I'm on the road again, and consequently was not able to repost this here when it first appeared on Naked Capitalism last week. I originally wrote it for Real Economics, but a series of excellent questions by Lambert Strether at CorrenteWire led to a much revised and expanded article.

Bill Neilâ's most recent exegesis, The Costs of Creative Destruction: Wendell Berry vs. Gene Sperling, provides a devastating critique of the economic thinking of Democratic Party elites, using as a foil Sperling's speech before the National Press Club on March 27, 2012. Sperling is Chairman of President Obama's Council of Economic advisors, and his speech was entitled "Renaissance of American Manufacturing." Neil writes:

It was Sperlingâs statement, though, that in the decades which we think of as witnessing our deindustrialization, from 1965-1999, the nation had a fairly steady component of about 17.3 million manufacturing jobs. For someone who had seen the factory shells and crumbling walls of manufacturing districts in Philadelphia, Camden and Newark close up, and had worked as a social worker in old industrial Trenton, NJ during the 1970âs, this was an astounding claim. Once again, just as I felt when I came of political age during the Vietnam War, I was at odds in a great "accounting dispute" over "costs" with the nation's best and brightest. How could this economist who had served in Democratic administrations, advance such a blasé base line on manufacturing jobs, for the very years when a key part of that party's base, organized labor, and the working class, were being evicted from middle class Main Street?

(Here is the link to Part I: The Hidden History of Deindustrialization; the links to the remaining three parts are at the end of this post.)

One of the first links Neil provides is to a stunning March 2012 report, Worse Than the Great Depression: What Experts Are Missing About American Manufacturing Decline, by the Information Technology and Innovation Foundation, which refutes the common wisdom that the loss of U.S. manufacturing jobs is because of gains in productivity. If new, more productive manufacturing technology is the primary reason for the loss of manufacturing jobs, then we should be seeing a pattern of rising capital investment in that technology. But there is no such pattern. In the chapter entitled, "Capital Investment Trends in U.S. Manufacturing", the study notes:

A more accurate measurement of U.S. manufacturing output suggests that superior productivity was not principally responsible for the loss of almost one-third of U.S. manufacturing jobs in the 2000s. If it were, we would also expect to see a reasonable increase in the stock of manufacturing machinery and equipment, for it is difficult to generate superior gains in productivity without concomitant increases in capital stock. Conversely, if loss of output due to declining U.S. competitiveness caused the decline of jobs, we would more likely see flat or declining capital stock. In fact, we see the latter, which is more evidence for the competitiveness failure hypothesis.

U.S. Manufacturing Capital Stock is Stagnant

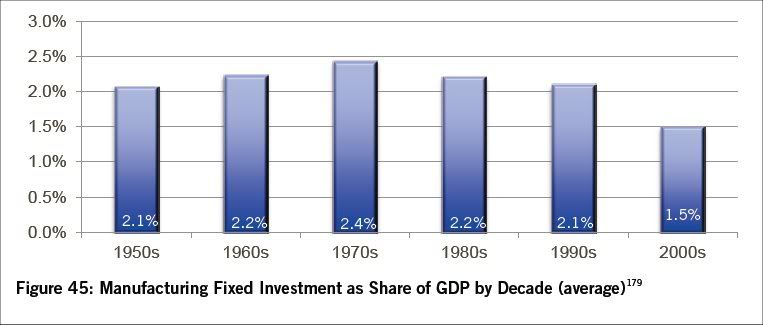

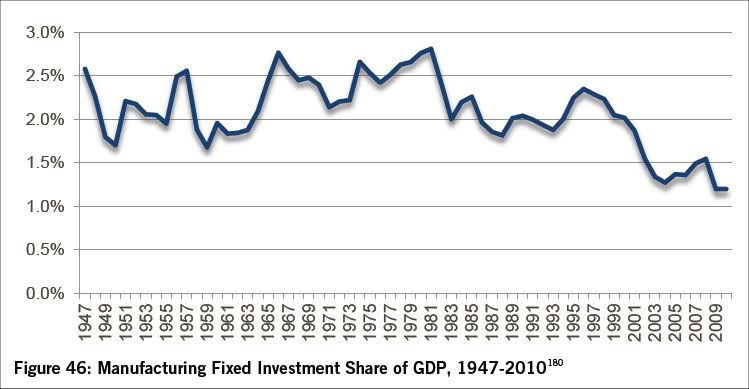

Over the past decade, as Figure 45 shows, the overall amount of fixed capital investment (defined as investment in structures, equipment, and software) made by manufacturers as a share of GDP was at its lowest rate since World War II, when the Department of Commerce started tracking these numbers. An analysis by year shows that the annual rate has generally declined in the 2000s, going under 1.5 percent for several years for the only time since 1950. (See Figures 45 and 46) This decline represents the decreasing amounts invested, on average, in new manufacturing plants and equipment every year.

These two graphs show clearly show the decline in capital investment in manufacturing.

But if these were adjusted to a per capita basis, the trend would be even worse, because of growing population. This is important, because it means that as a nation, the United States is becoming less capital intense. It is becoming, in other words, less capitalistic. This is a symptom, as well as a function, of the U.S. economy coming to be dominated by rentiers and usurers, rather than producers. On these grounds is the most devastating critique of Mitt Romney's Bain Capital: their private equity operations, forcing companies to borrow money to pay out fees and dividends to Bain, actually de-capitalize those victim companies. But President Obama and Democratic Party elites are unable and unwilling to attack Romney and Bain on these grounds. The reason, of course, is that the Democratic Party is as much in thrall to rentiers and usurers as the Republican Party is. More on this later.

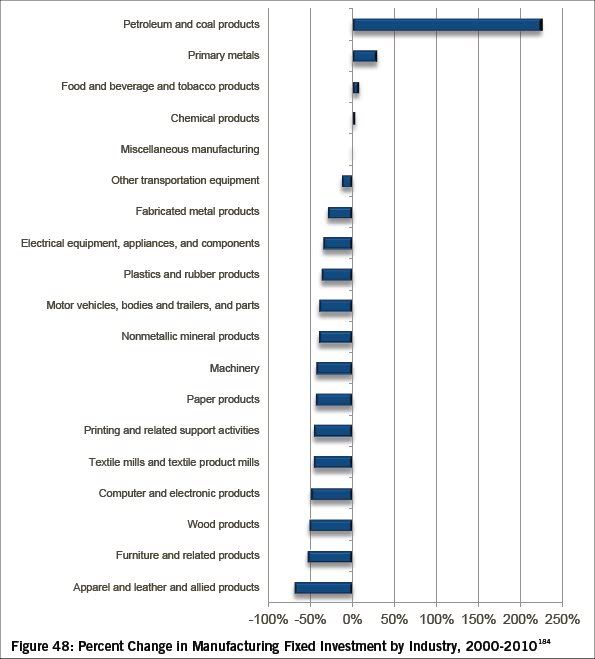

The next graph, providing a break down of capital investment by industrial sector, is extremely important, because it shows that almost all the positive growth in capital expenditures is accounted for by one, huge industry – oil and gas. All other manufacturing industries except primary metals, chemicals, and food and beverage products show negative rates of capital investment. Again, in other words, de-capitalization. This is extremely important because it shows that the U.S. economy is being returned to a neo-colonial status of being a supplier of raw materials. This probably applies to the oil and gas industry, also: recall that there has not been a new refinery built in the U.S. for over three decades. So, the gains in capital investment shown by oil and gas is almost entirely for extraction.

The same trend of de-capitalization of the U.S. economy was found by Steve Roth, who reposts what he writes to the blog Angry Bear. In December 2011, Roth wrote Capital in the American Economy Since 1930: Kuznets Revisited, and reported what he had found:

The most notable and consistent postwar trend is the decline in net investment, even while gross investment remained mostly flat with slight decline, and capital consumption increased slightly. Those two small trends compound to result in the quite large (35%) decline in net investment as a percent of GDP from the 50s to the 00s.

That oil and gas are such an outlier on the graph above also shows the outsize political economy effect of the rentier influence exerted by the oil and gas industry. If we were seriously trying to address resource constraints and climate change, we would not be seeing such an outsize impact by oil and gas. There should be trillions (not merely billions) of dollars of new investment going into clean energy technologies, new energy distribution systems, retrofitting all types of structures for energy efficiency, replacing all vehicles with new, high efficiency vehicles, and so on.

This lack of investment in what the country really needs shows why government regulations are crucial. We need to have regulations and taxes that encourage economic activity that society needs, and discourage economic activity that harms society. Now, everything wrong is incentivised, while support for education and clean energies is being cut in a mad dash to austerity. We need regulations and policies that make it more profitable to invest in wind farms and solar arrays, than in credit default swaps and currency futures. In his 1973 study of the economic principles established at the foundation of the United States, The Foundations of American Economic Freedom: Government and Enterprise in the Age of Washington (University of Minnesota Press), E.A.J. Johnson wrote:

The general view, discernible in contemporaneous literature, was that the responsibility of government should involve enough surveillance over the enterprise system to ensure the social usefulness of all economic activity. It is quite proper, said Bordley [John Beale Bordley], for individuals to "choose for themselves" how they will apply their labor and their intelligence in production. But it does not follow from this that "legislators and men of influence" are freed from all responsibility for giving direction to the course of national economic development. They must, for instance, discountenance the production of unnecessary commodities of luxury when common sense indicates the need for food and other essentials. Lawmakers can fulfill their functions properly only when they "become benefactors to the public"; in new countries they must safeguard agriculture and commerce, encourage immigration, and promote manufactures. Admittedly, liberty "is one of the most important blessings which men possess," but the idea that liberty is synonymous with complete freedom from restraint "is a most unwise, mistaken apprehension." True liberty demands a system of legislation that will lead all members of society "to unite their exertions" for the public welfare. It should therefore be the policy of government to aid and foster certain activities or kinds of business that strengthen a nation, even as it should be the duty of government to repress "those fashions, habits, and practices, which tend to weaken, impoverish, and corrupt the people." (pp. 194â195)

The very concepts of the public welfare, general welfare, and common good , of course, have been under constant attack by conservatives and libertarians since the New Deal. But these concepts were fundamental to the creation of the republic. (Please note we are not referring to "republic" as in the Republican Party, which has, since the early 1900s, transmogrified from the Party of Lincoln into the party of social Darwinism). I have, for nearly a year now, been urging people to read two books that explicate these concepts: The Ideological Origins of the American Revolution, by Bernard Bailyn, Belknap Press of Harvard University Press, Cambridge, Mass., 1967, and The Creation of the American Republic 1776-1787, by Gordon S. Wood, University of North Carolina Press, Chapel Hill, NC, 1969.

As Wood explains:

The sacrifice of individual interests to the greater good of the whole formed the essence of republicanism and comprehended for Americans the idealistic goal of their Revolution. From this goal flowed all of the Americans' exhortatory literature and all that made their ideology truly revolutionary....

From the logic of belief that "all government... is or ought to be, calculated for the general good and safety of the community,"... followed the Americans' unhesitating adoption of republicanism in 1776. The peculiar excellence of republican government was that it was "wholly characteristical of the purport, matter or object for which government ought to be instituted." By definition it had no other end than the welfare of the people: res publica, the public affairs, or the public good. "The word republic", said Thomas Paine, "means the public good, or the good of the whole, in contradistinction to the despotic form, which makes the good of the sovereign, or of one man, the only object of government."

....In a republic "each individual gives up all private interest that is not consistent with the general good, the interest of the whole body." For the republican patriots of 1776 the commonweal was all encompassing—a transcendent object with a unique moral worth that made partial considerations fade into insignificance. "Let regard be had only to the good of the whole" was the constant exhortation by publicists and clergy. Ideally, republicanism obliterated the individual. “A Citizen,” said Sam Adams, “owes everything to the Commonwealth.” “Every man in a republic,” declared Benjamin Rush, “is public property. His time, his talents—his youth—his manhood—his old age—nay more, life, all belong to his country.” “No man is a true republican,” wrote a Pennsylvanian in 1776, “that will not give up his single voice to that of the public.” (pp. 53-61)

Neo-liberalism in economic policies can never be anything else but an abdication— repudiation, really—of this Revolutionary concept of republicanism. In fact, when the Information Technology and Innovation Foundation report derides "egregious foreign mercantilism policies," it is demonstrating a crippling lack of understanding of what the American republic is supposed to be. Policies favoring and promoting a nation's industries, and the earning power of its people, are an essential part of republican statecraft. These policies were explicitly laid out in first Treasury Secretary Alexander Hamilton's series of reports to Congress on banking, credit, and manufactures. While Hamilton's report on manufactures initially received a cold response, many of its policies were later enacted after the War of 1812 showed again how important it was for the United States to control its own industrial base. But in the general sense, of the battle between Hamilton and Jefferson (over whether the United States would remain a agrarian in nature, or would develop capital markets as it industrialized), it should be stressed that Hamilton's vision was of a nation developing its industries and becoming ever more capital intensive. And Hamilton was fully supported by President Washington.

With the de-capitalization shown in the above graphs, with the de-capitalization of Mitt Romney and Bain – and the hedge fund managers who fund the Democratic Party – we are moving rapidly away from the vision and policies of Washington and Hamilton for a more capital intensive economy. This of course begs the question of what are the differences, if any, between today's Republican Party and Democratic Party. To understand this, it is useful to first identify the major shift in economic paradigms that occurred in the 1970s and 1980s. For this, we turn to former AFL-CIO economist Thomas Palley, who has recently published what looks to be the most important book of the year, From Financial Crisis to Stagnation: The Destruction of Shared Prosperity and the Role of Economics:

...the roots of the financial crisis of 2008 and the Great Recession can be traced to a faulty U.S. macro-economic paradigm that has its roots in neoliberalism, which has been the dominant intellectual paradigm. One flaw in the paradigm was the growth model adopted after 1980 that relied on debt and asset price inflation to drive demand in place of wage growth linked to productivity growth. A second flaw was the model of engagement with the global economy that created a triple economic hemorrhage of spending on imports, manufacturing job losses, and off-shoring of investment.

The combination of stagnant wages and the triple hemorrhage from flawed globalization gradually cannibalized the U.S. economy's income and demand-generating process that had been created after World War II on the back of the New Deal. However, this cannibalization was obscured by financial developments that plugged the growing demand gap.

Financial deregulation and financial excess are central parts of the story, but they are not the ultimate cause of the crisis. Financial developments contributed significantly to the housing bubble and the subsequent crash. However, they served a critical function in the new model, their role being to fuel demand growth by making ever larger amounts of credit easily available. Increasing financial excess was needed to offset the increasing negative effects of the model of growth and global economic engagement that undermined the demand-generating process on which the U.S. economy depended.

As Palley explained in The Debt Delusion in February 2008 (before the collapse of Bear Sterns laid bare the rot within the financial system):

America's economic contradictions are part of a new business cycle that has emerged since 1980. The business cycles of Presidents Ronald Reagan, George H.W. Bush, Bill Clinton, and George W. Bush share strong similarities and are different from pre-1980 cycles. The similarities are large trade deficits, manufacturing job loss, asset price inflation, rising debt-to-income ratios, and detachment of wages from productivity growth.

The new cycle rests on financial booms and cheap imports. Financial booms provide collateral that supports debt-financed spending. Borrowing is also supported by an easing of credit standards and new financial products that increase leverage and widen the range of assets that can be borrowed against. Cheap imports ameliorate the effects of wage stagnation.

This structure contrasts with the pre-1980 business cycle, which rested on wage growth tied to productivity growth and full employment. Wage growth, rather than borrowing and financial booms, fueled demand growth. That encouraged investment spending, which in turn drove productivity gains and output growth.

In an interview about his new book, Palley identified three political groupings according to their view of the financial crises, its causes, and proposed solutions:

Broadly speaking, there exist three different perspectives. Perspective # 1 is the hardcore neoliberal position, which can be labeled the "government failure hypothesis". In the U.S. it is identified with the Republican Party and the Chicago school of economics. Perspective # 2 is the softcore neoliberal position, which can be labeled the "market failure hypothesis". It is identified with the Obama administration, half of the Democratic Party, and the MIT economics departments. In Europe it is identified with Third Way politics. Perspective # 3 is the progressive position which can be labeled the "destruction of shared prosperity hypothesis". It is identified with the other half of the Democratic Party and the labor movement, but it has no standing within major economics departments owing to their suppression of alternatives to orthodox theory.

The government failure argument [#1] holds the crisis is rooted in the U.S. housing bubble and bust which was due to failure of monetary policy and government intervention in the housing market. With regard to monetary policy, the Federal Reserve pushed interest rates too low for too long in the prior recession. With regard to the housing market, government intervention drove up house prices by encouraging home ownership beyond peoples' means. The hardcore perspective therefore characterizes the crisis as essentially a U.S. phenomenon.

The softcore neoliberal market failure argument [#2] holds the crisis is due to inadequate financial regulation. First, regulators allowed excessive risk-taking by banks. Second, regulators allowed perverse incentive pay structures within banks that encouraged management to engage in "loan pushing" rather than "good lending." Third, regulators pushed both deregulation and self-regulation too far. Together, these failures contributed to financial misallocation, including misallocation of foreign saving provided through the trade deficit. The softcore perspective is therefore more global but it views the crisis as essentially a financial phenomenon.

The progressive "destruction of shared prosperity" argument [#3] holds the crisis is rooted in the neoliberal economic paradigm that has guided economic policy for the past thirty years. Though the U.S. is the epicenter of the crisis, all countries are implicated as they all adopted the paradigm. That paradigm infected finance via inadequate regulation and via faulty incentive pay arrangements, but financial market regulatory failure was just one element.

Palley's overall schema of the shift from an economy based on rising wages and increased productivity, to one based on inflation of assets and increased debt, is another way of describing how the U.S. economy is being made less capital intense, or de-capitalized. If a corporate raider or "private equity partner" is able to gain control of an industrial company for $1 billion, and is able to break it apart and sell it piecemeal for $1.2 billion, the nation's capital intensity has NOT been increased. The stock of capital did NOT increase by $200 million, contrary to all the numbers on all the financial statements dutifully reported by the dupes of the financial press. And this is an extremely simple example. Reality is more often characterized by complex financial arrangements that, when boiled down, amount to asset stripping and outright de-capitalization through imposing debt. These are not new tactics: Donald Bartlett and James Stewart detailed this financial piracy in a nine-part series originally published by the Philadelphia Inquirer over two decades ago, in October 1991, which was published as the book America: What Went Wrong?. (Look especially at Chapters 8 and 9.)

True republican statesmanship depends on a more than passing familiarity with the frontiers of science and technology, and a firm understanding of the economic problems that need to be solved, because republican statesmanship requires the economic incentives of society be structured in such a way as to encourage the application of the leading edges of science and technology to solving those problems. Without promotion and directed application of the leading edges of science and technology, a society is doomed to crash into the constraints of its natural environment – with the catastrophic results Jared Diamond writes about in his book, Collapse: How Societies Choose to Fail or Succeed. If society fails to steer the flows of credit and money creation into socially useful economic activities, this technological imperative makes social collapse inevitable. This is really nothing new: all the great texts of the world's religions offerexamples of what happens when a society allows itself to fall under the control of an oligarchy of rentiers and usurers. Combine this social imperative with what we now know about the requirement for scientific and technological progress – for example, climate science – and we see how the rise of "special interests" that are basically rentiers and usurers, fundamentally clash with the intended political economy of a functioning republic. At some level, the Founders understood this: they identified the two greatest threats to the survival of a republic as a standing army, and the rich. De-capitalization and de-industrialization are wrecking not just the economy, but the nation as a self-governing republic. It is no coincidence that the words plutocracy and oligarchy – both deadly enemies of republicanism – have come to be used more and more often as we discuss and debate our system of political economy today.

This is a greatly expanded version of what first appeared as US Manufacturing: "Worse Than the Great Depression" on Real Economics.

The last three parts of Bill Neil's The Costs of "Creative Destruction": Wendell Berry vs. Gene Sperling are:

Part II: Wendell Berry Applies Conservative Classical Christian Humanism to the Economy

Part III: The Search for Community in the 1930â²s

Part IV: The American Left in the 2nd Great Crisis of Capitalism....2008...???