the firm’s New York-based chief economist, wrote in a June 10 report. ‘Our inclination is to think that the German government will back down and that the region will reach an agreement on a financing package that will include some modest, voluntary private-sector involvement.”

The debt crisis has already forced Trichet to tear up the rule book. The ECB is lending unlimited amounts of cash to support banking systems and has relaxed collateral requirements. In May 2010, it took the unprecedented decision to start buying the bonds of distressed nations in an effort to calm markets as Greece’s fiscal woes began to infect other euro-area members.

The Frankfurt-based central bank has since bought about 75 billion euros of bonds. Of that, 40 billion euros is Greek debt, according to a Barclays Capital estimate. The ECB stopped buying bonds 10 weeks ago.

Trichet is the head of the European Central Bank (ECB). If Greece defaults the European equivalent of the Fed takes a &Euro;40B hit, which is about $56B.

Bloomberg