There’s no way to be nice about this. I need to scream to get your attention.

WE NOW HAVE ONE SHOT LEFT AT AVOIDING A FATE WORSE THAN THE 1920s- 1930s GREAT DEPRESSION.

One shot, that’s it. We must get a multi-trillion dollar stimulus bill that goes entirely into infrastructure, as Robert Reich has suggested..

There were actions that could have been taken this past year that would have stopped these crises, which could have been forced on the financial markets.

Bush, Bernanke, Paulson and the others in charge either did not see the need for these actions, or refused to impose them. Over a year has been wasted flinging piece-meal and ineffective actions at a mounting financial tsunami.

We now have one chance left at heading of these crises and avoiding a deterioration of our real economy into something I fear will be much, much worse than the First Great Depression.

I was covering and writing about deregulation and financial derivatives back when one of the very few Congressmen to oppose the deregulation of the savings and loans, Texas Democrat Henry Gonzales was chairman of the House Banking Committee (read Molly Ivins’ November 2000 obituary of Gonzalez here) and Richard Breeden was chairman of the SEC. Many of you probably know the general outline of the history of these issues the past 30 years. But in the late 80s to mid-90s, I was in some of the hearings where these ideas were debated in the Congress, in the SEC and CFTC and in some of the think tanks back in the late 1980s and early 1990s. I saw how Wall Street got its way over and over and over again.

For me, opposing Wall Street came down to one central idea – it’s the real economy that’s important, and the banking and financial system should always be kept in a position of subservience to it. It’s the real economy that produces and distributes the food we eat, the clothes we wear, the houses we live in, the cars and buses and trains and planes we ride in. The real economy provides what people needed to survive; by contrast, you can’t eat a debenture or a bond. And in the 1980s, the real economy, as I saw it, was being sacrificed to and looted by the banking and financial system.

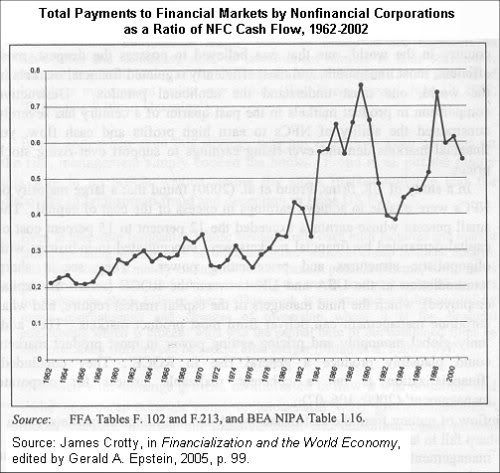

As Professor James Crotty has shown, the ratio of cash flow non-financial companies must give to the banking and financial system has more than doubled since the 1970s.

The trajectory of Breeden’s career mirrors exactly what has gone wrong with the banking and financial system. He was a lawyer at Cravath, Swaine & Moore, and Willkie Farr & Gallagher when both firms were eye-deep in the leveraged buyouts of the Michael Milkin / Drexel Burnham Lambert years (1970-1080s). At the SEC, Breeden was quite militant in his successful attempt to force a more lassaiz faire approach to financial markets. Then Breeden joined Baker Botts, the law firm tied so closely to Bush and Cheney. And guess what Breeden is now? A fracking hedge fund manager.

The financial catastrophe that has occurred under George W. Bush is thus only the logical result of the "post industrial" policy trends of the past three decades. People such as myself tried to warn about the eventual outcome for over thirty years, but so much money was being made by the people on Wall Street and in the futures pits of Chicago, that our voices were drowned out by the loud, noisy celebration of "success speaks for itself." I left my journalistic position in 1996, feeling very tired, belittled, jaded, cynical, and completely marginalized. Meanwhile Wall Street led the country on a tear of false prosperity that my fellow Americans can now see was nothing but debt, debt, debt, piled on more debt.

But by August 2007, it was clear to me that the collapse of two Bear Stearns hedge funds that had bought derivatives based on sub-prime mortgages had triggered a series of financial crises worse than the Great Depression. Worse than the collapse of Continental Illinois Bank. Worse than Long Term Capital Management. Worse than the peso crisis, the Indonesia crisis, the Japan crisis, the Russia crisis, the Enron scandal.

On Mon Oct 01, 2007, I wrote:

Clinton, Obama, Edwards, Richardson, Gore, whoever. Even if any of the Democrats win, it’s not really going to matter unless we get one thing straight.

This nation is screwed, economically. Only by openly and brazenly attacking the power and interests of the "economic royalists" (as Franklin Roosevelt called them) is anyone – Republican or Democratic – going to make any headway against the coming storm.

On Sun Dec 16, 2007, I wrote a diary entitled, Central banks look to financial 'nuclear option'. The week after that, a number of central banks, led by the U.S. Federal Reserve, poured $1 trillion – that’s trillion with a t, not a b – into the financial markets, in just three days.

With that $1 trillion, we passed a point of no return.

On Mon Jan 07, 2008, I wrote:

The sub-prime mortgage crisis pushed the world’s financial system passed the tipping point in August and the world’s financial system is now collapsing.

SNIP

The obvious conclusion is that the next president of the United States is going to be dealing with an economic collapse. The extreme level of economic hardship that will likely result is going to make the population more open to radical solutions – Naomi Klein’s shock doctrine – but whether the population will opt for progressive solutions or go the way of Germany in the 1920s and 1930s is, I fear, entirely open to question. It will be a terrifyingly interesting dynamic between the next President and the howls of pain from the mob outside that will determine which way the next president goes in dealing with the economic collapse.

My own view is that this is going to be a fight to the death. Either we demolish the power of Wall Street and dismantle the structure of speculative finance and return to industrial capitalism and a Keynesian goal of full employment and wage growth, or the United States will cease to exist as a free, democratic republic in the next ten to twenty years. I honestly believe the stakes are that high.

I wrote this on Mon Mar 03, 2008

So, this is it. The financial system has crashed. Now we're finally seeing the Republican's cherished "trickle down" theories begin to work – and with a vengeance- as the damage spreads into the real economy. The basic mechanism for this is the contraction of credit, which is cutting off funds for real economic activity. Goldman Sachs and others estimate that the financial crash has contracted lending by about $2 trillion--and our economy is $15 trillion in GDP. Banks and other institutions are simply unwilling to lend.

On Tue Apr 22, 2008, a few weeks after the "rescue" of Bear Stearns, I wrote in Euthanize Wall Street to save the economy:

The "bail out" of Bear Stearns five weeks ago did nothing to solve the underlying causes of the unfolding financial meltdown, so another major crisis is unavoidable.

SNIP

the goal in the next crisis point of the financial collapse should be to ruthlessly euthanize the biggest institutions on Wall Street.

SNIP

Before the next Bear Stearns hits, we need to answer the question: What do we want the financial system to do? When we are facing global crises of food and water shortages, and global climate change, I suggest that we can no longer afford to allow the financial elites to use the economy’s credit mechanism for their own private gain. We must begin to think, plan, and build long-term. It makes no sense to face the future hobbled with a financial system that is oriented to short-term speculation and self-aggrandizement. We need to redirect credit away from speculation and into the building of a new, green economy.

When Wall Street finally collapsed in September, and the $700 billion bailout was being shoved down our throats, I reiterated, Let Wall Street Burn. The $700 billion would be wasted, because, again, it was not addressing the real problem: an out-of-control financial and banking system that was not meeting the needs of the real economy.

Rather than that $700 billion going to pay Wall Street bonuses and allowing banks to buy other banks, we should have used it to start putting people to work in real jobs building the new infrastructure we need for a green economy. That would have saved the auto industry - if the auto industry had decided to help meet the need.

And, just to remind you, I've have tried to warn a week ago that Obama's short list for Treasury Secretary points to a continuation of the disaster, and that I think a crucial fight has broken into the open for the economic policy soul of President Obama.

Now, we now have one shot, and one shot only, left at avoiding a fate worse than the 1920s and 1930s Great Depression. We must get a multi-trillion dollar stimulus bill that goes entirely into infrastructure, as Robert Reich has suggested.

This is it folks. We either do that, or there's no way out of the worst economic catastrophe in the history of mankind.

And, no, I am not exaggerating.

This could have been stopped at some point in the last half of last year, by the federal government immediately suspending all foreclosures, and forcing the banks and mortgage lenders to forego the interest rate increases called for in ARM mortgages. If someone was paying a mortgage at 4.25 percent interest, and then are not able to pay when the interest rate resets at nine or ten percent, the mortgage lender could have been forced to keep the interest rate at 4.25 percent interest.

Of course, this would have violated the sacred free workings of the market. So no one in the U.S. elite even floated the idea. Certainly not Bush and his coteries of knuckle-dragging market fundamentalists. But neither was there a peep from any Democrats, including Barack Obama.

Cramming the mortgages down the banks will still have to be done. But it should have been done last summer. Now, the damage has been inflicted: over a million homes have already been foreclosed, and another 1.5 million homes are in the process of foreclosure.

Residential construction employment has fallen off a cliff, and commercial construction employment is now following. The U.S. auto industry, which broadly accounts for one of every ten jobs in the U,S., is basically bankrupt and pleading to be put on life support. World maritime shipping has been torpedoed, and many firms are now paying multi-million dollar penalties to cancel new shipbuilding contracts rather than take delivery of new cargo ships that cannot be filled.

But the point here is that an economic collapse today is going to be much worse that it was in the 1920s and 1930s. James Kuntsler actually wrote something very similar to what's below a few months ago. In fact, I think much of what's below was lifted from Kuntsler.

Letter Re: The Depression of the 1930s--Why No Societal Collapse?

There are some substantial differences between our society in the early 21st Century, and America in the 1930s. With these differences, our society is now much more fragile and vulnerable to collapse. Here are a few that come immediately to mind:

Consider the Attributes of America in the 1930s :

A largely agrarian and self-sufficient society. (Now, just 1% of the population operating farms and ranches feed the other 99%.)

Not heavily dependent on computing and communications, technology, grid power, and petroleum-based fuels.

Shorter chains of supply. Most food was grown within 100 miles of where people lived.

A very small underclass that was dependent on charity or public welfare.

Lower property tax rates and lower (or nonexistent) license fees, vehicle registration fees, et cetera.

The majority of workers lived near their work.

Most displaced workers were willing to accept lower-paying jobs--even doing hard physical labor.

The entire nation was economically self-sufficient and could carry on without many imports.

Far greater self-sufficiency at the household level (domestic water wells, windmills, wood burning stoves, home vegetable gardens, home canning, and so forth)

A much lower level of indebtedness (public and private). At the outset of the Depression most families had cash savings. (We are now a nation of debtors.)

A sound currency, still backed by specie. (Although FDR's administration seized most privately-held gold in 1933, the currency was at least still fully redeemable in silver coinage until 1964.)

Lower percentage of corporate employment--so there were less risk of huge layoffs that would devastate communities

A significantly more moral society that still had compunctions and a prevalently law-abiding attitude.

A homogeneous population that largely shared common Judeo-Christian values. A much larger portion of society attended church regularly

A simpler, less extravagant lifestyle, with tastes in cooking and entertainment that did not require large outlays of cash.

Most families owned only one car (with proportionately lower registration and insurance costs), and they lived in smaller homes that were less expensive to heat.

In summary, in the 1930s it cost a lot less to live (as a percentage of income) and people were willing, able, and accustomed to "making do" without. When people lost their jobs, in many cases they didn't lose their homes because they were paid for. Many folks could simply revert to a self-sufficient lifestyle and earn enough with odd jobs to pay their property taxes. What fraction of

The bottom line: If America were to experience a Second Great Depression, given the high level of debt and systems dependence, there would be enormous rates of dislocation and homelessness. And with modern-day immorality and the prevalent "me first " attitude, I have no doubt that riots and looting would absolutely explode.

Now is the time for very, very bold action. Even bolder than what Paul Krugman and Robert Reich have proposed. We’ve got one shot at getting it right this time. Let’s not blow it again.