That’s right. Unless you are on NY AG Eric Schneidermans' side here, one can't claim to care about the abuses of Wall Street and the overall fraud behind the subprime mortgage meltdown and the foreclosure crisis. It's really that simple. You have to criticize this White House for pressuring him to side with the dirty banker deal they still support or factually one really can't claim to care about a functioning financial system or economy at all.

For instance, it occurs to me that as our brave brothers and sisters are getting beaten and maced while occupying Wall Street, we must not forget that there is a real chance for some accountability.

original art by ©priceman but feel free to share it with anyone you want. Make it go viral!

There is also a chance for us to submit the idea that more attention should be paid to this story among the protesters so the media can't say there is no unifying message. Like Susan Sarandon said, there should be some unifying messages that tie everything together like campaign finance reform and ending Too Big To Fail. I would argue the same not that I don't think there are already unifying messages by occupying Wall Street in general now that the movement is spreading to more cities. Prosecuting fraud is also at the core of all of which #occupywallstreet is protesting, so why not draw attention to the fight Eric Schneiderman is bringing forth against the banks?

NY AG Eric Schneiderman like Elliot Spitzer before him is not budging despite this administration’s attempts to get him to basically sign onto the dirty banker deal and paltry 20 billion dollar settlement for crashing our economy and taking a big part crashing the global economy, municipalities and the like. This dynamic might rock the markets soon with the prospects of Greece defaulting causing insolvency with their bond holders in France and elsewhere as well. This is behind the joblessness and the sickening austerity measures prolonging it all of which is being protested.

Is New York Attorney General Eric Schneiderman the One to Finally Fight Big Money's Power in Politics?

Schneiderman may not disappoint. In an interview with Salon in his office, Schneiderman refused to get specific about criminal or civil, jail time or fines. But he made clear that he has committed time and staff to an investigation with goals that go well beyond extracting $20 billion in exchange for release from prosecution, the deal that his fellow state attorneys general have tossed onto the table down in Washington, and which the Obama administration would like to see him sign.

"The people who caused this crash have to be held accountable and I don't detect any diminution in the desire of the people of New York for that basic kind of justice to be done," he said. "Part of this [investigation] is to air this out and expose it so we can make sure it never happens again."

Snip

"I think the banks are very scared," said Tom Adams, a former securities insurer who now writes about the banking industry for nakedcapitalist.com. Adams says he believes Schneiderman has no shortage of hurt and angry former Wall Street players willing to talk to him about what went down.

"To impose accountability seems to be an overarching theme for him, by pursuing this in a way the SEC hasn't," Adams went on. "A crisis happened and there were people responsible. I think he has fertile territory in MBS [mortgage backed securities] and CDOs [collateralized debt obligations] and if he actually names individuals and gets meaningful time, that would be significant, more than taking away the jets or the Hamptons homes."

For all his mildness, Schneiderman disdains the current discourse of Washington.

"One of the things that concerns me right now is this effort to rewrite history, to move us away from the fact that it was bad deregulatory moves and greedy, risky conduct that caused this to happen and that it wasn't the fault of the teachers and cops and firefighters who now seem to be the targets of this effort to cut spending. The markets didn't crash because we were paying too much to teachers."

Yes. Attorney General Eric Schneiderman is the one to finally fight big money's power in politics as the banksters want more than just a small settlement they can make up very quickly and then go on to business as usual. They want…

These Robber barons that used robo-signers to foreclose homes are looking to make a deal that would give them immunity from states that are conducting foreclosure investigations which is one of the main reasons out of many NY AG Eric Schneiderman heroically is standing alone in upholding an actual functioning financial system and economy. Attorney General Tom Miller doesn’t get this and he foolishly booted Shneiderman off of the 50 state AG committee while pursuing a deeply flawed deal. I would say his naiveté and this administration’s naiveté or complicity is dangerous.

Anyone who says Scheiderman opposing this deal would hurt consumers really doesn’t understand the securitization process and how broken and interconnected it is with home owners and investors. I have unfortunately heard the same thing here in attempts to defend this administration. It's sad when defending politicians or refusing to stand up to the status quo takes precedence over a functioning financial system and economy. Unless accountability and legal principle behind every transaction of every functioning dollar is upheld our system is ultimately worthless. I'm afraid the so called "pragmatic" excuse fails miserably just like MBS did and will again.

Nice words to hear from someone with subpoena power on Wall Street. But in June, Iowa Attorney General Tom Miller booted Schneiderman off the 50-state AG's committee that's been trying to make its own deal with the banks over mortgage servicing. Miller's spokesman in Des Moines said Schneiderman's desire to go after the big fish -- the investors and banks -- would hurt consumers.

"We are trying to focus on homeowners, not investors," said Geoff Greenwood of the Iowa AG's office. "We are focused on foreclosure, servicing. We are not trying to address everything under the sun in connection with our financial crisis and we think that by including securitization we are definitely stalling the case, broadening beyond homeowners and potentially pitting homeowners against investors."

Schneiderman responds that he'd rather not "get into a tit for tat" over what happened with the Iowa AG, but insisted that their tack is too narrow. So, he's pursuing a New York-based investigation, which may or may not lead to a separate and better deal, leveraged with depositions and subpoenaed documents revealing facts about the mortgage servicing issues that affect consumers, and also the so-called securitization issues -- the mortgage-backed securities and CDOs, investor products that actually led to the economic crash still playing out on the shabby streets and foreclosed homes of Main Street America.

Eric Scheiderman is right and everyone who wants to make excuses for the Iowa AG and this administration are wrong and they have a fundamental misunderstanding of our entire system and our entire economy, period. Hell yes, their tack is too narrow. Their understanding of the foreclosure crisis is too narrow. Their understanding of the heart of the foreclosure crisis and the fraud within is too narrow.

You have to address everything behind this crisis because they are connected. Duh. Otherwise as James K. Galbraith stated in his talk on financial fraud at the 20th annual Levy Institute Hyman Minsky conference at the Ford Foundation in New York City on April 15, 2011. (transcribed by selise who deserves thanks for it in this great piece):

James K. Galbraith: Without the rule of law, the financial sector is no use to anyone except those who own it and the politicians they own

This is a fundamental fact that is at the root of either an actual understanding of our economic system and economic policy fiscal or monetary or a dangerous naive misunderstanding that will cause the next crash or two looming on the horizon. That brings me back to securitization which Tom Miller and the White House have a very poor understanding of(kind of like their understanding of the federal budget), like the concept of moral hazard which I will also get to.

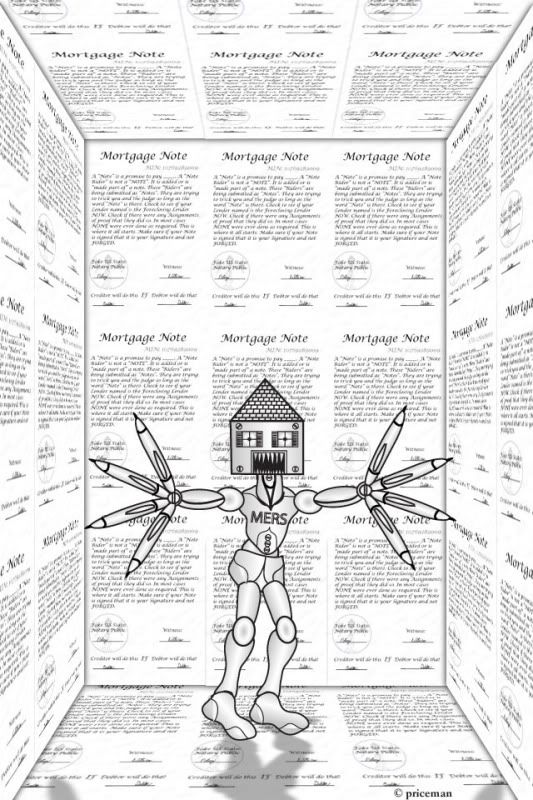

Fraud is at the heart of the securitization process. This process has been broken for some time, but with the foreclosure crisis still happening, it’s time for a refresher on what is going on in this game of "Where is the paper?" and "Where are the assignments, MERS?" Did these bankers' mind go “In Blank”?

OH Rep Marcy Kaptur was right.

They really can't find the paper up there.

(Animation by ©priceman)

Professor of Economics and Research Director of the Center for Full Employment and Price Stability, University of Missouri–Kansas City Randall R. Wray and securitization expert James McGuire show this is the case:

Why Mortgage-Backed Securities Aren't (Backed by Securities): How MERS Toasted the Banks

(original art by ©priceman)

(original art by ©priceman)

1. A valid "mortgage" requires a ("wet signature") note and a security instrument; these must be kept together, and any subsequent transfer of lien rights to the security instrument must be recorded at the appropriate public office. The mortgage note must be properly indorsed each time the mortgage is transferred. In the era of securitized mortgages this can be a dozen times or more. If ever presented for foreclosure, endorsements should demonstrate a clear chain of title, from origination through to foreclosure; and this should match the records at the public office.

2. MERS intended to provide an electronic registry of all mortgages. By appointing a "vice president" in every financial firm, it believed that all transfers of lien rights among these firms were "in house". Hence it operated on the belief that no subsequent public recording was necessary, and no further endorsement of the mortgage note was necessary for in-house transfers of the payment intangible as it kept a record of transfers of the mortgage. It claimed to be a nominee of these firms (purported to hold the mortgage) but also to be the holder of the mortgages including the "Unidentified Indorsees In Blank" -- mortgages that were never properly endorsed over to purchasers. We know, however, that MERS recommended that mortgage servicers retain notes, so MERS's claim to be the holder rests on its claim that appointed VPs are employees. But these employees are not an agent/employee of the "Unidentified Indorsee In Blank", nor are they paid by MERS or in any way supervised by MERS.

3. This practice is in violation of numerous laws. Property law requires filing sales in the public record. Notes must be affixed (permanently) to the security instrument -- a mortgage without the note has been ruled a "nullity" by the Supreme Court. MERS's recommended business practice (with the servicer retaining the note) would make the mortgages a "nullity". A complete chain of title is required to foreclose on property -- every sale of a mortgage must be endorsed over to the purchaser, and properly recorded. Without this, it is illegal to foreclose on property -- no matter how many payments the homeowner has missed.

Further proof on just how inept Iowa AG Tom Miller's view on how we just need to wait to address our broken securitization process in conjunction with a failed Too Big to fail financial system. Only a fool or a tool would think we can address this later. Securitization was one of the many important aspects that failed to be addressed by the lackluster Dodd Frank pseudo financial reform bill.

As of now securitization lacks broadly defined standards at every turn and is full of asymmetrical information. (What Joseph Stiglitz won his Nobel prize in pointing out) among numerous other problems Joshua Rosner lays out in this excellent presentation.

Securitization

Taming the Wild West

Joshua Rosner

Joshua Rosner on Securitization from Roosevelt Institute on Vimeo.

Contracts that Work

We also need to address the lack of uniformity in the contractual obligations

between various parties to a securitization. “Pooling and Servicing Agreements” (PSAs) and “Representations and Warranty” terms can be several hundred pages long. They define features like the rights to put back loans that had underwriting flaws, the responsibilities of servicers, and the relationship between the different tranches. In addition, key terms that define contractual obligations are not standardized across the industry, across issuers of securities with the same

type of collateral (e.g. RMBS, CMBS or RMBS based CDOs) or even by issuer

(each issuer often had several different Pooling and Servicing Agreements and

Representation and Warranty Agreements).

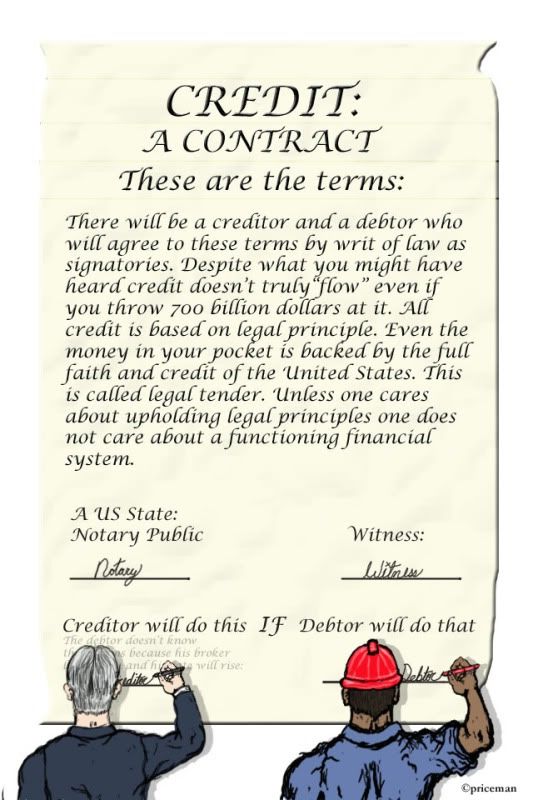

That brings me to my next point which should be obvious by now, but again I will refer to the brilliant James K. Galbraith who warned us there would be No Return to Normal. President Barack Obama stated we needed son of TARP and the PPIP bailouts on top of TARP in order to "get credit flowing again." That never truly happened, but there is a reason:

(original art by ©priceman)

(original art by ©priceman)

The oddest thing about the Geithner program is its failure to act as though the financial crisis is a true crisis—an integrated, long-term economic threat—rather than merely a couple of related but temporary problems, one in banking and the other in jobs. In banking, the dominant metaphor is of plumbing: there is a blockage to be cleared. Take a plunger to the toxic assets, it is said, and credit conditions will return to normal. This, then, will make the recession essentially normal, validating the stimulus package. Solve these two problems, and the crisis will end. That’s the thinking.

But the plumbing metaphor is misleading. Credit is not a flow. It is not something that can be forced downstream by clearing a pipe. Credit is a contract. It requires a borrower as well as a lender, a customer as well as a bank. And the borrower must meet two conditions. One is creditworthiness, meaning a secure income and, usually, a house with equity in it. Asset prices therefore matter. With a chronic oversupply of houses, prices fall, collateral disappears, and even if borrowers are willing they can’t qualify for loans. The other requirement is a willingness to borrow, motivated by what Keynes called the "animal spirits" of entrepreneurial enthusiasm. In a slump, such optimism is scarce. Even if people have collateral, they want the security of cash. And it is precisely because they want cash that they will not deplete their reserves by plunking down a payment on a new car.

Legal tender is the foundation of our currency. Contractual obligations upheld by law are the foundation of credit. Credit is the foundation behind all securities bought and sold on the FOMC everyday which includes RMBS, CMBS, and all ABS on the Fed's balance sheet, especially the NY Fed. So unless one cares about upholding rule of law in economics as well as foreign and domestic policy, there is nothing to base our system on in the long run. Why? Well because:

There may be some who wonder why I have to involve the president in all of this, but there are multiple reasons, some of which I already laid out fairly clearly(despite the obvious regarding civics and criticizing our Representatives who work for us which is what our Republic was founded upon). The president supporting the dirty banker deal will continue a failing system. The same system the courageous protesters are protesting at #occupywallstreet. The president has the largest podium and is the most ubiquitous force in our lives, like it or not so it matters what he says.

So when he speaks economic nonsense, like Iowa AG Tom Miller who assumes we can go half-ass on confronting the issues of criminology and control fraud now while pretending we can confront Wall Street later, it harms this movement and thier push to right what was wronged. For instance when the president said this about D grade financial reform:

"Finally, because of this law, the American people will never again be asked to foot the bill for Wall Street's mistakes. There will be no more taxpayer funded bailouts. Period. If a large financial institution should ever fail, this reform gives us the ability to wind it down without endangering the broader economy. And there will be new rules to make clear that no firm is somehow protected because it is "too big to fail," so that we don't have another AIG."

http://www.marketwatch.com/...

It's dangerous ahistorical economic nonsense and it hurts all of the 99%. Former IMF and MIT economist Simon Johnson's(13 Bankers/Baseline Scenario) paper explains why:

Governments may now promise not to provide further bailouts, but in the view of Alessandri and Haldane (2009, p.7) – from the Bank of England – such promises are unlikely to be believed: "Ex-ante, they [the authorities] may well say "never again". But the ex-post costs of crisis mean that such a statement lacks credibility. Knowing this, the rational response by market participants is to double their bets. This adds to the costs of future crises. And the larger these costs, the lower the credibility of ‘never again’ announcements."

In contrast, the current consensus in US official circles is that the government can commit not to bail out large firms. For example, in the Dodd-Frank financial regulation bill (signed into law on July 21, 2010) there is a "resolution authority" that allows a regulatory agency (the Federal Deposit 1 "Too big to fail" is far from a new issue, as discussed in detail by Stern and Feldman (2004) – in the modern American context, it dates from at least the conservatorship of Continental Illinois in the 1980s.

snip

Can such a "no bailout" government policy constitute a credible commitment that solves the problem of "too big to fail"? Ex ante promises to let companies fail – and run through some form of bankruptcy – may not be optimal when the moment for a decision actually arrives. In particular, given the "systemic" nature of financial crises – with widespread perceived contagion both within and across countries – will financial markets really believe any government when it promises not to save

its biggest firms?

Recent experience in South Korea suggests an answer: No. When financial crisis broke out at the end of 1997, the banking system was threatened with collapse and the exchange rate depreciated rapidly. At this time of crisis, government policy was explicitly and emphatically not to bailout the largest Korean conglomerates (known as chaebol), which were heavily leveraged and exposed to the ensuing financial crisis. This approach was rooted in the incoming president’s long-standing dislike for and opposition to the political power of large chaebol, and the authorities attempted to make the firmest and most credible commitments in this regard, including through its agreements with the International Monetary Fund.

Despite this, the largest conglomerates ("chaebol") were able to borrow heavily from households through issuing bonds at low interest rates in 1998 – allowing many of them to avoid immediate failure and become even bigger relative to the economy. The largest conglomerates issued disproportionately more bonds than other firms and were able to do so at rates implying much lower default risk. There is no evidence that this advantageous access to finance was due to better historic performance, stronger prospects, or better governance within the biggest firms – if anything, all objective measures suggest that the largest conglomerates were actually in worse shape (apart from their presumed implicit government backing) relative to other Korean firms.6 Instead, the most plausible interpretation is that investors perceived these large firms as "too big to fail". Investors’ perceptions proved largely correct. Daewoo, Korea’s third largest conglomerate, declared bankruptcy in 1999, and Hyundai, Korea’s largest conglomerate, also had a de facto default in 2000. And in both cases, the Korea government, fearing another economic crisis, intervened so as to effectively and largely bail out the bond investors.7

It was a lie and the president had a chance once he was first elected to pass real financial reform; a real bank rescue involving temporary nationalization and access to their books, accountability for the CEOs, and ending Too Big to Fail which is at the heart of all of these problems. The same problems that were solved for 50 years in FDR's first 100 days with his 1933 banking reforms including Glass Steagall and the creation of the FDIC were passed shortly after he was almost assassinated. That is until it was systematically destroyed by Citibank lobbyists on the Federal Reserve Board in the 80s and Third Way Democrats and Republicans in Congress in the 90s(signed into law by a Third Way President).

So unless we focus on the one man who is fighting the big moneyed interests taking on the systematic problems behind the whole crash of 2008 and the foreclosure crisis right now, there won't be a chance later and we know this by economic history and data.

Let's support and voice support for NY AG Eric Schneiderman while occupying Wall Street and cities across the country. Even if you are more sympathetic to the president and Democrats in Congress than I am, but you want to help out #occupywallstreet, demand our leaders support NY AG Eric Schneiderman. Do so, so we can have some real accountability for what Wall Street has done to our country and to the global economy.

Otherwise electoral politics means very little in the grand scheme of things.