Crossposted from Blue Indiana

Anyone who's bee watching the new lately knows that there's something of a property tax revolt going on in Indiana. Hundreds of thousands of Hoosiers have seen their property tax bills skyrocket, and if you follow the media narrative, you'd think that there's been a massive growth in government spending that's at fault here. The truth though is that there hasn't been a tax increase in Indiana, but there has been a massive

tax shift.

"Statewide, increased local spending has almost nothing to do with it," said Larry DeBoer, an agricultural economist at Purdue, explaining why many homeowners' property taxes are skyrocketing. "Statewide, this is almost entirely a tax shift from one set of taxpayers (business and industrial) to others (homeowners)."

Homeowners are seeing dramatic tax increases because business inventory is now exempt from property taxation, the Legislature capped property tax replacement credit subsidies to local government, and the assessed value of homes for taxing purposes is now adjusted annually based on home sales data in your neighborhood, said DeBoer, an expert in state and local government public policy.

In at least two counties -- "and I think a whole lot more" -- commercial and industrial property values are mistakenly not being adjusted annually, DeBoer said in an interview.

How Indiana Gave Working Hoosiers The "Shift"

Dr. DeBoer has identified the two principle drivers behind the shift in property tax burden to residential owners.

The first issue is the decision by the Indiana egislature to end the inventory tax. The 2002

tax restructuring established a 100% exemption on assessed value starting on 2006 (payable 2007) tax bills. This has shifted taxes previously paid by business to residential property owners.

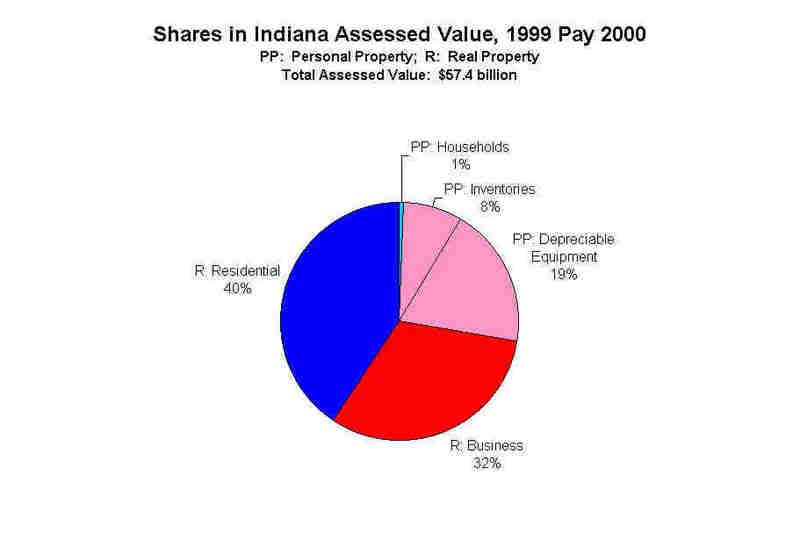

Just to give you an idea, under the old rules the

inventory tax alone accounted for 8%

of the property tax levy, meaning that ending the inventory tax, meant shifting that 8% from companies holding inventory onto the rest of the assessed value in a county. This shifted the burden of property taxes onto residential property holders. I've included a pie chart from the linked page below.

One thing that I am unclear on is whether the personal property tax on depreciable equipment has been exempted from the property tax levy as well. This represented 19% of the total levy in 1999, meaning that if it has been exempted as well, almost a full third of the assessed value has been exempted. This would represent an even larger shift from businesses to residential property owners.

The second issue raised by Dr. Deboer is the apparent failure to reassess commerical and industrial property values in the same manner as residential properties. The 1998 Town of St. John decision lead to a change in the way that property value was assessed away from a "true value" system to one that more closely reflected "market value." This created susbtantial increases in the value of older homes, and ended assessment advantages given to residential owners over businesses.

However, as was pointed

out in a recent tax hearing in Indianapolis, there have been "irregularities" in which residential properties have been taxed at substantially higher rates than their business counterparts.

John Price, an attorney who has filed a lawsuit over the current bills in Marion County, cited numerous flaws in assessing that resulted in property tax bills to businesses remaining the same while homeowners' bills soared -- a major factor in Gov. Mitch Daniels' decision to order a reassessment here.

Price noted the tax bill for three Broad Ripple banks combined was about the same as for one homeowner there. And another bank, he said, only saw its taxes go up because an assessor mistakenly classified it as a residence.

Obviously, if businesses are being systematically underassessed, the net impact will be to force the burden of the property tax levy onto residential properties. Meaning that people are going to be driven from their homes to reduce property tax bills for a few large corporations. And while there's outrage at this, the sad truth is that residential owners have long been called upon to accept higher tax rates in order to provide property tax abatemtents for economic development purposes.

A quick a dirty run through of recent news articles shows that Indiana towns and counties provide property tax abatements on a regular basis, further shifting the burden onto residential owners. Madison granted a Toyota supplier $2.6 million in property tax abatements to create 39 jobs, $67,000 for every job created. Greensburg struck a relative bargain, granting a $300,000abatement creating 80 jobs, $4,000 for every job created. Lebanon granted a $924,000 abatement to a French publisher to create 38 jobs, $24,000 per job. All these add up, and by neccesity shift the property tax burden from businesses making profits to homeowners struggling to make ends meet on shrinking wages.

Moving beyond the narrow purview of property taxes, further evidence of a massive tax shift from businesses to working Hoosiers can be found in the shrinking portion corporate share of state taxes. Since 1990, the share of state tax revenues provided by corporate income taxes has been cut in half. Only by counting riverboat taxes as corporate taxes, does the portion of state taxes born by corporations remain stable.

Shockingly, a 2004

report issued by Indiana's Legislative Services Agency (LSA) indicates that 44.3% of corporations filing tax returns in Indiana reported no income tax liability. Meaning that nearly half of Indiana corporation's paid absolutely no taxes. Again, the 7% drop in state tax revenue coming from corporate income taxes had to be made up elsewhere.

Mercifully, the introduction of riverboat gambling in this period created a new revenue stream to compensate for the loss of corporate income tax revenue. However, I think it only seems fair to question the fairness of a tax system that shifts the burden from inanimate corporations to living, breathing human beings struggling to get by.

There is another way.

A Progressive Plan for Property Tax Relief

For unto whomsoever much is given, of him shall be much required: and to whom men have committed much, of him they will ask the more.

Luke 12:48

The most fundamental argument against the fairness of any property tax is that it does not account for ability to pay. It is a regressive tax that falls disproportionately on those who can not bear the burden without going broke. In contrast, progressive taxation accounts for the ability to pay, the most well known example of this being the federal income tax. Any effort to reorganize the Indiana tax system must be based upon the guiding principle of ability to pay.

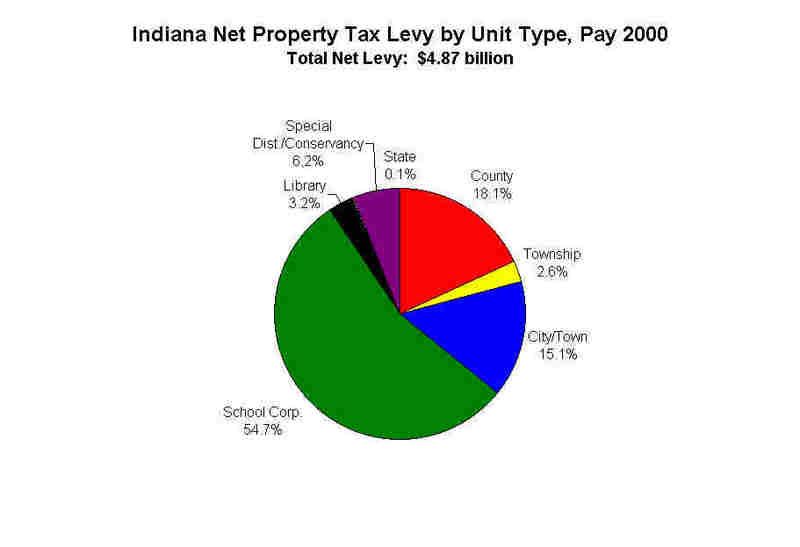

One solution frequently proposed by those on the Right is to cut spending, yet in the case of the property tax levy this involves taking money away from public education. As the graph below (taken from the Purdue Ag Econ page linked above) shows, around half of the property tax levy comes from school districts.

2004 data shows that just over half of school funding comes from the state of Indiana, while around 31.6% of total funding comes from the property tax levy. With

1,021,348 students, Indiana spent $8,431 per student in 2004, giving a total budget of $8.61 billion.

One quick, and easy way to cut property taxes in half would be to remove the burden of school funding from the property tax levy, and transfer it to the state. At 31.6% of total school funding, property taxes generated around $2.71 billion in 2004. I want to give a note of caution at this point that while I was able to locate 2005 information for income tax returns, this school spending data comes from 2004. So there will be some small discrepancy between the two.

In order to shift school funding off the property tax rolls, the state needs to find a new revenue source yielding $2.71 billion dollars annually.

One way in which to do this in keeping with the principle of ability to pay is to reorganize the state income tax along progressive principles. Currently, Indiana is one of only 6 states to have a flat income tax. This means that whether you have $1 or $1 million in Indiana gross tax income you pay 3.4%, meaning that the Indiana income tax, like the property tax, is not progressive.

Beyond being unfair, the lack of progressivity in the Indiana income tax yields little acutal income. While at the federal level the earned income tax credit means that low income individuals pay little of no income taxes, this is not true of Indiana income taxes.

It's worth noting that while individuals reporting taxable gross incomes under $20,000 represent 45.9% of a Indiana tax filings, they represent only 10% of gross taxable income. As such one quick and easy way to take the burden of property taxes off those who most need it without simply changing the form it takes, is to exempt those making less than $20,000 from the Indiana income tax.

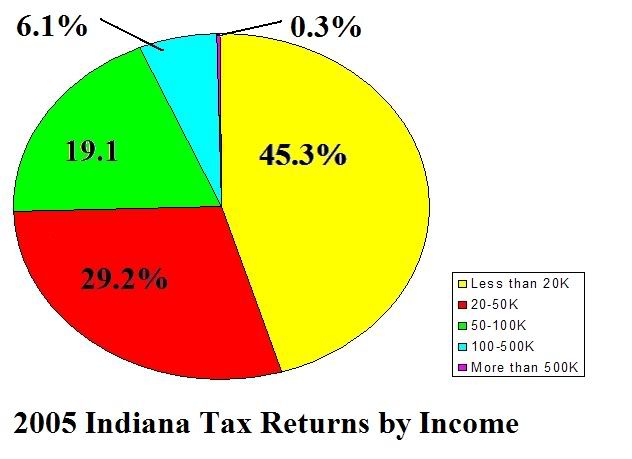

This means ending the income tax for nearly half of Hoosiers at the same time that we cut property taxes in half. I'm taking my numbers for "INDIANA ADJUSTED GROSS INCOME" line from the 2005 income tax returns. It's revealing to see the differences between the number of people filing at various income levels, and the amount of income at different income levels.

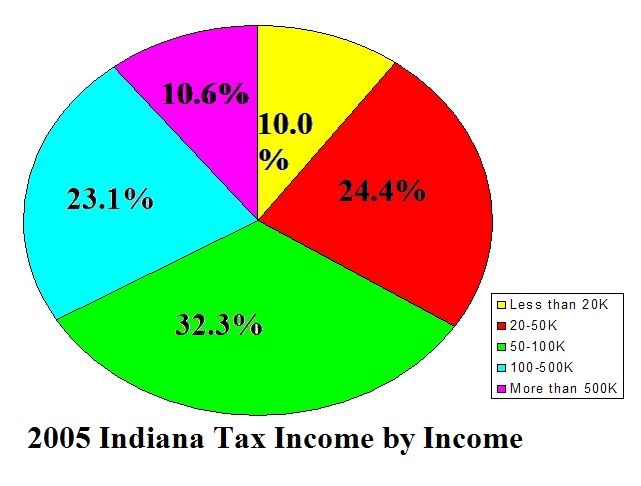

I've made a graph below showing the percentage of tax returns at various income levels. For example, this shows that 45.3% of Indiana tax returns report less than $20,000 in Indiana Adjusted Gross income, whole only 0.3% report more than $500,000 in taxable income.

A second way to look at these returns is the precentage of total state income represerented at various income levels. For example, those making under $20,000 represent only 10% of total state income, while those earning more than $500,000 represent 10.6% of total state income.

Put another ways while roughly 1.5 million people make less than $20,000, their piece of the state's income pie is actually less than the roughly 10,000 people making more than $500,000 in taxable income. You read that right, the top 0.33% represent earn more income that the bottom 45.3%. Yet, under the current income tax system that pay the same tax rate. That hardly seems fair.

By establishing a progressive tax system, we can cut property taxes in half at the same time that we end or keep the current rate steady for 3 out of 4 Hoosiers.

Just as a first go to start the discussion off, here's the new income tax schedule I'd propose.

Less than $20,000 0%

$20,000-$50,000 3.4% (Same as current rate)

$50,000-$100,000 6.0%

$100,000-$500,000 8.0%

More than $500,000 10.0%

This would yield $2.86 billion dollars in new revenue for the state, allowing the state to assume responsibility for school funding. This in turn would allow property tax bills to be cut nearly in half. I see this as an immediate fix, but I would like to throw out a few other ideas to lower the tax burden facing most Hoosier taxpayers.

- To pass a state law requiring that all future property tax abataments be subject to a binding referendum in the affected taxing jurisdiction, so that homeowners are aware of the tax burden being shifted onto them by business. In time, this would allow for property tax rates faces homeowners to be lowered even more dramatically.

- The immediate appointment of an independent auditor to examine corporate tax returns and determine if any fraud has been committed by the 44.9% of Indiana corporations claiming no income tax liability. Any money recouped by this effort could be used to lower income tax rates.

Conclusion

Working Hoosiers have been "shifted" too long, and it's about time that tax fairness, and the principle of ability to pay be reintroduced into the discussion of tax matters in this state. This is a rare moment in which the Left can show real leadership and improve the lives of working Hoosiers. If we don't, the Right will, and the "shift" will only grow larger, as those to whom much has been given refuse to pay their fair share of the state's tax burden.