On Friday evening, former financial regulator William Black appeared on the Bill Moyers’ Journal and levelly charged President Obama and his administration with deliberately violating the law, enacted in response to the 1980s savings and loans crisis, that requires the U.S. government to place any undercapitalized bank into receivership.

Hundreds of Kossacks were understandably greatly disturbed and distressed to see such serious charges leveled against our new President. One in particular, who has chosen the DailyKos handle of "Geekesque," responded with a diary in which he or she argued that Black and Moyers were not just wrong, but lying, without offering any explanation as to what motive they might have to lie about so serious a matter.

Geekesque’s argument boils down to whether or not the Prompt Corrective Action Law cited by Black applies to bank holding companies. Hilarously, after accusing me of acting like a freeper and not engaging in critical thought, Geekesque is forced by the logic of his or her argument, to the outlandish claim, in the last sentence of the first full paragraph of an update to his or her diary, that no one can touch a bank holding company.

WTF? What is so sacrosanct about bank holding companies? We the people, through our government, grant life to these bank holding companies by granting them a corporate charter. Implicit in the granting of a corporate charter is the expectation that the corporation thus brought into existence will in some way serve the public purpose while seeking to make a profit. What are we to make of the assertion that certain companies are beyond the reach of government sanction? Such thinking is the very worst manifestation of the corporatism that has misshapen our economy, destroyed our financial system, and usurped our political system.

It turns out, Geekesque is wrong about the supposed cloak thrown over bank holding companies by the Bank Holding Act of 1956. Apparently, not many people took Geekesque’s advice to "be smarter than the freepers" by clicking through to the links found on the page Geekesque linked to, and actually reading some of the sections of said Act.

But I want to return to Section 1831 of the Prompt Corrective Action Law, the very last phrase of which states that the "or" of action alternative to receivership is permissible

"after documenting why the action would better achieve that purpose."

OK, show us the documentation. Point out where Paulson or Bernanke or Geithner, or any official in this or the former administration has explained in some document why Citicorp or Citibank or whatever has not been put into receivership. Maybe the first time these zombie banks appeared at the government's doorstep seeking a handout, Geekesque's "or" clause was plausible. But the second time? And the third time?

But it is not enough to simply point out these errors committed by Geekesque, who is simply doing what corporatists often do – try to elude the truth in the spectacularly confusing palace of mirrors that the modern legal system has sadly become, where "justice" is merely a slogan, and the real game is who can best twist and reinterpret previous legal decisions to maintain the power and influence of the corporatists.

Which brings us to the really important issue: What is it that we want the financial system to do?

My view is that we want the financial system to aggregate savings in the economy, then disburse those savings to those people and businesses who need them and will use them for real economic activity.

In my view, therefore, the financial system exists to serve the needs of the real economy. The financial system should be subservient to the real economy. The disproportionate share of profits and income that has gone to the financial system these past three decades, however, strongly suggests that the financial system is no longer serving the needs of the real economy, but has metastasized like a cancer and is engorging itself by eating away at its host.

But why can’t the financial system be elevated to the same level of importance as the real economy? What’s wrong with the financial system "creating wealth" through inventing and trading financial instruments with no connection to real economic activity? To answer these questions, we need to understand what it is the real economy does.

Jared Diamond is rightly famous for his book Collapse: How Societies Choose to Fail or Succeed, in which Diamond examines how societies descend inexorably into collapse when they ignore environmental limitations and mismanage their natural resources. The key point that most readers of Diamond miss is that a society’s environmental limitations are defined only within a fairly specific period of time based on the prevailing technological mode of that society’s economy. Any society that remains stuck in one technological mode will eventually bump up against environmental limitations: what is considered a resource and how much of it is readily available and usable. Because all an economy really is, is how a society organizes itself to procure and process raw materials (natural resources) to create and distribute what is needed to sustain and reproduce human life. So the most important economic activity a society engages in the pursuit of new scientific and technological knowledge that allows that society's economy to avoid environmental limitations and inefficient misuse of natural resources.

For the past century and a half, we have developed an economy based on the technological mode defined by the internal combustion engine and its use of refined petroleum as a fuel. It has been increasingly clear since the late 1970s that our society must break out of this technological mode, both because the amount of petroleum is finite, and because the deleterious effects of burning so much petroleum are so terrible.

It is against this pressing need that we must judge the performance of a financial system: the most important thing we as a society should be doing right now is the research and development of alternatives to the fossil fuel based economy. Has the development of alternative energy technologies been adequately funded since the late 1970s? Imagine what would have been accomplished these past three decades if a like amount to the trillions of dollars that have gone to prop up the zombie banks in the past seven months, had been devoted to the research and development of alternatives to the fossil fuel based economy since Jimmy Carter installed solar panels on the roof of the White House.

This is why Simon Johnson has warned on March 9, 2009 that

Derivatives have the potential to create a rent-seeking structure that is unparalleled in human history. No society can afford to allow that kind of financial system to operate.

Anyone who spends a little time actually looking at reports by the various bank regulatory agencies will see immediately that the problems are located almost entirely in the largest financial institutions in the country. For example: Table VI-A Derivatives, All FDIC-Insured Commercial Banks and State-Chartered Savings Banks

Note that there are 1,097 banks that report holding $201.096 trillion in derivatives. Of these, only 81 banks have assets over $10 billion, and these hold $200.998 trillion - or 99.95 percent of all derivatives. This is where the problems are.

And of these 81 mega-banks, it's actually only a handful that account for over 90 percent of the derivatives holdings, according to the Office of the Comptroller of the Currency.

It's also interesting to see how concentrated the credit derivatives are (this would include the credit default swaps, which are the instruments that turned the sub-prime mortgage collapse into a collapse of the world financial system). Go down to the lines entitled "Credit derivatives as guarantor" and "Credit derivatives as beneficiary."

Now, go down to the line "Credit losses on derivatives". All 1,097 banks report $1.072 billion in losses on derivatives. Of that, $1.071 billion in losses is reported by the 81 mega-banks. Again, almost all these losses are concentrated in a handful of the largest banks: Citibank, and Bank of America being the two banks generally know to be the walking dead.

Finally, you will note that these numbers do not seem to account for all the numbers (in trillions) that are floating out there. I'm not sure why, but I suspect that these numbers do not yet include the statistics from the former investment banks which became commercial banks in order to qualify for direct Federal Reserve life support back in September 2008. These are the more ambulatory institutions that are merely laying on the ground bleeding, but which, in my opinion, need to be killed off for reasons of ending their overwhelming political power, and addressing the problems of anti-trust and "too big to fail." These would be Goldman Sachs, Morgan Stanley, and JP Morgan Chase.

Is it really the case that allowing all 81 mega-banks is going to also destroy the remaining 1,016 banks? I think it will only destroy the cozy little casino mega-banks created and own - and in which the house always wins in the long run.

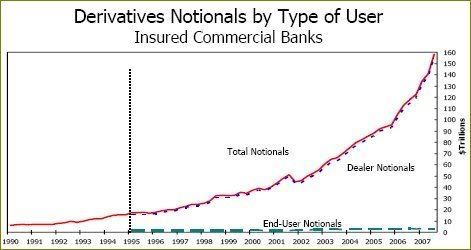

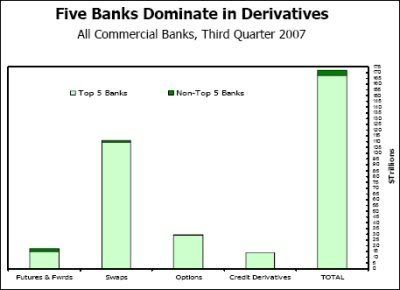

And it's not even the 81 largest banks. It's actually less than a dozen. Here’s a graph from the Third Quarter 2007 Report on Bank Derivatives Activities by the Office of the Comptroller of the Currency

Look at that bottom line that stays flat no matter how much derivatives increases. That’s the amount held by end-users – it’s the banks that are holding most of the derivatives.

According to the Federal Reserve Board’s Report on the Condition of the U.S. Banking Industry: Second Quarter, 2006, derivatives holdings of the 50 largest bank holding companies as of the second quarter of 2006 totaled $ 117,631 billion, or $117.6 trillion.

Derivatives holdings of all other reporting bank holding companies in the United States was $88 billion. In fact, only five commercial mega-banks - J.P. Morgan Chase, HSBC, Citibank, Bank of America, and Wachovia – accounted for well over 90 percent of derivatives activities by commercial banks. Here’s a graph from the OCC report:

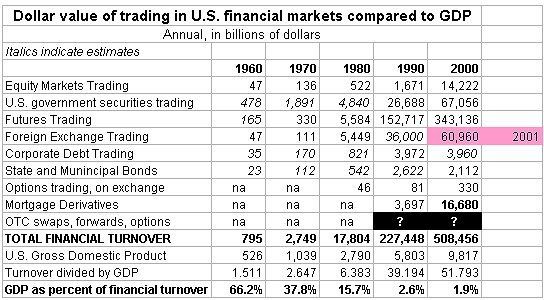

Here’s another way to look at the problem the financial system has become. In the 1960s, all the trading of all the stocks, bonds, futures, foreign exchange, and other financial instruments amounted to about one and one half times the U.S. annual gross domestic product. Today, the trading of all the stocks, bonds, futures, foreign exchange, and other financial instruments amounts to over fifty times U.S. GDP, or around three trillion dollars a day in the U.S.

Above from the Wikipedia article on Financialization

How much does it cost our economy to move around this much financial paper each and every day? Let us assume that the fees, commissions, and so on paid to the financial system for all this frenetic activity amount to one percent. (An October 2003 study conducted by John P. Hussman, President of Hussman Investment Trust, found that the costs to the funds he manages actually amounted to approximately 1.87%; scroll down to the bottom.)

So, one percent of three trillion a day is $30 billion in commissions / fees / bonuses, etc., paid to the financial system for all that paper being shoved around. That's the amount that is going to all those people like the guys in the Chicago futures pits standing behind CNBC's Rick Santelli you saw last month.

$30 billion a day is the equivalent of 600,000 (six hundred thousand) jobs paying $50,000 a year.

That is, the cost to the economy of allowing the financial system to operate as it has been, trading $3 trillion a day, is equivalent to 600,000 good, middle class jobs. Each and every day. This is how the financial system sucks the life blood out of the economy. This is why the present financial system must be destroyed.

One of Stirling Newberry’s recent zingers is that

The more conservative thinkers are appalled at the idea that the monetary order that emerged post-collapse of Bretton Woods might be attacked, because living off of dipping a small cup in the Niagra Falls of finance is the only world they have ever known. . .

I'm distressed that this comment applies to so many of us.

But back to the numbers of this torrent of financial trading. You no doubt saw or heard of the most recent job loss statistics. We're losing over 600,000 jobs a month. How about one day a month, we stop ALL financial trading, and use the money saved to keep 600,000 people in their jobs for one year?