Here's another Health Insurance is Evil story with some incriminating screen shots. A little over a year ago we came within hours of losing our insurance while my wife was 6 months pregnant.

My wife's former employer, a 121 year old, fourth generation company in Muskegon, was heading into a downward spiral that would eventually lead to its collapse.

Months before the final death twitch, the company got behind on its insurance.

We learned of the health insurance problem only after we had been to a couple pre-natal check ups and had had a routine ultrasound.

A series of letters came in the mail -- "Your insurance has been suspended." So they wouldn't pay the doctors.

To our knowledge the COBRA continuation of our policy was both too expensive, and not available:

What group health plans are subject to COBRA?

The law generally covers health plans maintained by private-sector employers with 20 or more employees, employee organizations, or state or local governments.

Government Site

So we embarked on continuing our policy privately and changing the specific plan to something more manageable.

Side Note: I know there's a lot of folks who would point fingers at the employer here. And maybe he could have been more attentive to this specific issue as his great-grandfather's business and personal situation rapidly swept around him like pyroclastic flow. But I know him from first hand experience to be an honorable person in light of later actions, and count his as a friend. So for now, let's leave that criticism off the table.

We knew our insurance was about to move from Suspended to Dropped.

Here's the problem with Dropped insurance...

...if you're pregnant, and you get Blue Cross Blue Shield of Michigan which, as Michigan's non profit insurer of last resort, cannot turn you away for a pre-existing condition, they STILL will not cover ANY maternity costs if you deliver the baby six months prior to having insurance.

So...if you haven't held the new policy and maternity rider for six months prior to delivering the baby...they won't cover the costs of prenatal care or delivery. At all. (And since she hadn't lost her job, we weren't quite at the point where we could get state assistance.)

Fun Fact: The itemized bill for the prenatal services and delivery? $12,000. For a normal pregnancy.

So we were determined not to let the insurance drop.

I called Blue Cross Blue Shield of Michigan to personally pick up the insurance where our employer left off to prevent a lapse in coverage.

I got routed to an insurance agent who for some reason aggressively pointed me toward a health savings account.

If you're unfamiliar with health savings accounts, they pay NOTHING of ANYTHING until you reach a certain point...like $3000. You pay $320 a month for insurance that does nothing until you've incurred $3000 of health costs. Which is even WORSE if your baby is due in January...because your policy starts OVER. So you pay $3000 out of pocket for prenatal. Then January 1st hits and the clock is re-set, and when the actual delivery and hospital costs come, you pay ANOTHER $3000.

I didn't like this idea.

The agent's case for this specific health savings account policy?

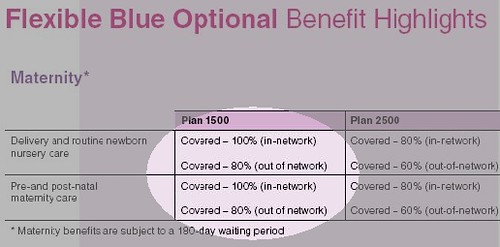

An AMAZING maternity rider. Here's the information he sent me:

See that? Get the health savings account and get the maternity rider which covers ALL maternity stuff. 100%. No deductible.

My wife's prior employer was given a packet with exactly the same information in print. Insurance agents throughout the state had this very same brochure.

100%. No deductible.

Wow.

This sounded good. I needed, NEEDED to get my insurance within 48 hours before getting dropped...

Before I signed on to this insurance I called Blue Cross Blue Shield and asked them to email me a description of the policy.

They said: "Yes sir. It will take us 20 days to print and ship the policy description to you."

TWENTY DAYS?!?! You're going to mail it?

"Yes sir."

That won't do. I need it now.

"No sir. It will take us 20 days to print and ship the policy description to you."

Look. Just EMAIL an electronic version to me. A PDF. I don't need a print version.

"I'm sorry sir. It will take us 20 days to print and..."

FINE...shut up...

Geezus.

Well, I thought, the Agent insisted his information is correct. Blue Cross directed me to him. I have this cross reference brochure of information from my wife's employer. So.......

I signed on. 100% coverage of maternity. AND, he said, it would retroactively apply to costs incurred during the suspension time.

Then the bills started flowing in. And flowing in. And flowing in.

I called Blue Cross.

Hey...what's the deal. I thought you covered this stuff 100%.

"Yes sir. After the deductible"

NO! Nononono...that's not what I purchased.

"Uhh...yes you did."

So I called back several other times to talk to different people. One or two said I was right. Most said I was wrong and needed to pay up. The agent was worthless. Kept saying how people at Blue Cross don't have the training he does.

Finally I got on the phone with a woman who insisted I was wrong.

"No sir...you need to reach your deductible before the maternity costs are covered. I'm looking at the...........hold on....."

She paused for a minute

"....I'm looking at two different versions of the policy brochure."

AHA!

"Yeah. It's strange. One says covered with deductible, one just says covered."

Can I have the one that I signed on for?

"I'm sorry. That's not a legal document. Didn't you get a policy description before signing on?"

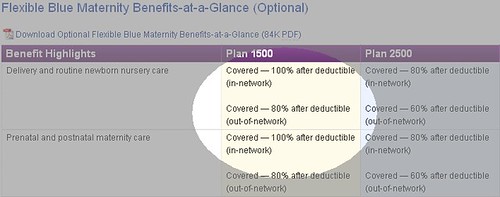

These days if you check the website, it looks like this:

To this day I owe over $6000 on the birth of my son because of this health savings account. Plus the $320 per month for this crap insurance.

And guess which company gets its money first?

The doctors and health care professionals who dutifully rendered the services which brought my son healthily into the world?

Or the company that dangled a bait and switch which claims it will cover me for services, maybe if I need them maybe and maybe, possibly, might save our house if one of us gets sick MAYBE?

Now, a year later, I send the doctors offices $20 a month, and whatever I can. They sometimes call to ask if I can pay more and I say "Sorry. I can't pay for more for the excellent services rendered, because I barely have enough to pay insurance for services that MIGHT be rendered." Some of the offices aren't as lenient. They don't take payments. They send to collections immediately.

It's easy to dismiss the two policy overviews as a matter of a typo...but we're talking about a company whose ONLY PRODUCT is a configuration of ink on paper or pixels on a monitor. If you can't trust the information, you have no product.

Since January I've attempted to find a new insurance company.

Two weeks ago I followed a lead I read about in a comment here on dailykos. Somebody suggested going to the National Association for the Self Employed. The organization claims to offer group insurance to the self employed and private contractors...people who are on their own, in the jungle.

I submitted my information and an agent called me the next day. He visited, gave me a presentation and wanted me to sign on right away. I told him I wanted to investigate the insurance first. Eventually he relented and left me no information about the insurance company, but a business card with no web address.

The insurance was called MEGA.

When I searched it online, after the first link for the company nothing by a laundry list of shady practices, fraud, and exposees from ex-agents citing a company who taught them how to mislead potential buyers.

As it turns out, the National Association for the Self Employed is a front for MEGA insurance. Selling insurance as though recommended through a disinterested third party organization.

Frankly, I don't know who to turn to.

Private enterprise can't be trusted. They can't be trusted to offer an honest, consistent product. And they can't be trusted to articulate what their product actually is because its in their own interest to be as vague and inconsistent as possible. Nobody knows what they offer. Not really. Not the agents, not the call center people, not the managers. Their policies and documents are written to be as amorphous and ethereal as possible...defined on a case by case basis.

Neither private business nor "for profit" "non-profit" organizations can be trusted to do this job.

We NEED the Federal government to take the reigns here and solve the health care crisis once and for all.

As an alarmingly growing number of employers drop health insurance to their employees in this economic recession, and as people lose their jobs and their COBRA benefits run out, the insurance companies are waiting.

They're waiting below with their jaws open wide to catch the growing number of individual plan buyers. The insurance companies know we've suddenly found ourselves in the woods and there are few disinterested third party groups that can council people on the best insurance for that individual. Most agents work for a specific company, displaced as self employed individuals to further remove the insurance company's fingerprints from fraud and deception.

There's only one entity that can help us with this. The Federal government needs to step in.

Policy Description I was given

Policy description Blue Cross will honor