Derek Thompson over at the Atlantic posted yesterday on the US's "two-speed recovery." He starts by noting:

The recovery is real. It's strong. It's widespread. It's historic.

Huh? What about that 9.2 unemployment rate? The weak housing market? What the heck is Thompson talking about?

This:

The multinational-corporate and financial sectors are experiencing a comeback of gosh-wow proportions. Corporate profits captured nearly 90 percent of the growth in real national income since growth returned in June 2009, an unprecedented share and nearly twice as dominant as the recovery 20 years ago.

But that's only the beginning of the story. Join me on the flip for the rest, as illustrated in two new charts produced by the IMF.

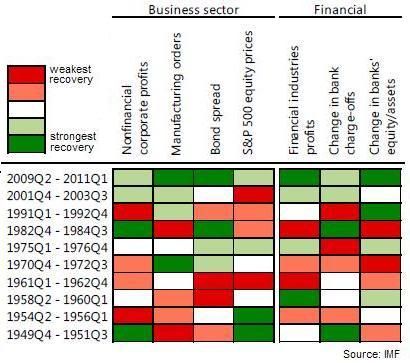

First, Thompson gives us a graphic showing how the business side of the recovery is looking these days:

If you need help reading that, the short version is that the current recovery for the business and financial sectors is the strongest in the US, when compared to all previous recoveries dating back to 1949.

I didn't know that until today.

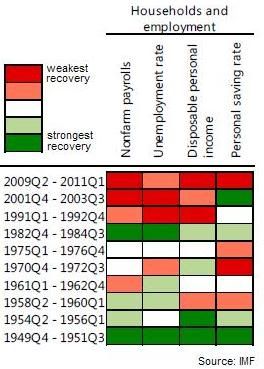

But we need to round out that picture with the second IMF chart, which makes the same comparison from the perspective of households and employment:

Thompson doesn't want to make a sweeping statement about class warfare, but I will. This recovery is booming along just fine, just so long as you're at the top of the economic spectrum. For those of us who are not in the top 1% of income, however, we're suffering through absolutely the worst recovery in recent history -- after suffering through the worst recession in recent history.

The political discourse in Washington is absolutely backward, and here I will give Thompson credit for asking the right questions:

When you look at these charts and contemplate the need for deficit reduction, the first question you'd want to answer is: Where should we schedule cuts? Should we concentrate them exclusively among government employees and middle class families who depend on government services, or should we also begin deficit reduction by finding reasonable ways to ask the richest Americans to pay more?

By the way, while you're over at the Atlantic, you need to check out James Fallows' column today on the sources of the budget deficit. I won't go into the details, except to point out that he starts by noting that Clinton's final budget projection expected the US to have a $2.3 trillion surplus by 2011. Instead, of course, we have a $14 trillion deficit.