Krugman's latest post suggests that we just aren't doing enough to fix our economy, that if only the Fed and the government had implemented the right monetary and stimulus policies over the past few years that we could have whipped this recession and things would be going much better than they are now. He leaves out two major points by using the August 4th market crash to justify writing that is wholly American-centered: the European debt crisis and, most importantly, worldwide oil supplies. I hope to show that we're in a deeper hole than most people realize, and if we don't start honestly acknowledging the situation, we'll never be able to plan to dig ourselves out.

I have a lot of respect for Krugman, and generally I agree with his commentary. That said, he suggests that the crash is due to market concerns about US growth. This may be partially true, but it doesn't begin to tell the whole story. First, the markets aren't just worried about the US lack of growth, they're worried about debt defaults throughout Europe. Some credit agencies Greece is already defaulting on their debt by asking for "voluntary" restructuring of debt deals to be more favorable to Greece. This is on top of massive austerity cuts in Greece that led to large riots, captured in the image of a Greek parliament guard holding station while being exposed to tear gas used on the rioters. As Krugman said, Treasury yields remain low, indicating that nobody is worried about American debt. On the other hand, European yields in troubled economies have been rising and may continue to rise, demonstrating the real fear that some European countries will be unable to pay back their debts.

The second and more important issue Krugman ignores is the impact of oil prices and oil supply on our economy, which is a real and ongoing drag. Our economic growth over the past several decades was fueled by an increasing supply of cheap oil; the correlation between growth in oil supply and growth in world GDP is made very apparent in a paper published in the journal Energy which is summarized here (feel free to message me for access to the paper itself). The difference between what America spent in 2002 versus today on just oil imports amounts to almost 2% of America's GDP! (This number will be fully explained later on.) When oil does get brought up by the media, people point fingers at Libya, speculators, domestic drilling policy, OPEC manipulation, and oil company profits, sometimes at the same time. The fundamentals of the oil industry suggest that these are at most peripheral effects, and that oil prices are high because demand is outstripping supply, and new supplies are incredibly expensive compared to historical numbers. Simply put, we are running out of cheap oil. The American military is incredibly tuned in to the oil supply problem, and they released the following statement in February of 2010 in their 2010 Joint Operating Environment (pdf), which is intended to serve as a perspective on future trends, shocks, contexts, and implications for the military and national security :

... petroleum must continue to satisfy most of the demand for energy out to 2030. Assuming the most optimistic scenario for improved petroleum production through enhanced recovery means, the development of non-conventional oils (such as oil shales or tar sands) and new discoveries, petroleum production will be hard pressed to meet the expected future demand of 118 million barrels per day.

The American military, one of the world's largest oil consumers, is extremely worried about oil supplies over the next 20 years. Consider that traditional oil wells can supply oil for dollars a barrel, whereas the Canadian tar sands operate at closer to $40 per barrel when all costs (except environmental) are considered. When prices began rising in 2002 from a low of $20/barrel, oil corporations bet that they would continue to stay high enough to support the cost of extracting oil from tar sands. This indicates a fundamental shift, and it's caused by rising worldwide demand even in the face of higher oil prices, especially from China and India. Moreover, cheap traditional oil supplies are declining rapidly as older oil fields have passed their peak production. New supply will necessarily be much more expensive.

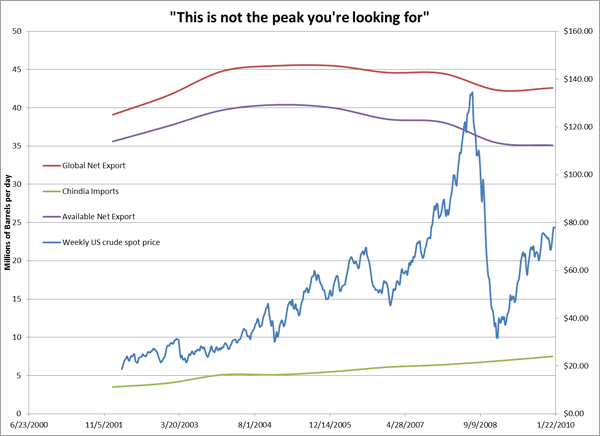

The situation is even worse when you get beyond just supply and demand and start looking at the oil exports, or the oil that actually gets to the market. If Saudi Arabia produces 10 million barrels per day (mbd) but consumes 1 mbd internally, the global market only "sees" 9 mbd of supply. Consider the following graph that looks at global net exports:

This chart is based on data collected by an analyst who goes by westtexas and posts to www.theoildrum.com. Most of the data is supplied by BP, with some additional information coming from the IEA and other sources. The left vertical axis plots oil global net exports, global exports minus China and India imports, and China and India imports in mbd. The right vertical axis shows the American spot price of oil over this same time, with data obtained from the US Energy Information Administration (EIA). The chart clearly shows a peak in global net exports in 2005, and also that China and India continue to increase their oil consumption, leaving far less available for the developed nations to consume. The peak in exports does not show up in the overall supply data, and it happened because oil exporting nations have been increasing internal consumption, best illustrated by rapidly dropping Saudi Arabian oil exports. It is not surprising that American oil imports peaked in August of 2006 according EIA, and have been dropping ever since.

The other interesting point to note in the graph is what happened to the price of oil during and after the recession. The graph shows that even at the depth of the 2008 Recession, oil never dropped below $30/barrel, and it immediately began to rise even as the recession continued. The price data ends in January, but we now know that oil continued to rise, with prices spiking again above $100/barrel, and even with the latest market crash oil prices remain around $90/barrel. Compare that with the $20/barrel price of oil in 2002, and then consider that America imported more than 11 mbd in 2010. At an average price difference of $60 /barrel, that amounts to $250 billion per year that America must spend due to the increased cost of oil as compared with what we were paying in 2002! To continue with the ditch metaphor, no wonder we're having a hard time getting back on the road and driving again when we're having to pay so much more for fuel.

Now, let's get back to all of the finger pointing with regards to oil supplies and prices. I mentioned Libya, domestic drilling policy, OPEC manipulation, speculators, and oil company profits. First, Libya produced about 1.6 mbd before the revolution. That's less than 2% of world oil production, and if oil supply was robust others should have been able to pick up the slack using their spare capacity. Next, let's look at domestic drilling policy. This is the easiest to discredit, because the EIA says that America has total proven reserves of about 20 billion barrels, including the Gulf of Mexico and Arctic National Wildlife Reserve. Remember that we import 11 mbd, or 4 billion barrels per year - our entire proven reserves would only last us 5 years at current rates of consumption! Remember that number, it's a useful fact to discredit rightwing talking heads dinging Obama on oil policies.

OPEC manipulation is a problem, but they are limited by their reliance on oil money. Saudi Arabia has the most proven reserves and is the biggest oil producer and exporter in the world; given their dominance they serve as a useful microcosm for looking at OPEC. Like other OPEC members, Saudi Arabia is totally dependent on their oil to fuel their economy, as it supplies 75% of government revenues. It is also important to note that Saudi Arabia, like Iran, subsidizes food and fuel to help prevent unrest. While Saudi Arabia likes high oil prices, they must produce enough to fuel their economy, and longer term they must try to prevent the world from moving off of oil, or their country will literally collapse. To further complicate the issue, Saudi oil officials have been releasing confusing and contradictory statements in 2011. I have seen the suggestion that they are intentionally confusing things to add uncertainty to the markets to drive up price, but this can only work for so long as they are fundamentally dependent on selling a lot of oil to the world to fund their lifestyle. In short, OPEC is forced to continue to produce a lot of oil, giving them limited leeway with regards to manipulating prices.

As for speculators and oil company profits, these seem especially unlikely to be fundamentally responsible for high oil prices. A CNBC article suggested that the oil bubble fluctuation in 2008 was due to speculation, but what they don't talk about is how much money speculators lost in the crash. Speculators can only drive up the price for so long before they must pay up - consider that any oil speculator who expected oil prices to increase just lost a lot of money. Moreover, think about how much oil speculators would have to store in order to have an appreciable impact on the world supply of 85 mbd. Just to swing that by a 1 percent would require storing nearly a million barrels per day. The Strategic Petroleum Reserve is the only entity that comes close to storing enough oil to begin to effect prices beyond the short term, and high oil prices started rising steadily almost 9 years ago. Speculators incorporate longer term considerations (speculations) into current prices. This can be used maliciously to create bubbles, but speculation as a whole does not lead to long-term prices above where they would be - speculators make money on changes in oil price, not a stable high price. Oil company profits are an even worse scapegoat, because they simply sell oil at the highest price the market will bear. Their profits are huge, but the companies are also huge, and their profits as a percentage of revenues are lower than the Fortune 500 average. If we blame oil companies we are missing the fundamental problem, and that is that the world is running out of cheap oil. We can and probably should cut oil subsidies, but that won't even begin to solve the problem, and might even make it worse depending on what the money is used for.

The oil industry scapegoats are useful for obfuscating the reality of the situation, which helps maintain the current power structure. If people were more aware of the fundamentally unsustainable route the world is on with regards to an oil-based economy, there would be far more political pressure to transform our system to use other sources of energy. The oil industry absolutely doesn't want this, and they benefit greatly from the general confusion surrounding oil prices, and to the extent that you want to blame oil companies, blame them for trying to suppress the truth about oil supplies. Still, you can find plenty of oil industry insiders willing to talk about the reality, including BP's former chief petroleum engineer.

All economies are intricately tied to energy consumption, and our American economy is particularly tied to energy in the form of oil. Anybody who claims that we just need some particular government stimulus or monetary policy to fix the situation is blowing smoke. The era of growing supplies of cheap oil is done and gone. All hope is not lost, but the rough patch we're in will continue to prove difficult until we get serious about ending our dependence on all oil, foreign and domestic. It can be done, but it will be far more difficult than anyone in Washington is willing to say, because this is a message that will likely get the messenger shot. We have to wake ourselves to realize the truth, and demand policies that will remedy the situation. These include funding for public transportation and research into alternative energy. Some of this has been done recently thanks to Obama and the Democratic Congress, but we need greater action sustained over much longer time scales to solve the problem. This can only be accomplished when we and the American public become aware of the magnitude of the oil supply crunch.