Since last July, we've been treated to an unremitting series of massive subprime asset writeoffs by all of the major players in the American finance industry. As a result of the massive credit bubble and housing bubble, the two of which are closely intertwined, American financial institutions have lost virtually all credibility and American financial managers are now the butt of jokes the world over for their incompetence, their provinciality and most of all for their reckless greed.

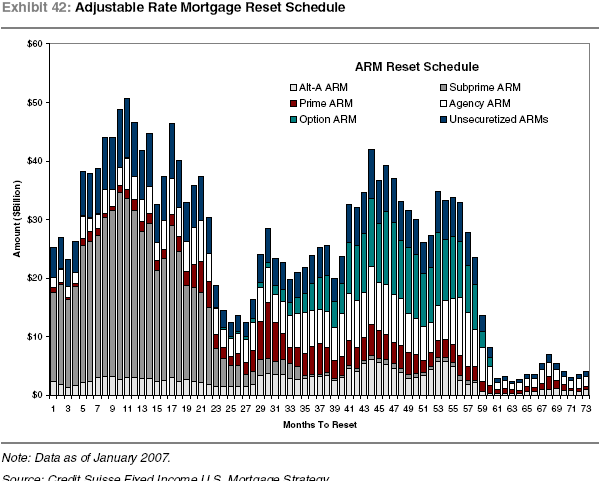

I've referred to the graphic below to illustrate how the various toxic waste loans begin to reset based on their calendar terms. As you can see, the subprime ARM market is rapidly reaching a climax, which is reached from August through October 2008:

However, other loan categories continue to fester under the general financial media radar. I'd like to direct your attention to Alt-A adjustable rate mortgages, which were bundled in the same type of securities as the subprime ARMs that have now forced nearly $200B in financial company writeoffs to date.

Another time bomb is ticking. Alt-A mortgages are a vehicle that was widely used to underwrite so-called low-doc/no-doc loans, in which self-employed and sketchily employed (possibly under the table) borrowers were vouchsafed mortgage financing, oftentimes without even a down payment.

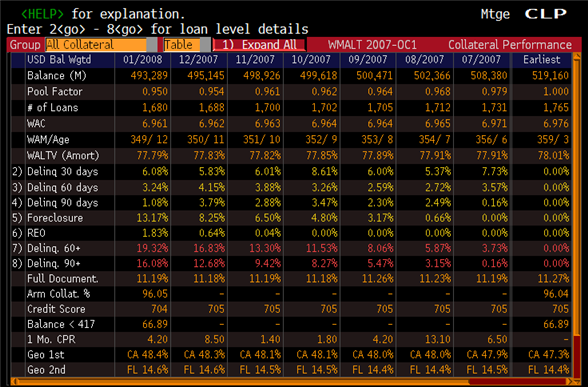

Here is a genuinely frightening graphic, culled from a commentary page from the Minyanville web site:

What you are looking at amounts to the progressive state, moving from left to right, of one of Washington Mutual's Alt-A loan portfolios.

At its peak, the entire loan portfolio for Washington Mutual was valued at $519M. Now look leftwards on Row 5 from the Earliest column, on the far right, to the last table ceel under 01/2008.

The foreclosure rate for Alt-A loans is skyrocketing. And this table does not take last month or this month into account. For January, a stunning 13.2% of this entire portfolio was in foreclosure status.

It gets worse if you look at rows 7 and 8, which are, of course, text-colored red. The deliquency levels for all remaining loans in the portfolio rapidly increase to an extremely ugly 19.3%. Looking across the chart, the month-to-month metastasization of this foreclosure rate is nothing short of astounding. A relatively quiescent securitization for Wamu is blowing up in their face in the span of seven months, with dramatic month-to-month acceleration.

In January, just about one-fifth of Washington Mutual's Alt-A loan book in this one pool was either in default or in serious jeopardy of default. Based on the number of loans in the leftmost column, a lot of people holding these loans are about to lose their homes.

And these are the numbers from just one mortgage pool, called WMALT 2007-0C1bank, from WaMu. One wonders: how many more of these do they have? And is this ugly trend going to continue?

Oh, and by the way: only 11% of these loans were originated with full loan documentation. Could this possibly be called reckless?

In a normal quarter, a distressed loan portfolio amounting to $500 million dollars would certainly be a cause for annoyance and would trigger a substantial writeoff, which a healthy bank could likely shrug off affter a quater or two.

But these are not normal times, when the entire American banking system is confronting the real possibility of financial meltdown. I'm no expert like Bonddad (as a correction below makes clear), but I am absolutely certain that this is the tip of the iceberg. These investments are scattered all over the banking system.

Banks right now cannot afford further multi-billion dollar writedowns of loan-backed bond investments in categories that up to now have not gotten a lot of press exposure.

If you're an investor in Washington Mutual, I would recommend clearing out your position stat. Washington Mutual now gazes at the possibility of an avalanche of "jingle mail," in which foreclosed and distressed borrowers simply mail their set of house keys back to the bank and walk away permanently. They are very likely seeing it take place as we speak.

Those are the seeds of recklessness, on a national scale, bearing fruit. Over 92% of this single Alt-A mortgage pool, bundled into mortgage-backed securities, was rated AAA.

This is one small bit of evidence of financial system fraud on a massive scale. Think about it: the entire American financial system was suckered into these disastrous investments by Wall Street. Using artificially cheap money, and counting on an ever-growing upward spiral of real estate values, the entire American financial system to varying degrees availed itself of a completely unregulated securities market that enabled boring old home loans to be packaged into new exciting securities that could be bought and re-sold multiple times over to pump up the quaterly balance sheets.

The original bundlers of these securities really need to be thrown in prison.

The bond rating agencies in this country (Moody's, Standard and Poor, etc...) have forfeited all credibility. Anytime you see a pronouncement, such as S&P's last week, that we may be nearing the end of the writedown cycle, just discard it as noise.

I repeat: this market was completely unregulated and ignored by the Feds. Companies such as Bear Stearns were in this market up to their eyeballs, and did massive work to build the mortgage securities market. Alan Greenspan was warned about the danger of this market years ago, and yet refused to do anything, not even to describe the possible hazards to Congress. No, to him these were financial "innovations" that helped deliver the American Dream to more families than ever.

As far as I'm concerned, the first person to be tried for fraud should be Alan Greenspan. Followed closely by Stanley O'Neal (ex-CEO of Merrill Lynch), Charles Prince (ex-CEO of Citigroup) and former Bear Stearns CEO James Cayne when they were pumping up the MBS/CDO market like the Sorcerer's Apprentice.

Meanwhile, our so-called President engages in behavior that makes Herbert Hoover seem engaged and focused on his job.

This is what the President thinks of you:

Nothing substantive will be done by the federal government while this poltroon is still in office. The stimulus? Throw it in the bank. If you absolutely do not have to spend it, don't. That's all the help you'll get from the Rethuglicans in the White House.

***Update*** Our friend I Have The Nuts provides an extremely useful correction in the comments below:

You've added together numbers you shouldn't have. The two numbers in red are calculated as follows. First:

(Delinq 60+) = (REO + Foreclosure + (Delinq 90 days) + (Delinq 60 days))

The total 60 day or over delinquency rate in the pool is stated as 19.32%, which does equal 1.83% + 13.17% + 1.08% + 3.24%.

Second:

(Delinq 90+) = (REO + Foreclosure + (Delinq 90 days))

And the total 90 day or over delinquency rate is stated as 16.08%, which does equal 1.83% + 13.17% + 1.08%.

The fact that this pool in January had 16.08% delinquent over 90 days and 19.32% over 60 days is quite bad.

So I'm correcting my numbers here. Thanks, Nuts. :)

***2nd Update*** Another commenter, ProdigalBanker, sums up the situation quite well:

"We are all subprime now". I wish I could claim credit for this one, but CR over at Calculated Risk owns it.

The takeaway here is that the perception of risk has shifted violently away from the risk free environment c. 2005 to something that is dark and scary.

Alt-A, subprime, CDOs, all of these categories are nothing more than a chapter in a global liquidity and solvency crisis. Uncle Alan telling everyone to buy a house using an ARM, transactions that made no financial sense beyond what fees could be generated, buying derivatives without reading the language in the documents, and the insatiable need to finance not only the Iraq War, but the Pottery Barn lifestyle so many Americans were taught to aspire to all have their roles in this soon to be sordid tale.

There is little the government can do. Interest rate cuts will crush the dollar, not that Helicopter Ben really cares, and drive inflation sky high - I have no clue as to how big an Expedition's gas tank is, but with regular gas heading well north of $4, what's left of the home equity loan is going to go to filling up that beast. If there is no additional liquidity, most of the major investment houses will be exposed as being insolvent, opening up an economy sized can of worms when those derivative contracts mentioned above start having to be unwound.

With JP Morgan buying Bear for less than the cost of Bear's headquarters, the global financial system dodged a bullet today. More problematic is that the run on the dollar is just gettting underway, and the US faces a Hobbesian choice of sky high inflation from increasing the money supply, or sky high interest rates from defending the dollar.

Damned if we do, damned if we don't. We are all subprime now and for the foreseeable future.

Couldn't say it better myself. I'm inclined towards mild disagreement regarding the interest rate cuts, however. Obviously it will hammer the dollar. But my guess is that along with the Fed's other moves, it's the least bad option among the sea of bad options that present themselves. There is a side benefit: American exports insensibly increase, on both the services front, manufacturing and raw materials. It will also depress imports as foreign-made goods increase in price. This process has yet to really play out but I think it will.

I also think that not every bank and brokerage is really vulnerable to this syndrome. The ones that saw through the mortgage-backed securities scam will be well-positioned to pick up huge assets for pennies on the dollar. Goldman Sachs, for example, has not been affected as yet (though it may well be this quarter), and Morgan was in a position to scoop up the large Bear Stearns asset portfolio. Many other foreign banks have not been significantly affected, with the significant exception of UBS.

It remains to be seen if the monstrous international derivatives market will begin to deteriorate as a result of the ongoing forced restructuring of the American financial community. But I think there is some decoupling going on elsewhere in the world, as China continues to grow and obtains more of its raw materials from other emerging economies. Brazil, Russia, China and India are growing economies with considerably less dependance on the American economy for their economic growth. This may be the situation's saving grace - that the rest of the world manages to ride out the storm more or less intact. We shall see...