On this Easter/Passover weekend while we are enjoying the blossoming of spring, Robert Reich has a blog post that nicely encapsulates a debate percolating through the econoblogosphere:

[W]e're not at the beginning of the end. I'm not even sure we're at the end of the beginning. All of these pieces of upbeat news are connected by one fact: the flood of money the Fed has been releasing into the economy.... The real question is whether this means an economic turnaround. The answer is it doesn't.

....

I admire cockeyed optimism, and I understand why Wall Street and its spokespeople want to see a return of the bull market. Hell, everyone with a stock portfolio wants to see it grow again. But wishing for something is different from getting it.

In other words, those seeing "green shoots" side and those seeing the "dead of winter" side are polar opposites. To the contrary, I believe there's good reason to believe that both sides are right.

In his post, Reich argues that:

The only economic fundamental that's changed ... is that so many people got so badly burned that the trust necessary for consumers, investors, and businesses to repeat what they did then has vanished.

....

I spent the better part of an hour yesterday evening debating Larry Kudlow on his CNBC program, along with Arthur Laffer and two other financial analysts, all of whom were sure that the stock market had hit bottom and was now poised for a major recovery.

Needless to say, Reich disagrees.

In my opinion, those seeing "green shoots" and those seeing the "dead of winter" are talking past one another. Kudlow et al. are arguing that this economic downturn may be bottoming. There are ample signs such as housing starts probably nearing a bottom and consumer spending rising from the grave that it could be so, though nothing is certain of course (and unemployment will almost certainly rise past 10% and remain there for a far too long period of time even if overall economic activity improves). Reich is arguing that the long-term fundamental imbalances in the economy -- too much financial debt, a lopsided distribution of income -- haven't been addressed, and until they are, the longer term view is bleak. There is ample reason to believe that Reich is also correct.

Many long-term forecasters thought, as far back as the 2001 recession, that a secular bear market was upon us. Eight years later, they are still correct. Most of those forecasters believe, as do I, that the secular bear market is nowhere near over. I hasten to add that in secular terms, a market reflects an economy pretty well, as opposed to short term fluctuations.

But just as the 2001 recession ended, giving rise to the tepid, debt-soaked, fatally flawed Bush expansion, so the 2007-2009 "Great Recession" can end, and some economic expansion take place before the underlying unaddressed fundamentals reassert themselves in a third leg down. That's what I've suggested previously by extrapolating from this graph:

that a long-term, inflation adjusted bottom in the financial markets has not yet been reached, and may still be 5-10 years away.

We are in Kondratieff winter, during which badly leveraged debt all gets undwound, and winter doesn't end until the deleverageing does.

At the same time, March's ~ DJIA 6500 may well have marked a short- to medium-term bottom, something I noticed at the time via this graph of insider purchases vs. sales (during the recession, the market has faltered when such trading was well above the blue line, and at a bottom when it was well below the blue line):

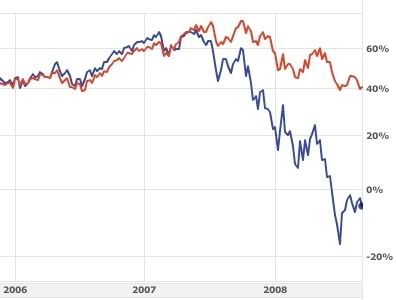

and as suggested by comparing the performance of financial stocks (in blue) vs. the S&P 500 )in red) (financials tend to lead the S&P, which in turn is a leading indicator for the economy) earlier in the recession:

vs. this year:

In other words: we may be getting near a bottom for economic activity during this recession, but any recovery will be brief and fragile, as the unaddressed imbalances of financial "innovation" and a maldistribution of income reassert themselves.

Think of it as the arrival of Springtime. But Springtime during an Ice Age.