As we optimistically look towards the fulfillment of our hopes of an Obama administration, it may be profitable to keep in mind the scope of the issues we face going forward. This piece is intended as a fragmentary survey of the economic state of our country, with an attempt to present the big picture in a few broad strokes and some zoom-ins to compelling pieces of the financial disaster that continues to unfold.

Our present economic degringolade set its initial roots 40 years ago in the Nixon administration, when the fortunes of the Republican Party turned firmly towards the sunlight, but really began to metastasize under Reagan. Here's a quick list of the numerous financial bubbles that have passed for economic growth over the last 30 years:

- The Junk Bond Scandal

- The Savings & Loan Scandal, fueled largely by (1)

- The first major Real Estate Bubble, ending in the early 90's, fueled largely by (2)

- The Dot-Com Bubble (the only one that actually produced something of lasting value - the Internet as we now know it)

- The Great Real Estate/Debt Securitization Bubble

All of this creates what Obama is now confronting: The Wealth Evaporation Machine.

This is the damage of effectively 30 years of Republican economic rule. We have not yet drunk the cup dry. By the end of this year, our financial system's entire risk portfolio will be almost completely nationalized. What will be the next shoe to drop? And what will happen next year? How will we pay for all this? Whatever else happens, I believe America's financial primacy is at an end. The Long Bubble is at an end.

Here's part of the whole sad story: the liquidation of the biggest Savings & Loan company in the United States.

The big question is: how can the people who marginalized the Risk Management teams at many financial institutions, and ran their respective companies into the ground in a few short years, in a scenario eerily reminiscent of the Saving and Loan scandal of the late 80's, be brought to book? We will look at three huge companies that eerily mirror one another: WaMu and Merrill Lynch, and finally Citibank.

WAMU. Who is Kerry Killinger? Well he should keep a low public profile, since he may well become this decade's answer to Ken Lay of Enron. Here is a quick bio, edited for brevity:

Kerry K. Killinger [was] the Chief Executive Officer of Washington Mutual Inc., since 1990 and its Chairman since 1991. [snip] His leadership path at WaMu began as executive vice president and later Senior Vice President for financial management, research, investor relations and corporate marketing, where he helped return WaMu to profitability in a deregulated environment.

Mr. Killinger has been a Director of SAFECO Corporation since January 2003. He serves as a Director of Simpson Resource Company and Green Diamond Resource Co. He has been a Director of Washington Mutual Inc., since 1988. He has been a Director of Simpson Investment Co., a forest products holding company, since 1997. He serves as a Trustee of The Seattle Foundation. Mr. Killinger is a national financial services retailer, serving the needs of mass-market consumers, as well as small and medium-sized businesses. He serves as a Member of Listed Company Advisory Committee of New York Stock Exchange Inc. He serves on the boards of the Financial Services Roundtable; the Washington Roundtable, the Washington Financial League, the Committee to Encourage Corporate Philanthropy, the Partnership for Learning; and the Greater Seattle Chamber of Commerce. In 2001, American Banker magazine named him its Banker of the Year.

Just Like Ken Lay of Enron. All kinds of laudable public involvements in vaguely high-minded organizations like the Partnership for Learning. Fingers in many pies. Possessor of a flawless high-end business pedigree, the perfect product of the American business school system dating back 40 years. Yet, in a few short years, this seemingly high-minded, trustworthy longtime S&L executive instituted a culture of recklessness that marginalized the risk controls built into his company. It wasn't enough that WaMu serviced individual mortgage holders and "small and medium-size businesses." No. The Bonus God had to be served.

Here is a look at a small piece of the carnage that destroyed Killinger's company:

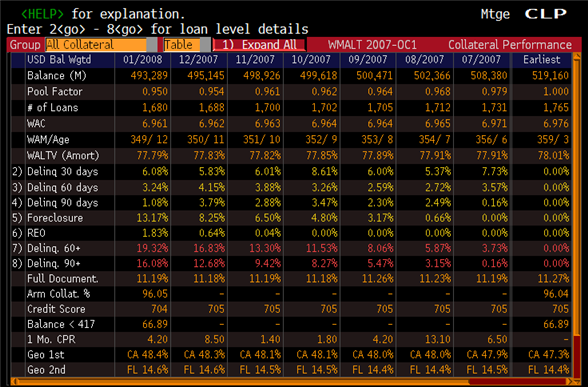

I wrote about this very subjectsome months ago, not long before WaMu exploded into shards. Below is the description of the chart you see above:

What you are looking at amounts to the progressive state, moving from left to right, of one of Washington Mutual's Alt-A loan portfolios.

At its peak, the loan portfolio for Washington Mutual in this pool was valued at $519M. Now look leftwards on Row 5 from the Earliest column, on the far right, to the last table cell under 01/2008.

The foreclosure rate for Alt-A loans is skyrocketing. And this table does not take last month or this month into account. For January, a stunning 13.2% of this entire portfolio was in foreclosure status.

It gets worse if you look at rows 7 and 8, which are, of course, text-colored red. The delinquency levels for all remaining loans in the portfolio rapidly increase to an extremely ugly 19.3%. Looking across the chart, the month-to-month metastasization of this foreclosure rate is nothing short of astounding. A relatively quiescent securitization for Wamu is blowing up in their face in the span of seven months, with dramatic month-to-month acceleration.

In January, just about one-fifth of Washington Mutual's Alt-A loan book in this one small pool was either in default or in serious jeopardy of default. Based on the number of loans in the leftmost column, a lot of people holding these loans are about to lose their homes.

And these are the numbers from just one mortgage pool, called WMALT 2007-0C1bank, from WaMu. One wonders: how many more of these do they have? And is this ugly trend going to continue?

Oh, and by the way: only 11% of these loans were originated with full loan documentation.

This is a numeric proof of the culture of risk that overtook Kerry Killinger's once-thriving company.

So, to sum up, Killinger is directly responsible for wrecking the biggest savings bank in the United States. It is, without doubt, his policies and agreements that enabled WaMu management to run a thriving financial institution onto the rocks in a few short years.

Will the elusive Killinger (whose photo is nowhere to be found anywhere on the Web) ever be held accountable for his decisions, management blunders and possible malfeasance?

Not to unduly pat myself on the back: I'm hardly the first person to point out the below:

But these are not normal times, when the entire American banking system is confronting the real possibility of financial meltdown. I'm no expert like Bonddad (as a correction below makes clear), but I am absolutely certain that this is the tip of the iceberg. These investments are scattered all over the banking system.

Banks right now cannot afford further multi-billion dollar writedowns of loan-backed bond investments in categories that up to now have not gotten a lot of press exposure.

If you're an investor in Washington Mutual, I would recommend clearing out your position stat. Washington Mutual now gazes at the possibility of an avalanche of "jingle mail," in which foreclosed and distressed borrowers simply mail their set of house keys back to the bank and walk away permanently. They are very likely seeing it take place as we speak.

And, in fact, they did see it take place. Their paper became worthless, and they went down hard, valued by Chase Morgan only for their sprawling retail networks in the western region of the country.

Balancing a huge consumer banking business with a massively leveraged securities business, Killinger built a huge two-headed monster, both of whose heads had to be continuously fed and businesses made to grow. Because of the drastically deregulated marketplace, leverage and risk were the best tools available to keep the shell game going. Given that Killinger witnessed firsthand the deregulation and destruction of the Savings & Loan business of which his company was a part and became CEO not long afterwards, it is stunning that he led his company to destruction in his turn. One has to think: ideology must play a role. People of this power, watching such things happen, inevitably blame regulation and legal restraints for their destruction.

Notes on Fannie Mae and the Auto Market

In another ugly example, Fannie Mae recently reported a massive $29 Billion (with a B) loss for the last fiscal quarter. Fannie and Freddie were by no means the worst of the financial companies involved in debt securitization; they underwrote mortgages that required documentation and a substantial down payment, and as a matter of policy only underwrite mortgages that fall into the "conforming" category. Yet, it's virtually certain that by the end of this year, a huge government bailout of both of these institutions is necessary. I think this will be the next shoe to drop after Citibank (more about Citi in a moment).

(A side note: All this while the American auto companies also are running on fumes. It appears that GM, Chrysler and Ford are all experiencing a lockout from the credit markets and being forced to burn cash on hand to meet their production expenses. When they went to ask Congress for a bailout, the top kicks of all three companies had the nerve to fly to Washington in their private jets and seemingly expected to roll over on their backs and have Congress scratch their bellies. Thank God, Congress had the sense to tell them to go away and come up with a logical plan. As Gail Collins wrote in the Times, these guys were so dim they couldn't even adequately explain themselves to people who wanted to help them!) Now, the Big Three are making another, hopefully more rational attempt tomorrow morning. As unpleasant as it is, dissolving the Big Three through bankruptcy would be the biggest union-busting act in history. Of course the three geniuses heading the auto companies may have destroyed their only chance for help:

Sixty-one percent of those questioned in a CNN/Opinion Research Corp. survey out Wednesday are dead set against the federal government providing billions of dollars in assistance the the auto makers, with 36 percent favoring such a bailout.

The poll, conducted Monday and Tuesday, also indicates that a majority of Americans, 53 percent, don't think government assistance for the auto makers will help the U.S. economy.

"Only 15 percent say that they would be immediately affected if the auto companies went bankrupt," CNN Polling Director Keating Holland said. "Seven in 10 say that a bailout would be unfair to American taxpayers."

In early November, polls indicated that nearly half the public supported federal assistance to the big auto makers when this issue first came before Congress.

Nice job, you morons.

Meanwhile, as evidence of the cratering American auto market, Parking lot after parking lot of unsold cars wait at ports around the country for dealers to take delivery. This problem affects not just the U.S carmakers, but carmakers around the world - the effects are just beginning to be felt.

Notes on the Bond Agencies

The corpses of America's biggest financial companies litter the landscape. The culture of recklessness infected virtually everyone, as this painful account of the highest executives at Merrill Lynch illustrates. This may be the first time that the primary architects of Merrill Lynch's downfall have been publicly named. Let's remember these names: Osman Semerci, the man who managed Merrill's bond unit, and Ahmass L. Fakahany, the firm’s vice chairman and chief administrative officer and the man responsible for every financial policy executed by Merrill. They formed CEO Stanley O'Neal's brain trust. Who will bring these three men to book? Is it even possible? (Yes.)

And what is at the root of all this systemic corruption? Why, the Credit Rating Agencies, of course. Moody's, Standard & Poor's and Fitch are at the very heart of this scandal. Compromised in every significant way, the rating agencies' first job was to satisfy their customers, the bond issuers--the very companies whom they are chartered to regulate. All three were and are directly funded by the very companies whose bonds they rate.

Now, this is not a terribly uncommon thing in the regulatory world; most regulatory agencies, like the FFIEC, FINRA and COSO all exist on regulatory fees levied on companies that are members of the fiefdom they regulate. The difference here is that the bond rating agencies are not non-profit or NGO-type agencies - they are private-sector firms who report earnings each quarter like everyone else. In a stunning built-in conflict of interest, the bond rating companies ginned up their quarterly numbers by waving through more and more bond issues.

One key reform should be to remove these "traffic cops" from the marketplace. Nationalize them and take away their ability to self-deal with the companies they're supposed to regulate. The problems we confront are far greater than a small group of rating agencies, but their role was intended as a final firewall to prevent fraudulent bond issues from gulling buyers looking for theat extra percentage point of earnings. If these three agencies had been doing their job, which they manifestly did not the heroin of fake AAA securities could not have spread as widely as it did.

CitiGroup

In an eerie replay from the Merrill Lynch playbook, CitiBank's disgraced CEO Charles Prince blithely ignored the gathering storm and prevented risk management officers from doing their jobs:

In September 2007, with Wall Street confronting a crisis caused by too many souring mortgages, Citigroup executives gathered in a wood-paneled library to assess their own well-being.

There, Citigroup’s chief executive, Charles O. Prince III, learned for the first time that the bank owned about $43 billion in mortgage-related assets. He asked Thomas G. Maheras, who oversaw trading at the bank, whether everything was O.K.

Mr. Maheras told his boss that no big losses were looming, according to people briefed on the meeting who would speak only on the condition that they not be named.

Unlike Washington Mutual, Citibank's risk management teams weren't repressed or bypassed; they were simply co-opted:

But many Citigroup insiders say the bank’s risk managers never investigated deeply enough. Because of longstanding ties that clouded their judgment, the very people charged with overseeing deal makers eager to increase short-term earnings — and executives’ multimillion-dollar bonuses — failed to rein them in, these insiders say.

Today, Citigroup, once the nation’s largest and mightiest financial institution, has been brought to its knees by more than $65 billion in losses, write-downs for troubled assets and charges to account for future losses. More than half of that amount stems from mortgage-related securities created by Mr. Maheras’s team — the same products Mr. Prince was briefed on during that 2007 meeting.

The Architects: Robert Rubin

What is worse, Citibank's executive corruption - there can be no other word for it - reaches into the Obama financial team:

While much of the damage inflicted on Citigroup and the broader economy was caused by errant, high-octane trading and lax oversight, critics say, blame also reaches into the highest levels at the bank. Earlier this year, the Federal Reserve took the bank to task for poor oversight and risk controls in a report it sent to Citigroup.

The bank’s downfall was years in the making and involved many in its hierarchy, particularly Mr. Prince and Robert E. Rubin, an influential director and senior adviser.

Citigroup insiders and analysts say that Mr. Prince and Mr. Rubin played pivotal roles in the bank’s current woes, by drafting and blessing a strategy that involved taking greater trading risks to expand its business and reap higher profits. Mr. Prince and Mr. Rubin both declined to comment for this article.

When he was Treasury secretary during the Clinton administration, Mr. Rubin helped loosen Depression-era banking regulations that made the creation of Citigroup possible by allowing banks to expand far beyond their traditional role as lenders and permitting them to profit from a variety of financial activities. During the same period he helped beat back tighter oversight of exotic financial products, a development he had previously said he was helpless to prevent.

And since joining Citigroup in 1999 as a trusted adviser to the bank’s senior executives, Mr. Rubin, who is an economic adviser on the transition team of President-elect Barack Obama, has sat atop a bank that has been roiled by one financial miscue after another.

Without quoting excessively from Page 4 of this damning article, it is clear that Robert Rubin bears considerable direct responsibility for the massive meltdown at Citibank. In the Clinton Administration and thereafter, Rubin was a Democratic apostle of the near-infallibility of free markets - a belief system that consistently ignored the need for clear rules of conduct and strong regulation and enforcement to minimize the damage that can be done in such a complex, interconnected, dangerously misunderstood international economic system, particularly one bearing an unprecedented shadow banking system comprised of a massively unregulated hedge fund sector and a hideously uncharted $50 Trillion+ derivatives market.

This free-market belief system has now been shown to be dangerously naive at best, amounting to a religion based around the Golden Calf of open markets. Rubin even attempts to minimize his role in this debacle:

"I’ve thought a lot about that," he said. "I honestly don’t know. In hindsight, there are a lot of things we’d do differently. But in the context of the facts as I knew them and my role, I’m inclined to think probably not."

Besides, he said, it was impossible to get a complete handle on Citigroup’s vulnerabilities unless you dealt with the trades daily.

"There is no way you would know what was going on with a risk book unless you’re directly involved with the trading arena," he said. "We had highly experienced, highly qualified people running the operation."

Yes, they did. Experienced managers like Thomas Maheras, who singlehandedly built Citi's Collaterlized Debt Obligation (CDO) business to the hundred-billion-dollar behemoth that was loaded with obscure complexity:

Yet as the bank’s C.D.O. machine accelerated, its risk controls fell further behind, according to former Citigroup traders, and risk managers lacked clear lines of reporting. At one point, for instance, risk managers in the fixed-income division reported to both Mr. Maheras and Mr. Bushnell — setting up a potential conflict because that gave Mr. Maheras influence over employees who were supposed to keep an eye on his traders.

C.D.O.’s were complex, and even experienced managers like Mr. Maheras and Mr. Barker underestimated the risks they posed, according to people with direct knowledge of Citigroup’s business. Because of that, they put blind faith in the passing grades that major credit-rating agencies bestowed on the debt.

While the sheer size of Citigroup’s C.D.O. position caused concern among some around the trading desk, most say they kept their concerns to themselves.

"I just think senior managers got addicted to the revenues and arrogant about the risks they were running," said one person who worked in the C.D.O. group. "As long as you could grow revenues, you could keep your bonus growing."

To make matters worse, Citigroup’s risk models never accounted for the possibility of a national housing downturn, this person said, and the prospect that millions of homeowners could default on their mortgages.

In last March's testimony to Waxman's Congressional Committee on Oversight and Reform, Citigroup's discredited former CEO Charles Prince goes so far as to say that Citigroup was a shining example of governance:

Over the past several

years, Institutional Shareholder Services, a leading independent analyst on corporate governance

– including executive compensation decision-making – has rated Citigroup’s corporate

governance practices in the top 10% of S&P 500 companies. In 2007, ISS rated Citigroup in the

top 2% of diversified financial services companies. ISS’s founder, Robert Monks, has described

Citigroup’s practices as "unique, cutting edge," and exceeding "the best practices currently

required by law and in the industry." Citigroup is justifiably proud of its corporate governance

practices.

The incompetence of Charles Prince as CEO of Citigroup must rank him as possibly the worst banker on the planet. After inheriting the grotesque mastodonic entity build by Sanford Weill from the merger of Citibank and traveler's Group, Prince's hands-off, heedless management style ranks him among the great incompetents in history. And Robert Rubin was at his right-hand. A man whom I like to call, simply, "Robert Ruin."

It is simply unacceptable that this man should have a role of any kind in the Obama administration!

Do a Google search for "Robert Rubin." At least on the tubes, the man is getting seriously raked.

The Architects: Alan Greenspan

In a shocking mea culpa,the the chief architect of the entire debacle reluctantly admitted his failure:

"You had the authority to prevent irresponsible lending practices that led to the subprime mortgage crisis. You were advised to do so by many others," said Representative Henry A. Waxman of California, chairman of the committee. "Do you feel that your ideology pushed you to make decisions that you wish you had not made?"

Mr. Greenspan conceded: "Yes, I’ve found a flaw. I don’t know how significant or permanent it is. But I’ve been very distressed by that fact."

On a day that brought more bad news about rising home foreclosures and slumping employment, Mr. Greenspan refused to accept blame for the crisis but acknowledged that his belief in deregulation had been shaken.

He noted that the immense and largely unregulated business of spreading financial risk widely, through the use of exotic financial instruments called derivatives, had gotten out of control and had added to the havoc of today’s crisis. As far back as 1994, Mr. Greenspan staunchly and successfully opposed tougher regulation on derivatives.

But on Thursday, he agreed that the multitrillion-dollar market for credit default swaps, instruments originally created to insure bond investors against the risk of default, needed to be restrained.

"This modern risk-management paradigm held sway for decades," he said. "The whole intellectual edifice, however, collapsed in the summer of last year."

Mr. Waxman noted that the Fed chairman had been one of the nation’s leading voices for deregulation, displaying past statements in which Mr. Greenspan had argued that government regulators were no better than markets at imposing discipline.

"Were you wrong?" Mr. Waxman asked.

"Partially," the former Fed chairman reluctantly answered, before trying to parse his concession as thinly as possible.

Really, what else is there to say about this ideologically driven creature, other than that I would not trust him with my daughter's piggy bank?

The Architects: Phil Gramm

The American financial sector is perfect evidence of what happens when a deregulatory ideology is put into practice in the real world. In A Deregulator Looks Back, Unswayed, the Sorcerer's Apprentice Phil Gramm may well be the single person most reponsible for this disaster. He remains an unrepentant true believer and the chief ideologue of financial deregulation:

In two recent interviews, Mr. Gramm described the current turmoil as "an incredible trauma," but said he was proud of his record.

He blamed others for the crisis: Democrats who dropped barriers to borrowing in order to promote homeownership; what he once termed "predatory borrowers" who took out mortgages they could not afford; banks that took on too much risk; and large financial institutions that did not set aside enough capital to cover their bad bets.

But looser regulation played virtually no role, he argued, saying that is simply an emerging myth.

A classic case of a conservative Republican refusing to accept responsibility for his actions. Let's recall that Gramm's wife sat on Enron's board! Willful ignorance is no excuse. Both Robert Rubin and Phil Gramm are cut from the same cloth, despite their respective party affiliations. Neither man can be accused of bank fraud. And the manifest incompetence of Charles Prince, Stanley O'Neal and Kerry Killinger may not rise to the level of prosecutable bank fraud.

Is there a solution for Legal redress?

I work at a technology company that develops products to help deal with IT auditing for access risk and regulatory compliance. It is here that I've first come into a small amount of knowledge of what tattered financial regulations and systems remain in place. Laws like Sarbanes-Oxley, where the CEO and CFO have to personally sign off on the quarterly results on their financial reports, have unfortunately proven useless in a deregulated market context. Prompted by the epic meltdown of Enron, in a few short years, SarBox is now shown to be woefully ineffective in an enviroment where huge financial companies operate in a largely deregulated enviroment, and where risk management teams are either repressed and ignored or simply co-opted into the corrupt system. Without risk management with teeth, and a reasonable regulatory system that stops recklessness, SarBox operates in isolation and is clearly insufficient to compel executive compliance with financial solvency and ethical business practices. However, it may be the only tool we have to bring many of these people to book.

The Sarbanes-Oxley law should be looked as a way to bring all of these men into court to be held accountable. It may be the only legal instrument available to prosecute the CEOs and CFOs of all of these failed companies, along with their handmaidens such as Robert Rubin.

Allow me to repeat myself:

It is simply unacceptable that Robert Rubin is present as part of the Obama transition team.

A man who bears direct responsibility for the deregulation of the American financial system cannot be allowed access to the corridors of power or the levers of decision-making.

He should be haled into court. And for now, Obama should fire him. Will this happen? I doubt it.

Here's why: Rubin is not alone. In fact, almost all Obama's entire economic team is directly or indirectly implicated in the Great Wealth Evaporation Machine:

As treasury secretary in 2000, Mr. [Lawrence] Summers championed the law that deregulated derivatives, the financial instruments — a k a toxic assets — that have spread the financial losses from reckless lending around the globe. He refused to heed the critics who warned of dangers to come.

That law, still on the books, reinforced the false belief that markets would self-regulate. And it gave the Bush administration cover to ignore the ever-spiraling risks posed by derivatives and inadequate supervision.

Mr. Summers now will advise a president who has promised to impose rational and essential regulations on chaotic financial markets. What has he learned?

At the New York Fed, Mr. Geithner has been one of the ringmasters of this year’s serial bailouts. His involvement includes the as-yet-unexplained flip-flop in September when a read-my-lips, no-new-bailouts policy allowed Lehman Brothers to go under — only to be followed less than two days later by the even costlier bailout of the American International Group and last weekend by the bailout of Citigroup.

It is still unclear what Mr. Geithner and other policy makers knew or did not know — or what they thought they knew but didn’t — in arriving at those decisions, including who exactly is on the receiving end of the billions of dollars of taxpayer money now flooding the system.

Confidence in the system will not be restored as long as top officials fail or refuse to fully explain their actions.

Couldn't have said it better. I know it's fundamentally unrealistic to expect Obama's newly appointed economic team to be swapped out for people who are not either morally compromised in some way or who bear histories of supporting calamitously wrong-headed policies. But is it not reasonable to expect people like Summers to own up to his screwups???

Wwhen all this is over, presuming that the antitrust system is fully restored so that Frankenstein's Monsters like Citigroup never happen again, and the financial markets are brought firmly into hand, with Glass-Steagall or a similar framework completely re-instituted as the law of the land and the hedge-fund industry brought to heel, America's business schools also must be reformed. Two generations of American business-school graduates have built and managed our financial system, and the end product is a pervasive culture of recklessness, again, spanning generations. Ethics and risk management are virtually non-existent in the upper reaches of America's business community. It's very clear, after our decade-long experiment in hands-off regulatory regimes, that our current class of business leaders from both sides of the aisle are calamitously untrustworthy.

The most powerful figures of the financial world proved to be both willful fools and destructively reckless. America's business culture is unique in its lack of morality, as is that of one of the two major political parties in this country, along with large and powerful groups within the Democratic Party. On Wall Street and all its tributaries, Bonuses Are Their God. Relatively obscure but powerful executives such as Kerry Killinger, and marquee names such as Charles Prince and Stanley O'Neal, share a common flaw: an ethical blind spot you could drive a truck through. Over the last 40 years, a culture of greed seized our country hostage. It is time that culture of untrammelled greed had a wooden stake brutally driven through its heart. As ably exhibited by the incompetent American car company executives, this stupidity pervades the entire American business community at its highest levels.

Was bank fraud committed? Can executives be held responsible with fines and jail time? Is there criminal cause, or is the entire horrible debacle the result of perfectly legal failed ideology and perfectly legal greed married to incompetence?

The fallen barons of the financial system must be held accountable. By signing off on quarterly financial statements that hid hundreds of billions of dollars of dangerous and poorly understood securitized debt instruments, these men committed violations of the Sarbanes-Oxley Act and put their companies, their shareholders and the entire world financial system at risk. They invented and agreed to a series of dangerous financial innovations, in the name of fat bonuses, that wound up destroying large sections of the American economy - and the damage is not complete yet. One can only hope that the Justice department will restore many lawyers to its ranks who are willing to prosecute many of the individuals named in this diary, because as a friend of mine who is a Berkeley law professor told me the other day, "if you look hard enough, you can always find something to take these people down with." Let the digging begin.

These people must be held accountable. Justice and fairness, and the interests of the American taxpayers and wage earners, and our country, and the world, demand it.