One of the great things about blogs is they encourage a healthy debate among people of differing opinions. On Thursday I wrote and article titled The Black Swan Myth. In this article I argued that there was insufficient evidence to argue the economy was currently in a Black Swan situation -- meaning we were in a period when the traditional methods of analysis and explanation were no longed valid and the underlying rules of the economy were in fact fundamentally changing. On Saturday a fellow member of this community posted an article titled The Swan is Still Black and We're Still Screwed. The authored specifically highlighted three areas of my analysis which he disagreed with. Below I will respond to these points and explain why I respectfully disagree with his analysis.

Initial unemployment claims

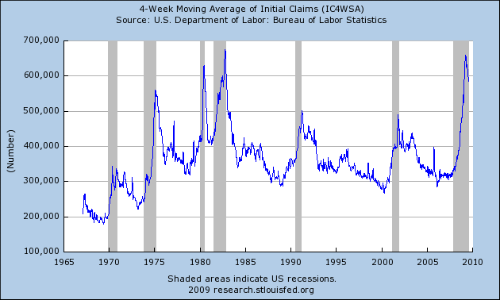

This is a very important number for my analysis because this number has historically topped out right before at just at the end of a recession. The chart below illustrates this relationship:

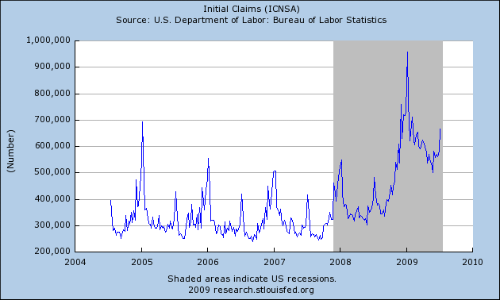

The author of the other article correctly noticed that these numbers are seasonally adjusted. He then argued that using the non-seasonally adjusted numbers provides an explanation which directly contradicts the current downward trajectory of the 4-week moving average of initial unemployment claims. Here is that chart:

The author instead argues that the projected direction of the 4-week initial unemployment claims is in fact upward as represented by this chart:

First, this is a suspicious graph largely because it is theoretical -- there are no marks for amount and time. Is it over a few months or multiple years? However (and more importantly) the author bases this graph on the fact that unadjusted initial unemployment claims are currently increasing. However, his analysis does not take into account the following points.

Historically there is always a spike in initial unemployment claims at in the summer. Here is the information from the St. Louis Federal Reserve:

Notice there is always a summer spike. Hence the reason why there is a need to seasonally adjust the numbers; if we relied on the unadjusted numbers, then every summer we would have a massive recession scare.

Secondly, other information from the labor market indicates initial unemployment claims will continue to move lower.

The Challenger job-cut survey continues to move lower:

And the number of seasonally-adjusted mass lay-off events is now lower than the first part of the year:

In short, there is no reason to think the current direction of initial unemployment claims is a fluke.

CIT Bankruptcy

While there was previously an understandable fear that CIT would go bankrupt, it now appears that will not happen:

CIT Group Inc., the 101-year-old commercial finance company seeking to ward off bankruptcy, agreed to a $3 billion loan for 2.5 years from a group of its bondholders, according to people familiar with the situation.

CIT will pay interest of 10 percentage points more than the three-month London interbank offered rate, said the people, who declined to be identified because the negotiations are private. Libor, a lending benchmark, is 0.51 percentage point. The board agreed to the financing yesterday, and CIT plans to announce the agreement as soon as today, one of the people said.

The funds would give CIT a chance to restructure its debt outside of bankruptcy, said the second person, who also declined to be identified because the talks are confidential. CIT will attempt a cash tender offer for its bonds in August as part of a broader recapitalization, the person said.

CIT needs time to strike deals with bondholders to reduce debt after the U.S. declined to give the firm a second bailout. New York-based CIT, which reported $3 billion of losses in the last eight quarters, received a $2.33 billion rescue from the U.S. Treasury in December after converting to a bank holding company to also be eligible to sell bonds backed by the Federal Deposit Insurance Corp.

While this is not a done deal, it does indicate that market participants are not only interested in dealing with the situation but are now able to deal with it. The reason is the credit markets are in fact much better now than 6-9 months ago:

Demand for the Federal Reserve's emergency short-term lending programs is abating, the latest sign that credit markets are healing.

Borrowing through a program the Fed launched to support the market for commercial paper, short-term corporate IOUs, is at less than one-third its peak level. Securities dealers and investment banks haven't used a Fed borrowing program, launched amid Bear Stearns woes in March 2008, for 10 weeks. Overseas central banks borrowing of dollars from the Fed is running less than a fifth of its $583 billion peak.

Meanwhile, a Fed facility that allows securities firms to trade hard-to-sell collateral for Treasury debt showed just $4 billion in volume recently, down from more than $235 billion in October. And the program through which the Fed auctions to banks is down almost 45% from March.

"The Fed has been able to shift the dominoes in the other direction by very aggressive liquidity policies," said Michael Darda, chief economist at MKM Partners, a trading and research firm. "Now you have these emergency liquidity programs rolling off as these markets improve."

The Fed's overall balance sheet -- the total of all its loans and securities holdings -- stood at $2.06 trillion for the week ended Wednesday, below the $2.3 trillion peak reached last fall, though it grew from $1.98 trillion a week earlier. When Fed officials met in late June, Fed staff said the size of the balance sheet "might peak late this year and decline gradually thereafter," according to minutes released recently.

We've seen a healthy shift from Treasury debt to corporate debt. Interest rate spreads on commercial paper are now back at normal levels:

Simply put, the credit markets are doing much better now.

Commercial Real Estate

First, the author of the other article made this statement:

It's not the CIT situation or commercial real estate alone that can do the real damage, but together the situation is made worse.

In other words, now that CIT is being solved, the author concedes that even if we have problems caused by commercial real estate they may not be enough to caused significant structural damage.

Now -- I will concede the following points: default are increasing and will probably continue to increase. This will put pressure on bank's margins. However, as this chart from the FDIC indicates, banks have been more than able to absorb the losses:

In addition, banks have currently raised nearly $80 billion of equity on the open market indicating there are multiple sources of cash in the event banks have to acquire more capital. In short, the current course of events banks should be able to withstand more stress at this point.

Simply put, there is still little reason to think we are in a black swan situation. Instead, we are in the midst of a severe recession.