The "bail out" of Bear Stearns five weeks ago did nothing to solve the underlying causes of the unfolding financial meltdown, so another major crisis is unavoidable. The "bail out" of Bear Stearns has merely bought more time for the big players on Wall Street to try and drag this out past the November election, because what they fear above all else is the rise of a progressive political movement strong enough to pry loose their grasp on the credit mechanism -- the financial system -- of our economy.

The fundamental problem is the big players on Wall Street have misused the credit mechanism for their own private gains through the bloating of debt and speculation, at the expense of actually allocating and supplying capital to the real economy. This is what has caused the 30-year decline of the American industrial economy that Barack Obama observes has made many Americans bitter- a comment that was, all too typically, taken out of context by Obama’s opponents. So this diary will look at the underlying truth of Obama’s remarks, and offer some radical observations on the role of Wall Street, and what needs to be done.

The goal of the next President must be to force the financial system back into subservience to the real economy. That is the only way the myriad financial, economic, and environmental problems facing us are going to be solved. To put it more precisely, that is the only way we as a society are going to be able to muster and allocate enough financial resources to solving those problems. Of course, the big players on Wall Street are not going to meekly accept their new role. A bitter, protracted, and probably bloody period of political warfare can be expected, as the big investment and commercial banks and hedge funds are stripped of their financial power and political clout, and forced into serving the needs of the real economy once again. I have already encountered what is likely to be one response of the extremist conservatives’ – to broadly define "Wall Street" as including everyone that owns some stock, or shares in a mutual fund, or even anyone who has part of their retirement plans in a pension fund. This broad definition includes well over fifty percent of adult Americans, but it obscures the essential facts that the financial system as presently constituted does not benefit these Americans.

The pillaging of the U.S. industrial base

I will start by looking at one particular industry, footwear, because it is one of the clearest and most undeniable examples of the decline of U.S. manufacturing; and because almost everyone today attributes that decline to the impact of cheap imports. Looking at really happened shows that the demise of the U.S. shoe industry had as much to do with a cancerous financial system as with cheap imports.

Back in 1960, over 95 percent of all the shoes, boots, and other footwear used in the United States was produced here – 600.5 million pairs were produced in the U.S. in 1960, for a population of 180.6 million. In 1968, there were 204,100 workers in the U.S. footwear

industry.

A December 1992 study on "Trade Restraints and the Competitive Status of the Textile, Apparel, and Nonrubber-Footwear Industries" by the Congressional Budget Office, concluded that since the U.S. footwear industry had collapsed to only 0.06% of total U.S. employment, and pay in the industry is so low, "It would generally be more efficient for the government to allow the jobs to disappear and to compensate any displaced workers who cannot find equivalent work."

This is very typical of the failure by U.S. elites to understand that economics is all about producing what people need.

By 2004, U.S footwear production had collapsed to 35.2 million pairs, for a population of 290 million. Today, over 98% of the footwear we wear in the U.S. is imported. And as of May 2005, there were 17,340 people employed in the U.S. footwear industry. (See http://www.bls.gov/...

So, in 40 years the United States went from producing over three pairs of shoes for every man and woman and child in America, to producing one pair for every nine people. Stop a minute, look down at your feet, and think about that -- 98% of the footwear we wear in the U.S. is imported -- and what it means. The accepted economic knowledge of today is that it does not make sense for the United States to produce its own footwear because workers in China and Vietnam can produce it so much cheaper. But try looking at it this way: the world’s supposedly richest economy can NOT provide its own damn shoes. Either that economy is so incompetent that it can’t make footwear productively and efficiently enough anymore, or that economy cannot provide a wage packet that allows its people to afford to buy its own products, or that economy is simply more interested in exploiting the cheap labor of foreigners.

I suggest that reality lies in a combination of all three possibilities. But what really happened to the U.S. footwear industry? Was it really killed off my cheap foreign imports?

Here is what actually happened to one leading American shoe manufacturer, Florsheim, in the 1980s. And it has nothing to do with foreign competition and cheap overseas labor. This is from the nine-part series America: What Went Wrong published by the Philadelphia Inquirer in October 1991. Researched and written by Inquirer reporters Donald Bartlett and James Steele, the series generated the largest ever response in the Inquirer’s history – over 20,000 requests for reprints and extra copies, leading to the publication a few months later of the series in book form. Bartlett and Steele cast an unblinking eye on the financial manipulations that were remaking the American economy – at the time, celebrated in the pages of the Wall Street Journal, business school lecture halls, and $1,000 a plate political fund raisers as "unleashing the creative spirit" of American entrepreneurs. This is just one of the dozens of actual case studies Bartlett and Steele brought attention to:

Interco, Inc., a once-successful Fortune 500 conglomerate whose products included some of the best-known names in American retailing - Converse sneakers, London Fog raincoats, Ethan Allen furniture, Florsheim shoes. In that year the investment banking firm Wasserstein Perella & Co. set out to reorganize St. Louis-based Interco, a company with scores of plants operating in the United States and abroad.

Interco could trace its origins back more than 150 years. It was one of the country's largest industrial employers, with 54,000 workers. It had annual sales of $3.3 billion. It had paid dividends continuously since 1913.

In the summer of 1988, a pair of corporate raiders out of Washington, D.C., brothers Steven M. and Mitchell P. Rales, targeted Interco for takeover, offering to buy the company for $64 a share, or $2.4 billion. To fend off the Raleses, Interco's management turned to Wasserstein Perella, which came up with a plan valued at $76 a share. Interco obviously did not have that kind of cash lying around. So the plan called for the company to borrow $2.9 billion.

The financial plan was the sort that Wall Street embraced with great enthusiasm. Supporters of corporate restructurings insisted that debt was a positive force, imposing discipline on corporate managers and forcing them to keep a tight rein on costs. Said Michael C. Jensen, a professor at the Harvard Business School, who was one of the academic community's most vocal supporters of corporate restructurings, "The benefits of debt in motivating managers and their organizations to be efficient have largely been ignored."

As it turned out, Interco failed to be a textbook model for the wonders of corporate debt. Instead of encouraging efficiency, it compelled management to make short-term decisions that harmed the long-run interests of the corporation and its employees. Within two weeks of taking on the debt, Interco closed two Florsheim shoe plants - and sold the real estate. Interco announced that the shutdowns would save more than $2 million. That was just enough to pay the interest on the company's new mountain of debt for five days.

At the Florsheim plant in Paducah, Kentucky, 375 employees lost their jobs. At the Florsheim plant in Hermann, 265 employees were thrown out of work. None was offered a job at another plant.

Just enough interest to pay the new debt for five days?!? Who is really benefiting here? Certainly not the employees. Certainly not the communities those employees lived in. Did the stockholders of Interco benefit? Perhaps they made some short-term gains in the stock price of their company, but how could they have benefited in the long run? Their company no longer has the capacity to manufacture anything. If you can’t produce something, how can you sell it? If you can’t sell something, how do you obtain revenue?

Oh, yeah, you borrow.

So, it’s the money changers and money lenders that benefit.

I selected the example of Interco to show that it was not really foreign competition, but the machinations of a financial system that had broken free of it subservience to the real economy of production and distribution, that began to undermine the U.S. industrial base. And I selected the footwear industry in particular, to debunk the notion that it was cheap imports that were to blame.

In a delightful post on European Tribune about The Greatest Generation--economics division, Techno related how in the early 1960s he had helped build a three-bedroom house for a worker in a shoe manufactory:

This economics called Keynesianism worked--spectacularly at times. The summer I graduated from high school in 1967, I worked on a small construction team that built homes. One home was for a guy who worked in a shoe factory sewing tongues or something. You could tell he worked very hard because he would almost fall asleep when he came over to see how we were doing after his work. But the home had three bedrooms, a modern kitchen and bath, a dining area and large living room, and a garage. Remember this guy the next time you read how folks making shoes in Indonesia live these days. We built him a nice house--it is still there and would probably sell these days for well over $100,000.

What role should the financial system play?

Now, this brings us to the question of: just what do we want our financial system to do? Do we want it to dictate terms and conditions of existence to the rest of the economy, as it did in the case of Interco, with the mistaken belief that "debt was a positive force, imposing discipline on corporate managers and forcing them to keep a tight rein on costs"?

There was near unanimity among U.S. elites that a collapse of Bear Stearns the week-end of March 15-16 would have imperiled the entire economy. But that is the common wisdom, and as with so much common wisdom, it is probably wrong.

What happened to Bear Stearns was that a number of players in the financial derivatives markets came to believe that Bear Stearns was no longer a credible counter-party, i.e., that Bear Stearns did not in fact have enough capital to actually cover all its obligations of the derivatives contracts it held. Now remember, the derivatives markets have become tens of times larger than the real economy. As a MarketWatch article on March 10, 2008 headlined, Derivatives the new 'ticking bomb': Buffett and Gross warn: $516 trillion bubble is a disaster waiting to happen

Now here’s the key thing: there is a mind-boggling amount of derivatives out there, but they are not that widely distributed. Derivatives are very complex contracts, and it takes an enormous amount of computer power and management time to understand them and manage them. In his new book, The Trillion Dollar Meltdown, former Wall Street lawyer and investment banker Charles R. Morris writes that "In 1983, modeling the payout scenarios on Fink’s comparatively simple three-tranche CMO took a mainframe computer a whole weekend." Of course, computing power has increased exponentially while decreasing in price since then, but the point is that buying, selling and managing financial derivatives is not for any institution. Millions of dollars in computers and software must be developed and maintained in order to even begin to hope to handle derivatives.

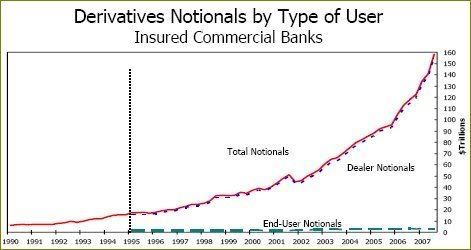

The result is that creating, selling, and trading financial derivatives is entirely the province of a very small number of investment and commercial banks that have hundreds of billions of dollars in assets. In other words, the big Wall Street commercial and investment banks. Take a look at this graph from the Third Quarter 2007 Report on Bank Derivatives Activities by the Office of the Comptroller of the Currency

Look at that bottom line that stays flat no matter how much derivatives increases. That’s the amount held by end-users. End-users ?! So it’s the banks that are holding most of the derivatives. Now, this is just commercial banks, and does not include derivatives activities of investment banks.

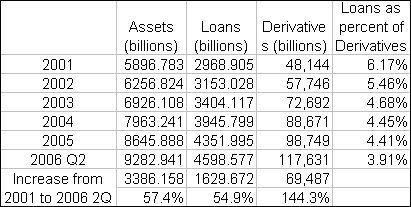

According to the Federal Reserve Board’s Report on the Condition of the U.S. Banking Industry: Second Quarter 2006, derivatives holdings of the 50 largest bank holding companies as of the second quarter of 2006 totaled $ 117,631 billion, or $117.6 trillion.

Derivatives holdings of all other reporting bank holding companies in the United States was $88 billion.

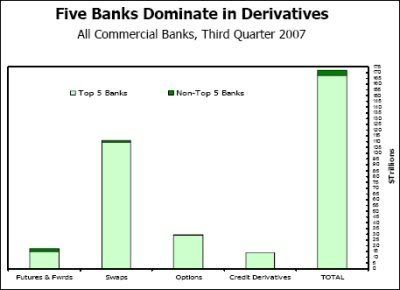

In fact, only five commercial mega-banks - J.P. Morgan Chase, HSBC, Citibank, Bank of America, and Wachovia – account for well over 90 percent of derivatives activities by commercial banks. Here’s a graph from the OCC report:

So, if Bear Stearns had been allowed to collapse, who really would have been hurt?

The big scam of financial derivatives

According to economics professors and business school finance textbooks, the purpose of derivatives is to make it easier to manage the various risks of debt, making credit easier and safer to provide. The effect, according to this common wisdom, is to make credit more readily available. But studies by the Federal Reserve Bank of New York have found otherwise. In other words, derivatives are NOT helping to create more and safe credit for the real economy. Why has this not been a central question our government and our media evaluate the situation in the aftermath of the Bear Stearns bailout? Let’s look at the evidence. These numbers come from the above report, the Federal Reserve Board’s Report on the Condition of the U.S. Banking Industry: Second Quarter, 2006

Note that neither assets nor loans increase anywhere near as much as derivatives. Note that in just five years, the proportion of loans to derivatives shrinks toward half what it was: 3.91 percent at the end of the second quarter of 2006, compared to 6.17 percent at the end of 2001. It seems reasonable to expect that if derivatives are in fact helping the creation of credit, the proportion would remain roughly the same. In fact, as we are seeing now, the huge growth of derivatives has triggered a financial collapse in which the supply of credit is rapidly diminishing.

Here’s part of the summary from Credit Derivatives and Bank Credit Supply, Federal Reserve Bank of New York Staff Report No. 276, February 2007

The results for the volume of lending are more mixed: the volume of large term loans is unaffected by changes in the degree of credit derivatives protection, while the volume of smaller term lending decreases. Overall, the results suggest an increase in the supply of credit to large term borrowers. Since large firms are more likely to be "named credits" in the credit derivatives market, this finding suggests that the benefits of credit derivatives may accrue mainly to these firms, rather than being spread more broadly across the business sector.

In contrast, there is little to suggest that increased use of credit derivatives leads to an increase in loan supply for commitment lending, to either large or small borrowers. The volume of new commitment lending falls as net credit protection increases, and loans spreads are basically unchanged. The average maturity of loans to small commitment borrowers also falls as credit derivatives protection increases.

In fact, the New York Fed study is forced to admit that

In contrast, Morrison (2005) and Duffee and Zhou (2001) suggest that credit derivatives may undercut other forms of risk transfer such as the loan sales market, and ultimately reduce the overall supply of credit (bank loans and bonds).

So, if the hundreds of trillions of dollars in derivatives are NOT helping get more credit into the hands of entrepreneurs and small businesses (and remember the Bush administration / conservative tax cutting mantra that small businesses are the engine of innovation and employment in our economy), then why are the big Wall Street banks creating such an overwhelming amount of derivatives?

I suggest that it is almost entirely to generate fees, and to trade for the banks’ own accounts. But, I confess, I really do not know. If someone in Congress would think to ask the questions I’m raising, we might get some answers. While we’re waiting, I would like to direct you to the point Warren Buffett makes in his 2006 letter to Berkshire Hathaway shareholders, where he relates the little parable about the Gotrocks. Buffet argues that the financial system continues to grow and grow, "earning for itself more and more fees and profits, which are actually being squeezed out of the real economy.

The London Telegraph revealed on March 23, 2008 that New York Federal Reserve Bank president Timothy Geithner has long been warning

about the dangers of concentration in the $45 trillion market for credit default swaps (CDS), in which that 10 banks make up 89 per cent of the contracts. Pay particular attention to the language used in the Telegraph article to describe the function of credit default swaps:

These CDS swaps are a way of betting on the credit quality of companies without having to buy the underlying bonds, which are less liquid. . . . In the old days it was hard for speculators to take "short" bets on bonds. Credit derivatives open up a whole new game.

"It is now much easier to short credit, " said James Batterman, a derivatives expert at Fitch Ratings in New York. "CDS swaps can be used for speculation, and that can cause skittish markets to overshoot," he said.

Is this reallywhat we want our financial system to be doing – making it easier to place "bets"?

Policy implications

If financial derivatives are actually only a way for the small, select club of big Wall Street investment and commercial banks to generate fees, and if derivatives activities are so highly concentrated, there are some very radical implications for policies to deal with the unraveling of the "shadow banking system."

Specifically, come the next "too big to fail" crises, it would actually be better to let the institution involved fail. And let them take the rest of the big Wall Street players with it. As far as the real economy would be concerned, good bye and good riddance. With derivatives acticities so higky concentrated, we can let the big Wall Street players collapse into the ruin they so richly deserve (pun intended) while insulating the rest of the financial system and the real economy from their collapse. Using the precedent of what Franklin Roosevelt did to stop the bank runs in 1932, the President need simply declare a bank holiday, but only for derivatives contracts. That prevents all the "counterparties" from being dragged down with the next Bear Stearns.

Besides, derivatives aren’t supplying credit to the real economy anyway. The important thing is to overcome the psychology of fear and panic that threatens to infect real bank lending to the real economy. The danger of the psychology of fear and panic spreading was the essence of the argument for "saving" Bear Stearns (which in effect was really a bailout of J P Morgan Chase, Lehman, and other big Wall Street commercial and investment banks).

We want to force a shift of the financial system away from the big-money operations of Wall Street, back to relatively small lending operations to Main Street. So we let the top dozen or so institutions go under. To save that part of the banking system that actually helps Main Street, the Fed should make a very public show of back-stopping the smaller commercial banks all around the country - just like it did for JP Morgan Chase in the Bear Stearns "bail-out."

The one nagging problem is what to do about all the shareholders of the big Wall Street commercial and investment banks? Whoever the next President is can send emissaries to the various pension funds and mutual funds to tell them in no uncertain terms of the intent to let the big Wall Street players meet their well-deserved doom, taking their shareholder with them. If someone wants to bet in a game of chicken that the next President would not actually let the big Wall Street players go under and remain a shareholder, well, they were warned. Yes, this is "talking down" the big Wall Street banks, but it would only be them getting a taste of the medicine they themselves have been cramming down the throats of the rest of the economy (such as having conniptions over Costco paying its employees much more than the retail industry average).

What remains of the big Wall Street players can be sliced and diced, and parceled out to all the thousands of remaining small banks. For example, a Chase branch or Citi branch in Peoria should be offered to 1st National Bank of Peoria for a song.

The goal is to excise the big Wall Street commercial and investment banks from the financial system, just like a tumor is cut out of the body. Yes, I will make the idea explicit here: the goal in the next crisis point of the financial collapse should be to ruthlessly euthanize the biggest institutions on Wall Street. These big commercial and investment banks are NOT providing any net value to the economy – they are actually sucking value out. A few years ago, John Bogle, founder and retired CEO of The Vanguard Group of mutual funds, estimated that the financial system is actually subtracting $540 billion in value from the economy (See Bogle’s discussion on Bill Moyers Journal.)

Consider the conclusions of a February 2005 report, by the Federal Deposit Insurance Corporation Consolidation in the U.S. Banking Industry: Is the Long, Strange Trip About to End?, on the effects of the emergence of the mega-banks like J.P. Morgan Chase, HSBC, Citibank, Bank of America, and Wachovia.

In addition to lacking consensus on cost efficiency gains, empirical work to date has also failed to find substantive evidence of other benefits that one might hope consolidation would yield. For example, there is little evidence that either consumers or shareholders have benefited from consolidation in the industry. In fact, there is growing evidence that increases in market power at the local level may be adversely affecting consumer prices (for both depositors and borrowers). And as we mention above, there is also some evidence that managers might be pursuing mergers and acquisitions for reasons other than maximizing firm value (researchers who have studied the issue have consistently found support for the idea that empire building and increased managerial compensation are often a primary motive behind bank mergers). Finally, findings from several researchers suggest that industry consolidation and the emergence of large complex banking organizations have probably increased systemic risk in the banking system and exacerbated the too-big-to-fail problem in banking.

Did you catch that? empire building and increased managerial compensation are often a primary motive behind bank mergers. Forbes reported last week that the five principals of Goldman Sachs were paid over $300 million. This is really what the game has been about for the past thirty years.

If society is receiving no benefits from a financial system which has been restructured under deregulation to favor speculation rather than real investment, and which has led to domination by less than a dozen big institutions that are increasingly unwilling to lend to the smaller actors in our economy, why do we continue to tolerate the laissez-faire policies that have led to this situation?

In his post on European Tribune I referenced above, Techno related how he first became aware of the danger of the laissez-faire policies Techno related how he first became aware of the danger of the laissez-faire policies promoted by the financiers and speculators, in a class with John Kennedy’s chief economic adviser, Walter Heller:

Being reasonable is not easy. Folks with a simple one-size-fits-all philosophy substitute tenacity for reason and thoroughly mistrust anyone who begins an answer to a question with "that depends on a host of circumstances." But that was exactly what the Keynesians were trying to do--answer questions with "that depends." It was an attempt to match the subject of political economy with the complexity of industrialization. As a result, the economic fundamentalists mistrusted the complexity embraced by the Keynesians. And even after more than 40 years of Keynesian influence, the laissez faire fundamentalists had not disappeared from the economic debate--and certainly not at the academic level.

Facing packed lecture halls, Heller invited debate and controversy as a teaching style. One day, a crew-cut young prairie banker's son baited Heller with the idea that regulation of the financial business was an example of "creeping Socialism." Heller stood very still. He was visibly annoyed as if he were a world-class astrophysicist confronting a member of the flat-earth society. Since this was over 34 years ago, my quote may not be exact but as I remember it Heller said, "Young man, what I am teaching is not creeping, walking, or any other ambulatory form of Socialism. We saved Capitalism from itself. There are regulations because Capitalism without regulations does not work."

Heller's annoyance at the partisan of deregulated Capitalism that day was probably due to his frustration that even though he and his kind had found the political center, fundamentalism in economics had not been slain.

Now, Wall Street, the conservatives, and those who now think of themselves as progressives but who have made their living in finance and banking are going to howl that taking back sovereign control of credit allocation and directing credit flows into national priorities is government intrusion in the market, and even, gasp, socialism. Which is a total lie. The "free market" argument is merely the ideological justification for their mis-use of the economy's credit mechanism.

So, we need repeat, one very simple idea: It's WALL STREET versus AMERICA.

Impose a tax on speculation

Once we have eliminated the big Wall Street institutions that have been essentially looting the economy, and redirected the financial system back to providing capital for capitalism, we need to ensure that speculation does not again become a problem. The best and easiest way to do this is simply to tax speculation. In Why Financial Crises Will Keep Happening Ian Welsh explained how returning the top income (incomes over $5 million) tax rate to the 75% or even 91% of the 1940s to 1970s will eliminate much of the financial manipulation that ultimately saps the strength and vigor of the real economy. Executives must be placed in a situation where they can only make a fortune if they are able to manage a corporation over the long-haul of ten or twenty years. Making a quick fortune in just a few years

At this point to wring the excesses out of the system and to stop the systemic incentives to keep blowing bubbles is going to require making it so that reaping a fast fortune at the expense everyone else doesn't pay. There are two parts to any solution:

- The first and simplest way is to put a very progressive tax on all income no matter how or where earned that probably comes in at over 95% of all income over, say, $500,000 or a million at the most. Suddenly, needing to actually keep the companies sound, and knowing that in 7 years when the loans go bad, they'll still be there taking the heat for it, will tend to concentrate the mind not on "can I make enough money to be in a yacht in 3 years" but into "does this deal make sense over the long run".

- The second thing to do is to stop allowing people to sell risk.

For years Greenspan argued that risk markets (the ability to take on, say, default risk in credit or for that matter to sell loans in CDOs) made the system stronger and actually reduced systemic risk by spreading risk around. What it did instead is take the risk away from the people who were able to manage it because they were close enough to the ground to know whether a loan was risky and give it to people who really had no clue and had to rely on bond rating agencies to tell them if the risk was acceptable. Without a loan officer in the actual district, without actual inspections of houses and businesses and without the loan officers knowing that 10 years from now if the loan goes bad some manager is going to call them into the room and ask them to justify the decisions they made, the people taking on the loans had no ability to know if they could, or would, be repaid. And the banks, since they thought they were selling the risk, mostly didn't bother with old style vetting and indeed banks like Citigroup have gutted the departments which used to do that sort of work.

In The Economic Case for the Tobin Tax, Thomas Palley explains how a Tobin Tax helps dampen speculative volatility in the foreign exchange markets, and directly references the idea of Pigouvian taxes, which Wikipedia defines as a tax levied to correct the negative externalities of a market activity. A Google search for "Tobin tax" will provide a wealth of good material to read, or you can simply go to the website of the Tobin Tax Initiative. The thing to note here is that a Tobin tax must be placed not just on foreign exchange, but on all financial transactions: bonds, stocks, futures, options, and derivatives. A tax of one percent or less (Tobin originally suggested one fifth of one percent)

As the New Rules Project explains:

In 1970 more than 95 percent of currency trades were for activities linked to what many call the "real economy" -- investment, tourism, foreign aid, trade. Today only two percent are. The volume of currency trading is now some 50 times greater than the volume of trade in goods and services. We trade more than $100 worth of stock and bonds for every dollar raised for investment in new plant and equipment, a ratio almost four times greater than 30 years ago.

This delinking of money from place and productive investment is not the inevitable result of technological advances or economic evolution. Money is a human invention and rules that control its dynamic are also a human invention. To slow down the speculative and destabilizing flow of money, John Maynard Keynes proposed a small financial transactions tax in 1930. In the 1970s, Nobel Prize winning economist James Tobin proposed a tax on international financial transactions. The modest tax could dampen volatility and encourage longer term investment. Today traders hold assets for a few hours, or even a few minutes. They are happy with a very small return on each trade.

Before the next Bear Stearns hits, we need to answer the question: What do we want the financial system to do? When we are facing global crises of food and water shortages, and global climate change, I suggest that we can no longer afford to allow the financial elites to use the economy’s credit mechanism for their own private gain. We must begin to think, plan, and build long-term. It makes no sense to face the future hobbled with a financial system that is oriented to short-term speculation and self-aggrandizement. We need to redirect credit away from speculation and into the building of a new, green economy.

Many will object that my ideas might destroy credit or even the whole economy. My answer is: You mean, more than the present crises already have?

A Tougher Market for Student Loans

U.S. lenders freeze home equity credit lines

Paper cuts could bleed equipment-financing biz

Commercial property deals disappear as CMBS funding goes dry

Mountain of cash piling up, as investors wait for a sign

SEVERE Poverty Rate UP 26 percent since 2000