I thought I might be able to bring some additional insight into the death spiral discussion in bernardpliers' diary. The phenomenon is happening in the group market as well. This is adapted from my post of August 12, 2009

Ezra Klein interviewed Lindsey Graham back in August 2009 about GOP objections to Democratic health care reform proposals. In the interview, Graham conceded the need for Medicare and Medicaid to cover the elderly and the poor, but that the private insurance market was best suited to cover “the middle.”

But if Graham took the time to honestly examine the health insurance market, he'd see that the "success" of the private health insurers is an illusion built upon consolidation rather than organic growth. The hefty profits of these companies and the generous compensation of its CEO's create a facade of corporate health that masks reality - private insurance is losing a staggering number of customers and will collapse of its own weight without drastic changes.

In market terms, Medicaid exists to cover people who are too poor to buy private health insurance. And Medicare exists, again in market terms, to insure a population that private health insurance deemed uninsurable (i.e. too expensive).

If Medicare and Medicaid established suitable framing for the private insurance market to provide coverage for the “middle” then why does private insurance leave 47 million Americans uninsured? The obvious answer is that coverage is too expensive.

A review of employer-based health insurance by employer size illustrates this point in a couple of ways. As the 2008 HHS Medical Expenditure Panel Survey indicates, the more employees a firm has on payroll the higher the likelihood that it offers health insurance. Put another way, the more revenue a firm has the easier it is to afford to offer health insurance.

But something interesting appears when you look at what percent of these plans are fully insured (pre-packaged health plan bought from an insurance company) or self-insured.

Large employers are significantly more likely to self-insure than smaller employers. The large companies, those with the most revenue, would rather go through the hassle of putting together a provider network, hiring a claims processor, and buying their own reinsurance because… it is cheaper than buying a fully insured plan from an insurance carrier!

PERSONAL ANECDOTE:

A client of mine was spending $25 million a year with a BCBS carrier that had significant market share in its home state. After self-insuring two years ago, my client was able to keep costs level during year 1 (instead of the 10% increase that BCBS wanted for that year). But that also gave us a year of data to review. And we found that they were spending $4 million a year in emergency room visits. Out of that $4 million, over 80% was for non-emergent care. This led the client to invest in an on-site clinic in year 2 that saved $4 in ER costs for every $1 spent on the clinic. My client was able to provide better care at lower costs because it had access to its own claims data in a way that the BCBS carrier would never share with them because the carrier actually risked losing premium by doing so.

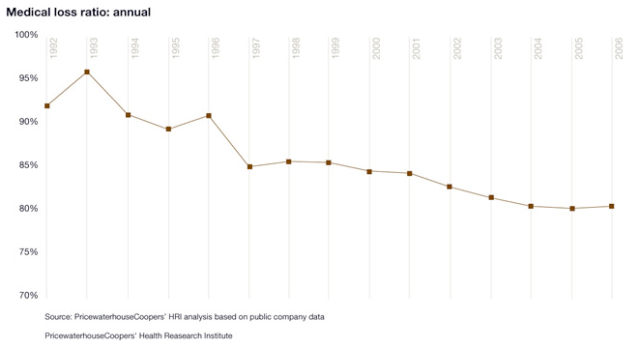

And the increasing margins of private insurance carriers has made self-insuring even more attractive. Medical loss ratios - the percent of insurance premiums that go toward paying medical claims - have fallen from 95% in 1993 to roughly 80% today. Here is the damning slide from the PricewaterhouseCoopers survey that ex-CIGNA executive Wendell Potter quoted from in his testimony to Congress:

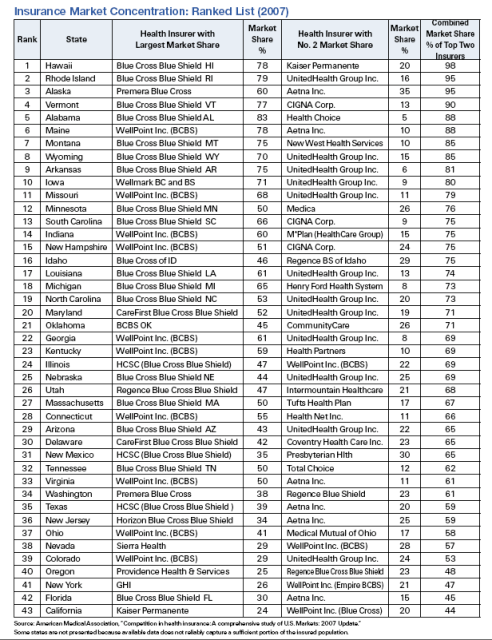

This strength in pricing is caused by an utter lack of competition. Most states are dominated by one or two carriers, as shown here:

Berkeley economist James Robinson's influential study on consolidation of health insurers posits:

Outside health care, consolidation often signals a period of prosperity and decline, as the industry is spared both the rigors and the stimulus of competition. A sustained period of high prices and profits in health insurance would result in continuing shrinkage in the number of firms purchasing coverage for employees, which eventually would engender a political backlash.

Lack of market competition leads insurers to essentially pass along all costs to the consumer with no financial risk to itself. With no financial risk to itself running the plan or competitive risk of losing customers, the carrier has no incentive to reduce costs - with the experience of my client being a prime example. This is how we see outsized profits in the private insurance industry - and the subsequent excessive compensation packages for their CEO's. These profits and executive compensation paint a picture of health for the insurance companies that masks the long term prognosis - the collapse of the business model.

The predictability of insurance relies upon the law of large numbers. Because of this, small employers will always be at a pricing disadvantage compared to large employers. There just aren’t enough employees in a small group to spread the risk of catastrophic claims. This has the effect of increasing prices for small firms relative to larger firms, even when the benefit plans are the same.

So if 80% of large employers opt out of the fully insured market, you are left trying to spread costs of catastrophic claims across smaller and smaller firms. That means higher overall insurance rates. This has the perverse effect of driving more large firms out of the fully insured market (knowing that they can do it themselves cheaper) and pushing more small firms out of any insurance at all (because they can’t afford it anymore). So Graham’s precious “middle” is getting smaller and smaller. And Robinson's supposition about the contraction of the market appears to be coming true.

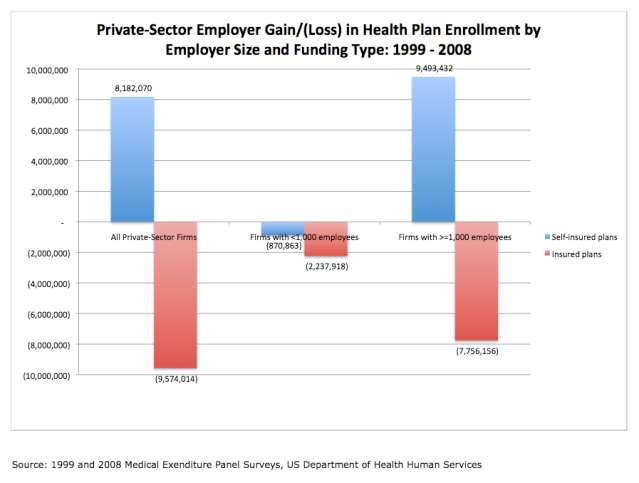

From 1999 through 2008, private-sector employment increased by just over 5 million employees. The percentage of employees in the private sector who work for firms offering health insurance fell from 89.1% to 87.7%, primarily due to small firms dropping coverage because of affordability issues. And the percentage of private-sector employees enrolled in self-insured plans jumped from 41.2% to 55.2% over those 10 years. This expansion was driven exclusively by the largest employers moving massively into self-insurance, jumping from 57% of employees in the largest firms covered by self-insurance in 1999 to a whopping 81.6% in 2008. The net effect is that private insurance companies lost 9.5 million members from their insured business over the last 10 years, while employers have taken on the financial risk of an additional 8.2 million employees through self-insurance during that same period.

We do not have a healthy private insurance market in terms of sustainability. What we are witnessing is the mass consolidation of carriers because they have no innovative way to grow organically. They are only growing through acquisition while, as evidenced in the chart above, their realistic universe of customers is shrinking. This is an industry that, absent major reform, will eventually collapse under its own weight of inefficiency and lack of innovation. It will be the service industry's version of the collapse of the US steel and auto industries.

Forcing private insurance carriers to provide coverage to people they deny coverage to today is necessary for universal coverage, but it will only serve to increase the rates they charge overall absent true competition or tight rate regulation. As Robinson further notes:

Consolidation of local markets, substantial barriers to new entry, few substitute products, ability to pass on increased provider costs, and a paucity of purchaser pressure are transforming competition in the health insurance industry. Further consolidation, and a further increase in entry barriers, is to be expected, as small local plans continue to sell out to the dominant carriers. The regional investor-owned health plans could be acquisition targets, offering national carriers increased enrollment and further reducing the potential for price competition.

The Republicans want us to believe in the power of the free market. But what the market is telling me is that private insurance companies are pricing themselves out of existence, and for those who can afford coverage, their insurance is likely to fail to protect them financially when they need it the most. Insurance that is too expensive and doesn't actually provide financial protection to its customers isn't a sound business practice.

The GOP fear that health care reform will kill private insurance. The sad truth is that private insurance is already killing itself today - without reform.

The only way private insurance is going to get healthy is through rigorous regulation, consumer protections, and true competition.