Our banking and financial system is nowhere near out of the woods. Thanks to a now-defunct company named World Savings (whose polluted loan portfolio constituted a poison pill for Wachovia, which recklessly purchased World Savings and in turn went under), the option ARM loan, which World Savings pioneered, now threatens a very serious second wave of real estate defaults.

And courtesy of another company I've written about before, a massive second wave of ARM-related mortgage defaults is heading our way. Combined with a freshly cresting wave of commercial real-estate defaults in every city in the country, this second round of failures will be more prolonged and possibly more damaging than the first one.

We wonder why the banks have not turned around and used the taxpayer-provided bailout funds to grease the wheels of consumer and business credit? I think I have the answer.

I'll also add a rather painful personal take on this subject at the end of this post.

My theory is that the banks are hoarding the bailout money they received from the first tranche of the $750 billion bailout fund precisely because they know this wave of Option-ARM defaults and commercial real-estate failures is coming and that they simply cannot afford further loan investment until that coming wave subsides.

Here is the seismic depth charge awaiting Obama's economic team:

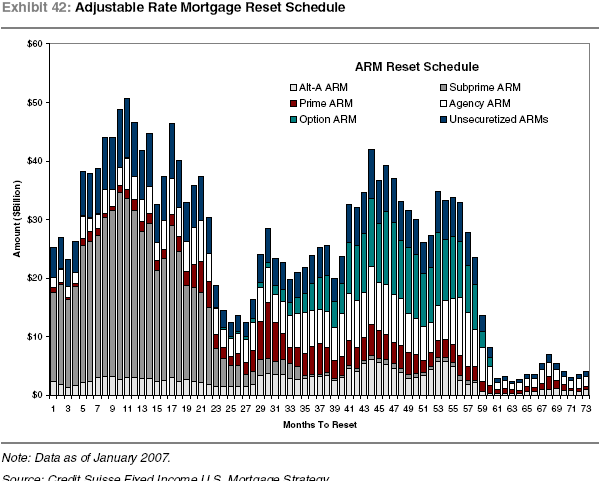

At this point in time, the first big wave of failures, based on subprime mortgages, is largely in the process of being worked out of the system. Move over to Bar 24 in the chart, representing January 2009, and you'll see that the Subprime ARM wave is largely a thing of the past. It's no big deal. We simply contemplate the wreckage of the American financial sector, with the complete destruction of the Wall Street investment banking houses and the quick disappearance of several of America's largest commercial banking institutions, a mere eight to nine years after the bipartisan passage and signing (by Clinton) of Gramm-Leach Bliley in 1999 wiped out what remained of the regulatory framework preventing the deadly combining of investment and commerical banking enterprises.

A mere nine years since Glass-Steagall was completely eliminated, the American banking class managed to destroy their entire business sector, with the active connivance of both parties on Capitol Hill. It took a mere nine years for this generation of American financial business leaders to give the lie to the theory of laissez-faire capitalism.

Unfortunately, what confronts Obama's economic team resembles the last, full, bitter cup of America's financial undoing. By next fall, roughly beginning from Column 33 in the chart above, the Option ARM wave starts to hit. And it lasts a LOOONNNNG time. In fact, another two years pass before the peak is past. In no specific month do the sheer quantities of Option ARMs match those of the worst months of the Subprime ARM meltdowns: perhaps 30-40 billion dollars a month of loans at risk throughout the system.

The big problem is, that Option ARMs are the most toxic type of mortgage loan, the most frankly fraudulent, that were ever conceived in the American banking system. And, because of the lack of separation between commerical banking and investment banking, all of these horrible predatory loans were flipped into securities before defaults started in earnest. The "Option" comes about simply because the loan gives the mortgage holder the option to make a small 'minimum' payment instead of their contracted regular payment amount. Unfortunately, companies such as WaMu and World Savings, which specialized in Option ARMs (World Savings invented them) often neglected to make clear to the borrowers that opting for such "options" quickly leads to an increasing principal on the loan. This in turn leads to increases in the size of the payments themselves and in the real amount owed on the loan. It is, in short, blatant loan sharking.

This is the reason, I propose, that the banks are not using the bailout money to increase the velocity of money through the system by making loans and financing small businesses or large business capital investment. They can't because all of them are facing a huge second wave of failed securities based on the toxic Option ARM loans those very banks originated (or purchased originating banks of) up through 2007. These guys are terrified. They know the game is up. The boards of all those companies are demanding that the corporate officers find any way possible to keep their companies alive through the downturn. At least, without direct evidence, this is what I see as a likely real-world response to the current situation in all financial companies that remain alive to date.

As evidence, please consider these terrible lines from a New York times article focusing on the destructive and openly fraudulent practices at Washington Mutual:

At WaMu, getting the job done meant lending money to nearly anyone who asked for it — the force behind the bank’s meteoric rise and its precipitous collapse this year in the biggest bank failure in American history.

WaMu pressed sales agents to pump out loans while disregarding borrowers’ incomes and assets, according to former employees. The bank set up what insiders described as a system of dubious legality that enabled real estate agents to collect fees of more than $10,000 for bringing in borrowers, sometimes making the agents more beholden to WaMu than they were to their clients.

WaMu gave mortgage brokers handsome commissions for selling the riskiest loans, which carried higher fees, bolstering profits and ultimately the compensation of the bank’s executives. WaMu pressured appraisers to provide inflated property values that made loans appear less risky, enabling Wall Street to bundle them more easily for sale to investors.

I have written about the CEO of WaMu, Kerry K. Killinger, before. I want to make sure everyone knows what this man looks like, because I have a feeling he is going to have a big nasty wolf at his door pretty soon:

This man, KKK, is specifically and fully responsible for the biggest investment fraud operation of all time. The scope of his operation makes Bernie Madoff look like an amateur.

But he could not have done it alone, as Mr. Madoff essentially did. Mr. Killinger's fraud had many accomplices.

As a supervisor at a Washington Mutual mortgage processing center, John D. Parsons was accustomed to seeing baby sitters claiming salaries worthy of college presidents, and schoolteachers with incomes rivaling stockbrokers’. He rarely questioned them. A real estate frenzy was under way and WaMu, as his bank was known, was all about saying yes.

Yet even by WaMu’s relaxed standards, one mortgage four years ago raised eyebrows. The borrower was claiming a six-figure income and an unusual profession: mariachi singer.

Mr. Parsons could not verify the singer’s income, so he had him photographed in front of his home dressed in his mariachi outfit. The photo went into a WaMu file. Approved.

"I’d lie if I said every piece of documentation was properly signed and dated," said Mr. Parsons, speaking through wire-reinforced glass at a California prison near here, where he is serving 16 months for theft after his fourth arrest — all involving drugs.

While Mr. Parsons, whose incarceration is not related to his work for WaMu, oversaw a team screening mortgage applications, he was snorting methamphetamine daily, he said.

"In our world, it was tolerated," said Sherri Zaback, who worked for Mr. Parsons and recalls seeing drug paraphernalia on his desk. "Everybody said, ‘He gets the job done.’ "

At WaMu, getting the job done meant lending money to nearly anyone who asked for it — the force behind the bank’s meteoric rise and its precipitous collapse this year in the biggest bank failure in American history.

Mr. Parsons, who worked for WaMu in San Diego from about 2002 through 2005, said his supervisors constantly praised his performance. "My numbers were through the roof," he said.

And:

WaMu’s retail mortgage office in Downey, Calif., specialized in selling option ARMs to Latino customers who spoke little English and depended on advice from real estate brokers, according to a former sales agent who requested anonymity because he was still in the mortgage business.

According to that agent, WaMu turned real estate agents into a pipeline for loan applications by enabling them to collect "referral fees" for clients who became WaMu borrowers.

Buyers were typically oblivious to agents’ fees, the agent said, and agents rarely explained the loan terms. "Their Realtor was their trusted friend," the agent said. "The Realtors would sell them on a minimum payment, and that was an outright lie."

According to the agent, the strategy was the brainchild of Thomas Ramirez, who oversaw a sales team of about 20 agents at the Downey branch during the first half of this decade, and now works for Wells Fargo.

Mr. Ramirez’s team sold nearly $1 billion worth of loans in 2004, he said. His performance made him a perennial member of WaMu’s President’s Club, which brought big bonuses and recognition at an awards ceremony typically hosted by Mr. Killinger in tropical venues like Hawaii.

Mr. Ramirez’s success prompted WaMu to populate a neighboring building in Downey with loan processors, underwriters and appraisers who worked for him. The fees proved so enticing that real estate agents arrived in Downey from all over Southern California, bearing six and seven loan applications at a time, the former agent said.

And:

Top producers became heroes. Craig Clark, called the "king of the option ARM" by colleagues, closed loans totaling about $1 billion in 2005, according to four of his former coworkers, a tally he amassed in part by challenging anyone who doubted him.

"He was a bulldozer when it came to getting his stuff done," said Lisa Alvarez, who worked in the Irvine office from 2003 to 2006.

Christine Crocker, who managed WaMu’s wholesale underwriting division in Irvine, recalled one mortgage to an elderly couple from a broker on Mr. Clark’s team.

With a fixed income of about $3,200 a month, the couple needed a fixed-rate loan. But their broker earned a commission of three percentage points by arranging an option ARM for them, and did so by listing their income as $7,000 a month. Soon, their payment jumped from roughly $1,000 a month to about $3,000, causing them to fall behind.

Mr. Clark, who now works for JPMorgan, referred calls to a company spokesman, who provided no further details.

A meth addict leaving drug paraphernalia on his desk at work, and being allowed to run riot because, after all, "he made his numbers."

I also must note that not a single word has emanated from the Bush Justice Department about prosecuting people such as Mr. Killinger, Mr. Parsons or Mr. Ramirez and their like in all the other banks in this country. That must change.

One can only hope that once we have an actual President in office, that Obama's Justice Department, hopefully run by Eric Holder, a noted anti-corruption lawyer, will throw the book at all of these people and pack the prisons with them.

Can We Fix This?

In short, probably not. I think one key part of Obama's economic recovery program must be to initiate a government-backed campaign to refinance Option ARM and Subprime ARM holders into more reasonable mortgages. This second massive financial depth charge cannot be allowed to detonate. Complicating matters is that in very few cases can one single loan servicer be dealt with to ameliorate each of these several million toxic loans, because the securitization mess ensures that no single counterparty can be negotiated with. These loans were in all cases originated with the express purpose of bundling them into securities that could then be sold on the open market to beef up the profits of the originating bank and that of the securities brokers themselves.

Of course, the sheer scale of such a project, given the need to more or less contact every Option ARM homeowners (I use the term 'homeowner' very loosely) virtually impossible. One possible approach is to compel the originating banks to relinquish their securitization records - I assume the banks still retain records of all loans they originated and that some kind of flag is in each file indicating that the loan was flipped to another party. This is still a difficult task, but nowhere near as difficult as contacting millions of individual loan holders. That task the originating banks should be forced to do. At least many innocent rank-and-file bank employees will keep their jobs.

Then, place responsibility for servicing the loan back on the bank that originated it. The only way to enforce this en masse may be to order the SEC to unilaterally cancel every Option ARM associated with a toxic security (pretty much all of them). Or pass a blanket omnibus law, doing so, and including a clause in which specific Securitization ID numbers are not required - just proof that the originating bank flipped the Option ARM loan to a third party. Then, in return for being forced to face the consequences of their shitty loan originations, provide the originating bank with the government financing necessary to adjust the loan to a level appropriate for the deflated price of the home on the open market, minus another 10-15% or so to cover some future depreciation while preserving a chunk of the principal. If the bank refuses to play, garnish the amount corresponding to the principal of the original loan from their corporate coffers to cover the cost of a direct Fannie Mae refinancing. Nationalize the originating banks and try their officers in a court of law for securities fraud, and throw them in prison. Even to the banks, 50% of something is better than 100% of nothing. And the prospect of time in Federal prison should concentrate their minds wonderfully.

This is the only way the damage can be limited. I will not speculate on the unpleasant potential consequences of cancelling an entire class of toxic securities; after all, those consequences are already here, as you will see below in the final section of this post. And fuck the hedge funds. They deserve everything that's coming to them.

I can see no other solution. It's time to stop playing games with these people. If the investors and boards of these companies don't like it, well, they should have been paying attention when people like Mr. Killinger were running their rackets.

By way of lip service, many of the people buying homes with these evil loans also were victims, blatantly lied to by people like Parsons, Ramirez and Killinger and told that yes, THEY TOO could buy the overpriced home of their dreams. However, many people eagerly bought the bubble propaganda of instant gratification and thought there was an easy way to home ownership, in a world where home values were guaranteed to rise every year in perpetuity, and where every man could have two sport-utes in their garage and 60-inch flat-screen TVs on the wall, with 24-month interest-free financiang and no cash payments for a year. Opulence on the installment plan. On a gardener's or a mariachi-singer's salary. For some of these people, refinancing their loans just may not be possible, since buying a $600,000 home on a gardener's income with no down payment and no documentation is an exercise in recklessness itself.

I also hate to say it, but to enable rational home-ownership financing again, particularly in grotesquely expensive states like California, some kind of deflationary cycle is inevitable to finally wring the excesses out of the system. Some major changes in the tax code may also be necessary. The home-ownership loan interest tax deduction may need to be revisited. If it is not to take half a lifetime to be able to save a 20% downpayment for a rational mortgage loan, many things are going to have to change, to enable the American Dream of owning one's home to remain a possibility. The bubble mentality must not be allowed to resurface again. It's scary to think that everyone's deflated home values may be in for a further deflation to $60,000-$80,000. But that is a reality we may be facing (and that I AM facing, RIGHT NOW).

I certainly hope I'm wrong. The solution I'm proposing stands a fair chance of preserving what is left of the American financial system, and partially staving off a great American Deflation, which runs a serious risk of occurring over the next couple of years. Unfortunately, based on some of the other diaries I've written, and on my current experience, my predictive abilities are pretty good.

No matter what, legislation also needs to be passed to re-establish Glass-Steagall as the law of the land. No matter what else is or is not done, without this specific re-establishment of regulatory power, nothing will change and Americans will be subjected to further waves of wealth destruction. Uniting investment banks with commercial banks is a recipe for disaster. (And this disaster falls directly in the laps of both parties, to a man. The Gramm-Leach-Bliley Bill of 1999 led directly to this disaster.)

And every dime needs to be garnisheed from Mr. Killinger's personal fortune and from all others like him. People such as the aforementioned loan officers Mr. Ramirez and Mr. Parsons also must be brought to book and punished severely.

In a way, it's good that the Bush Administration has done absolutely nothing to go after these people. Revenge is a dish best eaten cold. I want those people responsible absolutely hunted down and incarcerated for the rest of their lives, from every single investment and commercial bank that participated in this fraud against the American people.

-------------------------------------

On a personal note, I've just discovered that a 3br/1ba home around the corner, more or less, from my house, was sold at foreclosure auction for $130,000. I purchased my house for $360,000 four years ago with a 20% downpayment. This foreclosure house is almost an exact comp to my home, and is not a fixer. While one can pick around the margins of the valuation (my home is in a better part of the hamlet I live in; my house has a second bathroom; and my lot is a bit larger; the fact remains that it is an absolute certainty not only that my downpayment is forfeit, but that I am monumentally upside-down on my mortgage, which is doubtless the biggest financial transaction I will ever make, and one where we were very conservative and got three substantial discounts to the original selling price before we bought.

Essentially, I'm contemplating the utter wreckage of my financial situation. It's quite possible that our house is now worth barely half of what I am paying on my mortgage. I have already sent a request to the County of Sonoma demanding a reduction in my property taxes, but I seriously doubt they will accept the fact that comps in my neighborhood have plummeted so drastically unless I literally take them to court. It is absolutely certain that I will be filing immediately a second time with the county to request a drastic cut in my property taxes.

But, again, that's picking around the margins. I'm still stuck with a comparatively huge mortgage that I seriously doubt the bank will renegotiate. Twelve to fifteen years of appreciation on this house are likely gone.

And I'm the sucker left holding the bag. Even after being as cautious as I knew how to be in a bubble market. While people like Kerry Killinger sit back and count their millions.

In fact, the situation is so bad that sending the keys back to Wells Fargo is a real possibility. Particularly if I lose my job. Seven years of bad credit is nothing compared to paying double what a house is worth, year after year.

At this point, I wish I was still a renter. Even if I don't mail the keys back, it looks like I won't be moving for a LONG time.

Welcome to the Great Deflation. My family and I are victims, and I think I will have a lot of good company as this year goes on.