Last November I wrote a diary called The Panic of 2008? in which I predicted:

This is NOT the Great Depression II. Nor is this the stagflationary 1970s. It is going to unfold as some other Beast. Only the broad outlines of this Beast appear discernable now: it will likely feature (1) increasing import prices; (2) wage stagnation (that does not keep up with price inflation); (3) real asset deflation; and (4) possibly a Japan-style "liquidity trap."

That prediction has been borne out so far. In view of the events of this last week, particularly the run on Fannie and Freddie, and the failure of IndyMac, revisiting the Big economic Picture seems timely. The Panic of 2008 is unfolding like a neutron bomb over the financial and construction sectors of the economy, leaving the infrastructure of the rest of the economy basically intact. Asset prices - stocks and real estate - are declining, wages are stagnant, import inflation is setting records. But The Panic of 2008 nevertheless signifies an important turning point.

Cross-posted at The Economic Populist

I. Introduction

The genesis of the Panic of 2008 was the tremendous housing-centered credit bubble earlier in the decade. Fog-the-mirror credit was extended to those who had no hope of ever paying it back, by mortgage brokers whose sole financial interest was "closing the deal." The loans were immediately bundeled together and sold off to "investors" who thought they were buying "AAA" rated debt, which turned out to be cr*p. The availability of all of those mortgages also led to a massive overbuilding of residential housing, at inflated prices due to artificially stimulated demand. So now, just as the bad credits are blowing up, the underlying assets are in decline, triggering the next series of defaults -- much as each not-quite-watertight compartment in the sinking Titanic's filling up with water, tipped the ship just enough for water to spill into the next compartment.

II. The 3 modes of financial crises

To recap, it is worthwhile to return to this excellent summary of 3 types of financial crises by Prof. Brad DeLong. First, he identifies 3 classes of financial crises:

- Liquidity crises

- Solvency crises that are easily cured by easier monetary policy that boosts asset values

- Solvency crises that aren't easily cured by easier monetary policy

that he then describes in fuller detail:

A full-scale financial crisis is triggered by a sharp fall in the prices of a large set of assets that banks and other financial institutions own, or that make up their borrowers' financial reserves. The cure depends on which of three modes define the fall in asset prices.

The first -- and "easiest" -- mode is when investors refuse to buy at normal prices not because they know that economic fundamentals are suspect, but because they fear that others will panic, forcing everybody to sell at fire-sale prices. [My note: in this mode, unlike modes 2 and 3, underlying assets are worth more than accumulated debts, but they are not "liquid" -- they cannot be sold at other than discount prices prior to the date at which payments on debt become due].

The cure for this mode -- a liquidity crisis caused by declining confidence in the financial system -- is to ensure that banks and other financial institutions with cash liabilities can raise what they need by borrowing from others or from central banks.

....

In the second mode, asset prices fall because investors recognize that they should never have been as high as they were, or that future productivity growth is likely to be lower and interest rates higher. Either way, current asset prices are no longer warranted.

This kind of crisis ... [is] because the problem is that banks aren't solvent at prevailing interest rates. Banks are highly leveraged institutions with relatively small capital bases, so even a relatively small decline in the prices of assets that they or their borrowers hold can leave them unable to pay off depositors, no matter how long the liquidation process.

....

The problem is not illiquidity but insolvency at prevailing interest rates. But if the central bank reduces interest rates and credibly commits to keeping them low in the future, asset prices will rise. Thus, low interest rates make the problem go away....

....

The third mode is like the second: A bursting bubble or bad news about future productivity or interest rates drives the fall in asset prices. But the fall is larger. Easing monetary policy won't solve this kind of crisis, because even moderately lower interest rates cannot boost asset prices enough to restore the financial system to solvency. [My note: This mode is the full-fledged deflationary spiral and liquidity trap].

Applying DeLong's 3 modes to recent events, we see that what began as a "subprime" mortgage default event in February 2007 turned into a "liquidity" event in August 2007 as two Bear Sterns sponsored hedge funds collapsed. The Federal Reserve, dealing with a "mode 2" event, quickly lowered rates from over 5% to 2%. This allows banks to rebuild balance sheets and restore solvency and liquidity.

What happened this past week is the first indication that we may have begun to pass into a "mode 3" insolvency crisis, where even low interest rates cannot save fragille or overleveraged financial institutions like IndyMac -- and maybe even mortgage giants Fannie and Freddie.

III. The Neutron Bomb over the Financial Sector

A noteworthy graph from Yahoo finance demonstrates that a "neutron bomb" scenario -- in which the financial sector at ground zero is destroyed, but the infrastructure of the "real" economy is left basically intact -- indeed may be unfolding. The graph below covers the last 3 years for the S & P 500 (red) and compares it with the financial sector as represented by the Financial SPDR (blue), starting from a baseline (0%) of 5 years ago:

Note that both moved in close correspondence with one another until the "subprime" crisis hit in February 2007, and diverged more in July and August of last year as hedge funds started to implode and the entire "containment" idea was replaced with "contagion." And yet, although the financial sector has declined from +50% over July 2003 to -20% now, the S & P 500 as a whole (which includes the finance sector) has only declined to +28%.

As the financial sector now constitutes 16.19% of the overall weight of the entire S & P 500, a simple calculation leads to the conclusion that the rest of the S & P, in other words, everything except the financial sector, is still up ~37.5% from 5 years ago, or put another way, has declined less than 10% from its highs in 2007.

A silver lining: several recent snapshots of the real economy support the idea that the financial "neutron bomb" has not seriously damaged the "real," productive economy. For example, last week's ISM report concerning manufacturing, showed the sector growing slightly:

(A number over 50 means expansion. A number under 50 means contraction). The manufacturing sector of the economy isn't doing great, but it isn't even in recession territory yet (notice how the values were significantly less in both the moderate recession of 1991 and the dot bomb recession of 2001).

And then there's retail sales:

According to the retail sales data, apparently somebody forgot to tell American consumers that this was supposed to be a "consumer-led recession" because consumers are still spending more than they were last year. They haven't closed their wallets nearly as much as they did in the dot bomb recession of 2001. Despite the serious pain of soaring food and energy prices, so far Americans have only diverted their purchases from other goods. They haven't moved into the defensive crouch of a consumer recession yet -- let alone the 10% year over year decline in consumer spending during the first year of the Great Depression.

So far the data paints a picture of a total meltdown of the financial sector of the economy, with the rest of the economy, while under considerable stress from soaring gasoline prices, hasn't buckled yet. But make no mistake, this is a fragile basis for stabilization or recovery. As I pointed out in a diary one year ago entitled, Are Hard Times Near? The Great Decline in Interest Rates is Ending, for nearly 30 years American consumers have relied on increasing asset prices (stocks or real estate) or decreasing interest rates (to refinance debt) during those times like the last 8 years in which their incomes and wealth have not increased. Only once before (the recession of 1991) have all of these sources been closed off. The evidence is that Americans are increasingly adding purchases (like, of gas for their cars) to their credit card balances, and eating their seed corn by taking loans from their 401K plans. This cannot go on for very long.

IV. Meanwhile, Import prices have soared.

On Friday we also got an update on import prices. They are soaring, and the year-over-year comparisons are getting worse every month. Inflation in import prices, at 20.5% annually, is now worse than even during the 1970s oil shocks:

This is what happens to Banana Republics whose currencies are not worth holding on to. More on the ramifications of this in part VI. below.

V. A turning point this week?

But if so far we have only seen a "neutron bomb", then the events of the last week are warnings that an "atomic bomb" may be ticking, and a much worse "hydrogen bomb" is possible.

Until just a few weeks ago, the idea that the two huge Government Sponsored Entities (GSE's), Fannie and Freddie, might need rescuing, was a fringe idea. Then on Wednesday former Fed governor William Poole said they were "insolvent" triggering a classic panic -- an outright run on their shares. By the end of yesterday there were rumors floated and denied of nationalization and Fed intervention. If either scenario comes to pass, that would be like an "atomic bomb" having wide but not universal ramifications for the economy.

Fannie and Freddie did not write subprime mortgages or liar loans. While only a small fraction of Fannie and Freddie's $5 Trillion combined portfolio's (of conforming 80% or less mortgages) would likely fail, even 5% of that (a reasonable worst case scenario) is $250 billion. That would be an enormous tab for the taxpayer to pick up. Even if the taxpayer does not pick up this tab, but merely "purchases" the entities and becomes their new owners, (and becomes entitled to the income stream generated by the mortgages) that is going to add some serious red ink to the deficits. Taxes are going to have to be raised, budgets severely cut, or a large amount of new debt (bonds) will have to be issued. This is not good news for the world's biggest debtor, Uncle Sam.

In view of Uncle Sam's possible $100 billion+ new liability, something unheard of happened. Usually when the stock market tanks on bad news, investors "flee to quality" which typically means buying US treasury bonds. Yesterday, for the first time in living memory, that didn't happen. While gold, oil, and most other commodities rallied; and while most foreign currencies (e.g., Euro, Yen) rallied (i.e., the dollar lost value; US Treasury bonds not only did not rally, instead, they sold off significantly (orange line Thurs., to green line Fri.):

If the nationalization of Fannie and Freddie would be an "atomic bomb", then the ramifications to the FDIC insurance system of more bank collapses like IndyMac would be like a "hydrogen bomb", setting the stage for unthinkable commodity prices and a rout of US Treasury bonds orders of magnitude worse.

At the end of 2007, according to the FDIC's financial statement, it held $53 billion in its deposit insurance fund. According to the FDIC press release announcing the seizure of IndyMac:

Based on preliminary analysis, the estimated cost of the resolution to the Deposit Insurance Fund is between $4 and $8 billion

While the IndyMac failure does not impair that fund, if there are many more such failures lurking, ultimately the FDIC would have to resort to Uncle Sam's printing press to make good on its insurance. And that would make the selloff in US Treasuries on Friday look like a picnic.

VI. Conclusion: Slouching slowly but inexorably towards a Banana Republic

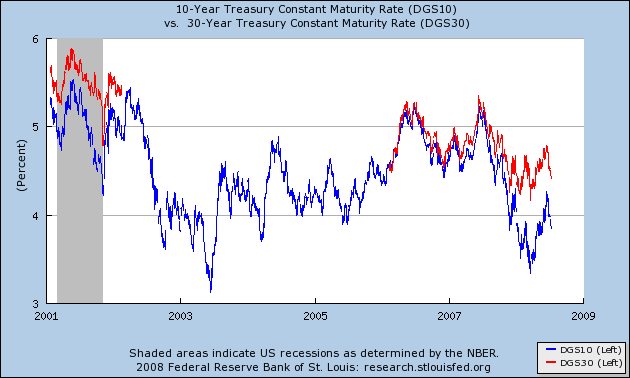

As readers of my comments and diaries know, I dislike Armageddon scenarios. They are extremely, extremely rare for a reason. Even with all of the mismanagement and collapse of the Bush/Greenspan credit bubble -- problems widely observed, reported on, and known to investors for the last several years -- US Treasury bond yields are still firmly in the range they have occupied since January 20, 2001:

But what is happening is that the US dollar has substantially lost its position as the world's reserve currency, as reflected in this graph of foreign holdings:

The US has largely escaped the ramifications of being a deadbeat debtor nation due to the privileged position of having the world's reserve currency. As that wanes, more and more inflation will be imported in response to ever more debt creation, even if necessary in response to a crisis. If long term rates go up 1/4% in view of a possible seizure of Fannie and Freddie, imagine what will happen to them if there is full nationalization, and if there is printing of money to fund FDIC insurance. Even a 1% increase in long term borrowing rates will create serious problems for consumers and for Uncle Sam's continuing to finance his debt.

The Panic of 2008 is the turning point. The average US citizen is seeing a declining standard of living relative to the rest of the world. Interest rates will begin to rise, not in a drastic end-of-the-world move, but gradually, inexorably, and increasingly so long as Uncle Sam and his citizens continue to accumulate debt.