There's been a lot of discussion of late of an imminent downturn or a double-dip recession.

Some blame the debt ceiling fiasco and the GOP's hostage taking.

Others blame Euro-zone debt and banking problems.

Others still blame S&P.

And yet another group blames the drag from the Japan earthquake/tsunami/nuclear accident.

Not enough people are looking at a fundamental economic downside: oil.

While I know he hasn't posted here in a while, I'd like to look at a very conventional, but interesting economic analysis NDD posted today:

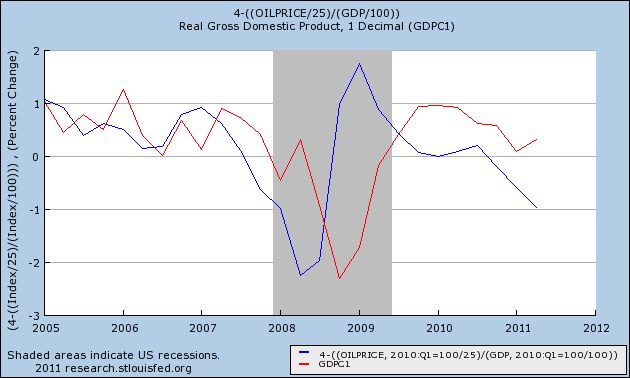

Oil analyst Steven Kopits, along with Prof. James Hamilton, are the two leading experts on how Oil shocks result in recessions. I have been referring to Mr. Kopits' metric every week in my "Weekly Indicators" summations. Kopits says that every time Oil prices rise to a level of 4% or more of GDP, a recession has followed.

Occasionally even the most popular economic bloggers, including top flight professors, express mystification at why the economy doesn't seem to be able to generate a self-sustaining liftoff. In response thereto, I give you the following graph, in which Oil prices as a percent of GDP are shown in blue (inverted, left scale), and quarterly GDP changes in red (right scale):

Let me explain his graph and its importance first, then talk about some bigger picture issues. The blue line is proportional to the inverse of oil prices - when the blue line dips below 0, that means that we've crossed the 4% threshold described above, which is the point at which oil prices are causing enough of an economic drag to cause a slowdown or outright recession. As you can see, the blue line dipped into negative territory in 2007 and GDP growth (the red line) followed close behind it. More worrying is that in the end of 2010 and the first half of this year the blue line dipped negative again.

Does this mean we'll go into a recession this year? It's not clear - oil prices are dropping fast at the moment, and are now back below the 4% threshold. However, it seems likely that we'll have at least one quarter of negative GDP growth this year (if not the two negative quarters required for an official recession).

What is the long term impact of oil prices on economic growth?

I do think it'd be valuable to take it one step further: looking at oil production itself. We've been on a production plateau globally since 2005 - after decades of globally increasing oil production, in 2005 that growth stopped: we have an energy ceiling. By all indications (analyses of the oil megaprojects that are likely to come online in the next 5-7 years, which are known because these things take time to develop) we're looking at a ever tightening oil choke collar in the coming years as oil production starts declining globally.

What happens then? While we have adjusted better (though not completely) to high gas prices this time around vs. 2008, declining oil production means that the choke collar is going to hit us frequently, which basically puts an end to sustained economic growth anytime this decade.

This recently revised chart from Calculated Risk shows that the latest GDP numbers indicate that we're still below 2007-level economic activity once you adjust for inflation:

Declining oil production is likely to manifest itself like it just has - an oil choke collar 2-3 years after every recession/downturn. If we have recessions or downturns every 2-3 years from here on out, is it really likely we're ever going to substantially exceed 2007 GDP?

Until next time...